SmileDirect Reverses 2020 Gains on Disappointing Year View

SmileDirect Reverses 2020 Gains on Disappointing Year View

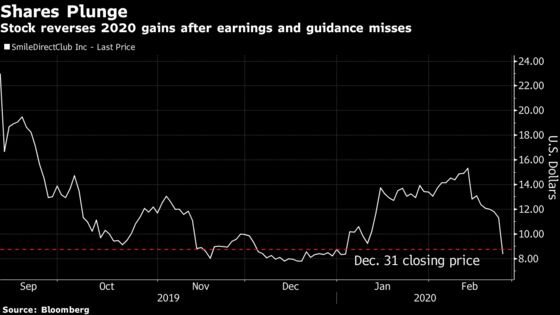

(Bloomberg) -- SmileDirectClub Inc. shares tumbled as much as 29% Wednesday after analysts said disappointing quarterly results and 2020 guidance could further push out profitability for the maker of teeth-straightening products.

“While we don’t think the business is broken, climbing out of the penalty box may take a few quarters of improved execution,” Jefferies analyst Brandon Couillard said, cutting the stock to hold from buy.

The poor quarter comes at a bad time for the disruptor in the orthodontic market. In less than two weeks, early investors and some insiders will get their first chance to sell when the initial public offering lockup expires. Indications from management that SmileDirect is ramping up spending in international markets could spell trouble for its core U.S. market, which Jefferies said “may be maturing faster than expected.”

SmileDirect’s loss on Wednesday reversed the stock’s 30% year-to-date rally through the prior day’s close.

Here’s what analysts are saying:

Jefferies, Brandon Couillard

The firm sees “less of an open-ended growth story,” as the company “plans to pump the brakes on growth to focus on more profitability and customer satisfaction.”

While SmileDirect’s fourth-quarter revenue missed, the adjusted Ebitda loss of $60 million was “more alarming,” which the company attributed to manufacturing issues that “won’t be fully remedied” until the second half of the year and “higher SG&A spend in support of a ’20 growth outlook that is no longer relevant.”

On the back of the weak 2020 guidance, profitability appears “pushed out” and the “much more aggressive” ramp in its market outside the U.S. is “another concerning sign that the US may be slowing faster than expected.”

“Given the accelerated cash burn, it may need additional capital sooner than expected.”

Downgraded the stock to hold from buy and cut its price target to $10 from $22.

William Blair, John Kreger

“The primary culprit for this surprisingly lower guidance is difficulty scaling the manufacturing operation, which in turn is pressuring gross margins, lowering shipment volumes, and straining customer support.”

Noted that management set a goal for positive Ebitda by the fourth quarter, “which is three quarters later than our model assumed,” and indicated a plan to scale back expansion spending on U.S. SmileShops and lay off staff in production and support.

“Such cuts should help reduce losses by the second quarter, although it will be interesting to see if the company can pull back on spending without hurting operations at the same time.”

Following the reduced 2020 outlook, the firm expects the stock “to be down materially, likely giving up recent gains,” as the current loss trends are expected to continue through the first half of the year.

Has an outperform rating on the stock.

JPMorgan, Robbie Marcus

“Though a disappointing close to 2019, we view the issues that stifled 4Q growth as transient in nature due to manufacturing, rather than a demand issue.”

The miss in SmileDirect’s initial 2020 guidance is “due primarily to the company’s efforts to employ a more controlled growth strategy to focus on optimizing the customer experience while experiencing manufacturing headwinds.”

Noted that the company is choosing to allocate more supply to newly launched international markets “while not fully pushing demand in the U.S. to where it could be.”

The firm sees “paths to upside in 2020 as the company continues to enter high-growth, low-penetration international markets, expands its portfolio of products and enters new channels.”

Has an overweight rating on the stock and lowered its price target to $16 from Street high of $31.

What Bloomberg Intelligence Says

“Post-4Q Earnings Outlook: SmileDirectClub’s 2019 close and initial 2020 view fell short as its credibility took another blow. The most incremental revelation was that SmileDirect will now focus on “controlling growth” and delivering profit after conceding it was unable to keep up with the demand and subsequent customer care associated with frenetic business expansion. The pathway to positive Ebitda by 4Q and beyond is ambiguous, with management broadly pointing to cost control and manufacturing automation as the means.”

--Analyst Fallon Stephan

--Click here for the research

To contact the reporter on this story: Andres Guerra Luz in New York at aluz8@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Will Daley, Steven Fromm

©2020 Bloomberg L.P.