Singapore Braces for More Delistings Even After Rule Fix

Singapore Braces for More Delistings Even After Rule Fix

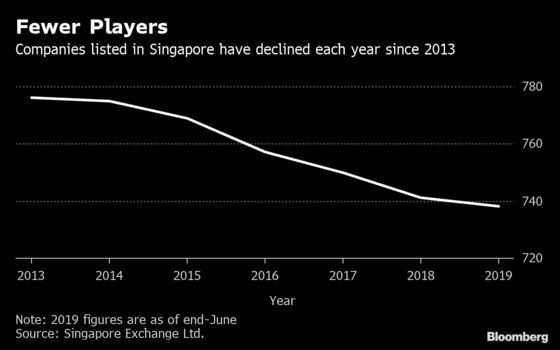

(Bloomberg) -- This year, Singapore’s stock market has seen on average of two companies a month looking to delist. The trend may not be reversing any time soon.

The Singapore exchange tweaked the voluntary delisting rules earlier this month, shifting the power to minority shareholders. Market watchers have said bidders may have to pay higher premiums to get deals done.

Delistings are expected to continue in the second half of this year even at higher prices, according to a poll of four analysts, because the rule change doesn’t affect the persistently low valuations which continue to plague the Singapore market. The Straits Times Index is trading at one-year forward price-to-book ratio of 1.13 compared with 1.71 for the MSCI Asean Index, according to data compiled by Bloomberg.

Taking listed firms private has been a key theme in Singapore’s equity market over the past few years as major shareholders, institutional investors and industry peers buy up companies due to low multiples. Fourteen companies are undergoing privatization or in the process of being bought out this year, the highest number since 2016, according to a report from DBS Group Holdings Ltd. this month.

“New rules will not entirely derail the trend of delistings in Singapore. In fact delistings may continue at a similar rate,” said Nirgunan Tiruchelvam, head of consumer equity at research firm Tellimer Research. “Premiums can rise but not beyond what’s affordable.”

To be sure, while delistings have picked up, equity offerings have also jumped in Singapore with firms raising $1.67 billion in initial share sales this year, more than the entire amount issued for the whole of 2018, according to data compiled by Bloomberg.

Here are five companies that analysts say are ripe for potential delistings:

SIA Engineering Co. (DBS)

- “SIA Engineering stock price has performed poorly of late, and could thus provide a value for money privatization target for SIA,” said DBS analyst Suvro Sarkar.

- He added that the benefits of keeping SIA Engineering listed is not clear given the stock’s low liquidity and the fact it’s already a cash-rich company.

- SIA Engineering’s officials did not immediately reply to an email seeking comment.

Unusual Ltd. (RHB Securities)

- The event producer and promoter has the largest market share in Singapore for concerts, has strong connections with Canto-pop artists, and can offer Asia access to a larger foreign competitor, said RHB Securities analyst Jarick Seet.

- Valuations are “now compelling for the company, especially since foreign peers are all trading at a way higher multiple as compared to Unusual”, he said. “Unusual is also on a growth phase itself in the last 2-3 years.”

- Company officials did not immediately reply to an email seeking comment.

Fu Yu Corp. (DBS and RHB Securities)

- A DBS report dated July 2 cited “attractive” valuations and net cash accounting for 54% of its market capitalization as reasons for a potential privatization or takeover offer.

- RHB’s Seet says the plastic component manufacturer is an attractive target for larger competitors who want a Southeast Asian exposure to diversify away from the U.S. and China markets.

- Octant Consulting’s Hermen Phua, whose firm handles investor relations for Fu Yu, said the company doesn’t comment on market speculation.

Frencken Group Ltd. (KGI Securities (Singapore) Pte.)

- Group is diversified in several businesses including the semiconductor, medical, analytical, automotive, and industrials sectors. This makes it an attractive target for a bigger competitor to acquire new customers and business segments, said KGI analyst Joel Ng.

- “It is also among the cheapest of the tech-manufacturers listed in Singapore,” he adds.

- Octant’s Phua, whose firm also handles investor relations for Frencken Group, said the company doesn’t comment on market speculation.

The Hour Glass Ltd. (KGI Securities)

- The watch and jewelry seller recently reported its highest annual profit in more than 20 years and trades at an attractive historical price-to-earnings ratio, while cash makes up 30% of its market value, said KGI’s Ng.

- He said “the Tay family (Henry Tay and Michael Tay) owns around 67%” of the company and “has been buying back shares in the open market. We think it makes sense for the Tay Family to privatize or either sell to a global luxury brand.”

- Company officials did not immediately reply to an email seeking comment.

--With assistance from Joyce Koh and Zhen Hao Toh.

To contact the reporters on this story: Yongchang Chin in Singapore at ychin22@bloomberg.net;Ishika Mookerjee in Singapore at imookerjee@bloomberg.net;Abhishek Vishnoi in Singapore at avishnoi4@bloomberg.net

To contact the editors responsible for this story: Lianting Tu at ltu4@bloomberg.net, Teo Chian Wei

©2019 Bloomberg L.P.