Singapore Dollar’s Winning Streak Faces Toughest Test Yet

Singapore Dollar Bulls Look to CPI to Keep MAS on Hawkish Path

(Bloomberg) -- The Singapore dollar’s three-month winning streak is facing its stiffest test yet as global growth headwinds dim the outlook for further central bank tightening. An above-consensus inflation report Monday would go a long way toward ensuring the currency’s advance remains on track.

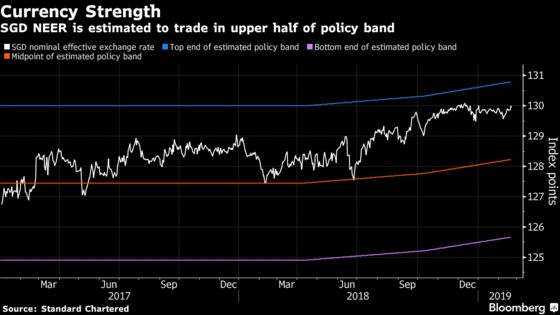

A gauge of the country’s nominal effective exchange rate, which the Monetary Authority of Singapore guides to conduct policy, is showing signs of weakness amid continued global trade tensions and a slowdown in China. On the flip side, strong domestic demand and resilient inflation are keeping alive wagers that the MAS will accelerate the pace of appreciation for a third straight time in April.

The clashing signals raise the stakes for economic data due in the run up to the decision. Here’s what traders will be keeping an eye on.

Unlike most central banks that use interest rates to tackle inflation and growth, the MAS instead steers the local dollar against a basket of its counterparts, adjusting the pace of appreciation, known as the slope, the width of the target band and the level at which that band is centered.

The MAS tightened policy in both of its decisions last year, spurred by rising inflation underpinned by an improving labor market and a robust economic expansion.

The country’s leading index suggests growth is set to remain steady, even amid increased downside risks to the global economy. Similar gauges tracking the OECD nations and China show waning momentum.

Resilient domestic demand will continue to put pressure on core inflation, which is hovering at the highest since 2014. Should growth accelerate, there could be a greater pass-through of import and labor costs to consumers, the MAS and Trade Ministry said in their last inflation report in January.

The central bank’s April policy decision is still “live,” Mohamed Faiz Nagutha, an economist at Bank of America Merrill Lynch, wrote in a Feb. 19 note to clients. The central bank could surprise the market with a hawkish bias given core inflation at or above the historical average, he wrote.

Still, increasing uncertainty over the global growth outlook has taken some of the wind out of the Singapore dollar’s sails. The International Monetary Fund cut its forecast for the world economy for the second time in three months in January, while warning rising trade tensions could spell further trouble.

The nominal effective exchange rate is estimated to be trading about 1.4 percent above the midpoint of the central bank’s policy band, down from a high of 1.6 percent in December, according to a Standard Chartered model. Versus the greenback, the Singapore dollar has weakened about 0.4 percent this month, sliding to 1.3511 at the close of trading Friday.

Fiscal spending will offer little support to mitigate the external risks. The macroeconomic impact of the budget is expected to be neutral this fiscal year, a government report last week showed.

Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. in Singapore, sees a 60 percent chance that the MAS will tighten policy in April, down from almost 80 percent previously.

“It’s a binary risk,’’ he said. “A pause after back-to-back tightening in 2018 admittedly makes for an increasingly compelling case.”

Below are key Asian economic data and events due:

- Feb. 25: Singapore January inflation, New Zealand 4Q retail sales

- Feb. 26: Singapore January industrial production, Taiwan January industrial production and unemployment rate, Hong Kong January trade balance.

- Feb. 27: Bank of Japan board member Goushi Kataoka speaks, New Zealand January trade balance, Hong Kong 4Q GDP

- Feb. 28: Bank of Korea policy decision, Bank of Japan board member Hitoshi Suzuki speaks, South Korea January industrial production, Japan weekly portfolio flow data, January retail sales and January industrial production, New Zealand February business confidence, Australia 4Q capital expenditure and January private sector credit, China February official PMI, Thailand January current-account balance

- March 1: New Zealand January building permits and 4Q terms of trade, Australia February home prices, Japan January jobless rate, February Tokyo CPI and 4Q capital spending, South Korea February trade balance, February PMIs for Malaysia, Thailand, Philippines, Indonesia and India, China February Caixin PMI, February CPI for Thailand and Indonesia

To contact the reporter on this story: Masaki Kondo in Singapore at mkondo3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.