Sluggish Bond Market Is the Latest Headache for Indian Firms

India needs a bigger bond market now more than ever. But its growth is likely to a hit this year.

(Bloomberg) -- India needs a bigger bond market now more than ever, to help get funds to cash-strapped companies cut off from their shadow lenders by a crisis in that sector.

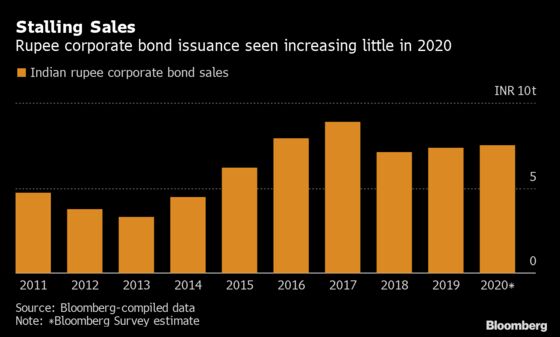

But a Bloomberg survey shows that sales of local rupee corporate notes will grow only 2% this year, a similar rate to 2019 that’s historically low. India’s corporate bond market remains small compared with other major economies, and outstanding rupee issuance amounts to the equivalent of about $540 billion, less than 10% of what is due in China.

Prospects of flat issuance is bad news for Prime Minister Narendra Modi’s efforts to revive sagging growth, with tight credit conditions feeding a vicious cycle of reduced consumption and investment. Smaller companies, which represent about half of the economy, are struggling with a double blow from a funding squeeze at shadow lenders, and investor wariness of anything but top-rated debt, often meaning government-backed ones.

Companies will raise around 7.5 trillion rupees ($105.5 billion) through domestic bonds this year, according to the average estimate from 11 of India’s top corporate bond arrangers, surveyed by Bloomberg. That’s an increase of about 2% on sales in 2019, and compares with a gain of about 28% a year on average from 2014 to 2017, according to data compiled by Bloomberg.

A stalling in issuance also undercuts attempts by Finance Minister Nirmala Sitharaman and predecessors to expand India’s corporate bond market to better distribute credit risks and wean reliance off bank loans.

All the news for the market isn’t bad, however, with some arrangers expecting state-owned companies to boost issuance to help push forward government investment plans. There are also some signs of improvement at the shadow bank sector, following a string of central bank rate cuts.

Here are some rupee bond arrangers’ outlooks for the market for this year:

ICICI Securities Primary Dealership (Shameek Ray, head of debt capital markets)

- “Overall rupee-denominated bond sales could show no or low growth as the trend for many companies to borrow through bank loans or from overseas markets may continue for some time.”

- “The need to push growth in the economy will fuel financing needs of state-owned companies. Government’s large infrastructure spending target and kick-start of capex will be routed through these companies and hence I see a strong year of issuance from them.”

- “As credit market hopefully returns to normalcy this year, I expect risk appetite to improve. Compelling spreads may coax investors to lend to non-AAA rated companies.”

Trust Capital Services India (Sandeep Bagla, associate director)

- “The worst is behind us, and gradually we should see corporates tapping the market.”

- “I expect most of the borrowing by companies would be to meet refinancing needs or for working capital requirements.”

- “I expect some pick-up in issuance where proceeds would be used for promoter financing or for real estate developments or bonds issued by NBFCs that lend to builders. Although, bond covenants may be tighter and higher interest rates may be charged by the investors.”

Derivium Genev (Ashish Ghiya, managing director)

- “Barring a few non-bank finance companies that missed repayments, we haven’t seen any further negative news from this sector in the last three months, indicating that others have managed their asset-liabilities well.”

- “I expect overall bond issuance volumes to increase, with more diverse issuers raising debt capital market funding.”

- “Cost of borrowing should be easy as RBI may need to be more growth supportive in its stance and actions. That said, however, higher government and quasi-government borrowing may keep the term and credit spreads at elevated levels.”

--With assistance from Swansy Afonso and Sheenu Gupta.

To contact the reporter on this story: Divya Patil in Mumbai at dpatil7@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Finbarr Flynn, Ken McCallum

©2020 Bloomberg L.P.