So Growth Is Slowing. And? We're Still Up a Ton: Taking Stock

So Growth Is Slowing. And? We're Still Up a Ton: Taking Stock

(Bloomberg) -- S&P futures look poised to give back about half their gains from Friday, even after the twin growth "scares," if you want to call them that.

The IMF cut its growth outlook for the second time in 3 months ahead of Davos, which got underway earlier Tuesday, while China’s 2018 GDP figures came in at the slowest pace in nearly 30 years (though on a much larger economic base). China’s GDP was in line with expectations, and while it adds fuel to the concern of slowing worldwide growth, I’m sure it will surprise very few that they failed to outperform amid a trade war with their largest partner.

Developments on that front also lost a bit of steam over the weekend to be sure, despite the optimism Friday on reports China was offering to close the trade gap with the U.S. by 2024. That led to the S&P 500’s second best day of the year.

Hopefully we’ll get more color on trade from a micro level later today with IBM’s quarterly results (they attribute nearly 20% of their revenue from the region) -- its first since announcing the mega deal for Red Hat in December.

Flood Gates

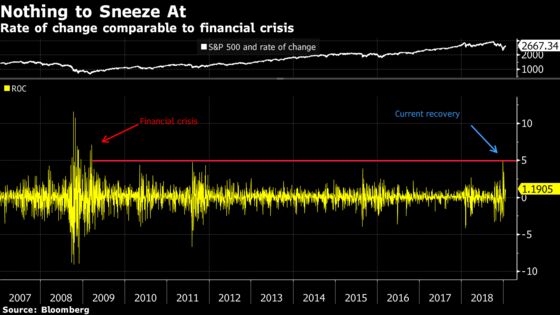

And with that optimism Friday and the 50-DMA in the rear view, bullish strategists’ eyes have now been set on 2,700 as the next target within reach, seemingly without fully appreciating how far we have come. The chorus seems to have accepted a full recovery as a natural thing and that it was only a matter time, without taking into account how "dire" it may have felt in the moment. Some of that may have rightfully attributed to the fact that economic figures by and large have been fine. But getting caught up on the nominal figures ignores the logarithmic nature of recent returns, which have have been quite extraordinary.

Nomura analysts recently called responses to positive headlines "asymmetrically" large. Gains are broad-based to be sure, with all sectors in the green since Dec. 26. Previous outperformers from 2018 are once again atop the list (Nektar Therapeutics, Celgene), with energy names Hess and Newfield Exploration not far behind with gains in excess of 40 percent over the past 3 weeks.

Bernstein for its part last week advocated a "low and slow portfolio strategy" in response in current conditions, specifically within stocks that outperform during a slowdown period but are not explicitly defensive. Some of the names that Bernstein felt could outperform at the end of the cycle and with less exposure to wage pressures included some health (ABBV, STZ, ANTM), consumer staples (STZ, PM), banking (SYF, STI), energy and transport (JBHT, APC) names to name a few.

The last grouping has some significance as energy is by far the biggest outperformer in the latest V-shaped recovery since Dec. 26 and should be in focus today after Halliburton’s results (following peer Schlumberger’s Friday performance post earnings -- its largest gain in nearly 8 years). Tudor Pickering wrote that the oil servicer’s results won’t necessarily revive the sector, but with Brent and WTI crude prices sustaining 15% and 16% gains respectively over the past month, there’s sure to be support (today may act as a check however with WTI down 2% in the early going).

Sectors in Focus

Wealth managers, especially in Europe (watch BAER SW, U.S. names BLK, FRC, SIVB) after UBS’s results warned that its wealth management segment was not meeting expectations. This follows Morgan Stanley which also cited weakness in its wealth management unit for their poor results last week.

Reports of proposed export bans on Huawei and ZTE products from a bipartisan group of lawmakers in the U.S. could add additional pressures on suppliers heavily geared towards the Chinese technology giants, such as optical and semiconductor names ACIA, LITE, IPHI, NPTN (already indicated lower by 6%), QRVO, SWKS, AVGO. More details can be found in Bloomberg Intelligence’s report: Huawei’s Trials and Tribulations

Canadian ADRs after the S&P/Toronto Stock Exchange Composite Index extended its streak of gains to a 12th day on Monday. U.S. shares will be poised to catch up following the Martin Luther King Jr. Day market closure.

Blizzard related names following Winter Storm Harper that brought heavy snowfall to many parts of the U.S.; watching Ski resort names MTN, SKIS, generator manufacturer GNRC and road care names PLOW, CMP, TTC.

Your 87-Hour ICYMI

Here’s some stuff you might have missed since Friday’s close:

Tesla continues its whiplash with investors, with Electrek reporting a "significant" boost to prices for its supercharging program, days after warning of headcount reductions in the wake of lower profit expectations that sent shares down the most since it was sued by the SEC in Sept.; Both NFL conference championships went to overtime, with "underdog" Patriots outlasting the Chiefs after 38 total points were scored in the fourth quarter, while the Saints lost after a now infamous "no call" for pass interference in the matchup with the Rams; California Senator Kamala Harris has thrown her hat into the ring for 2020 race for the White House; Sec. of State Pompeo (formerly the Director of the CIA) is considering a bid for the Kansas Senate, according to CNN; WSJ was out with a feature comparing JC Penney to the plight of Sears; Pawn shops and payday lenders were highlighted in the FT (albeit morbidly in this author’s humble opinion) as potential beneficiaries of the U.S. Government shutdown; Trump offered a deal on "Dreamers" in exchange for border wall funding which is unlikely to receive bipartisan support; the Super Blood Wolf Moon came and went, with the next lunar eclipse due in 2021.

Notes From the Sell Side

Nike is trading higher in the pre-market after getting an upgrade from Cowen’s John Kernan. He cited the possibility for "at least 200 bps" in gross margin improvement, which could offset cost pressures. He is optimistic about the athletic wear company’s ability to sense and react to consumer signals quickly and continue its higher, full-price sale through. His new PT anticipates 12% upside.

CRISPR Therapeutics was cut to sell at Citi, after analyst Yigal Nochomovitz suggested that some of its technology and programs lag more advanced competitors. He cited bluebird bio and Global Blood as competitors that were out in front of the gene editing biotech firm by almost 5 years. He sees a lack of catalysts in 2019 as part of the rationale for his Street-low price target of $21.

Tick-by-Tick Guide to Today’s Actionable Events

- Today -- 2019 World Economic Forum in Davos begins; Argus Americas Crude Summit in Houston

- 8:30am -- JNJ earnings call

- 9:00am -- HAL earnings call

- 10:00am -- Existing home sales

- 4:01pm -- AMTD earnings

- 4:05pm -- IBM earnings

- 4:05pm -- COF earnings

- 5:00pm -- IBM, COF earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.