(Bloomberg Opinion) -- Breaking up a European conglomerate is hard to do. Executives like the prestige, money and influence that comes with managing a giant company. Employees worry that belonging to a smaller enterprise may leave their jobs vulnerable, and in Germany workers have board representation. Absent a crisis or recession, companies see little urgency to reform.

So it’s pretty remarkable just how far Joe Kaeser has pushed Siemens AG to change.

On Tuesday evening, the Siemens boss – whose background is in finance, not engineering – announced the latest and most radical step so far to slim down one of Europe’s most important industrial companies. In profitability and valuation terms, his revolution is far from complete. Even so, he deserves credit for taking decisive action before activist hedge funds take aim at the Munich-based manufacturer, or a more dramatic reversal occurs, as has happened at its bitter U.S. rival General Electric Co.

The carve-out and listing of the company’s power, gas and wind activities will lop off 27 billion euros ($30 billion) of its sales, about one-third of the group total. In future, Siemens will become a holding company whose core assets are technology and software for infrastructure and factories. For now, the train business will be kept – a proposed merged with Alstom SA was blocked – but it’s questionable whether Siemens will own it in the long term.

In view of their better margins, the hope must be that the stock market will accord these core industrial activities a superior valuation; America’s Rockwell Automation Inc., for example, trades on about 19 times estimated earnings versus Siemens’s 15 times.

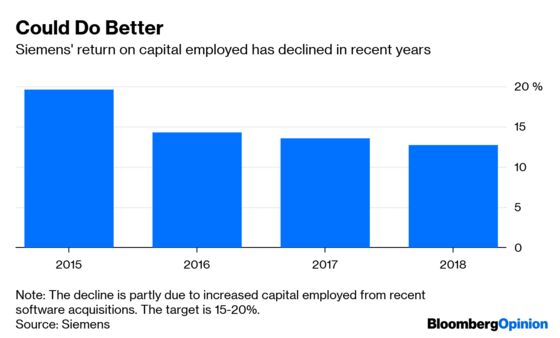

Yet for all his activity, Kaeser’s record on delivering shareholder value has been mixed. He spent $7.6 billion on oil equipment company Dresser Rand in 2014, just before oil prices tanked. Management infighting undermined the merger of Siemens’s wind business with Spain’s Gamesa. Collapsing demand for gas turbines has caused profits in its power and gas business to tank (although that’s hardly Kaeser’s fault). Returns on capital employed – a priority for Siemens – are a long way off the goal of 15-20 percent.

While the Siemens healthcare business has performed well since its IPO last year, its rising share price only underscores how little value investors ascribed to the rest of the business.

Still, Kaeser’s right to plow on. At their best, conglomerates help drive shared innovation, but too often this leads to a loss of accountability and enormous central costs. Having a diverse range of activities sounds like a useful defensive quality, but if they’re all being hit by technological upheaval simultaneously, it becomes a nightmare to manage.

Kaeser began his overhaul at Siemens by styling its various businesses as a “fleet of ships.” He’s right to cut the ropes and let some of them plot their own course.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.