(Bloomberg Opinion) -- Cash should be a byproduct of business success, not the goal itself. Royal Dutch Shell Plc has strained every sinew in recent years to satisfy investors’ hunger for generous dividends, and Tuesday’s strategy update was at pains to advertise its capacity to keep the funds flowing to shareholders. The Anglo-Dutch oil major foresees much stronger cash generation over the coming years. It has wisely resisted the temptation to make hard commitments on paying that out.

Shell says it has the potential to spend $125 billion on dividends and share repurchases between 2021 and 2025. That looks impressive. But it is not a pledge, and is not much more than the status quo. The annual dividend bill over the last year was an enormous $16 billion; the current buyback program averages out at just under $10 billion annually.

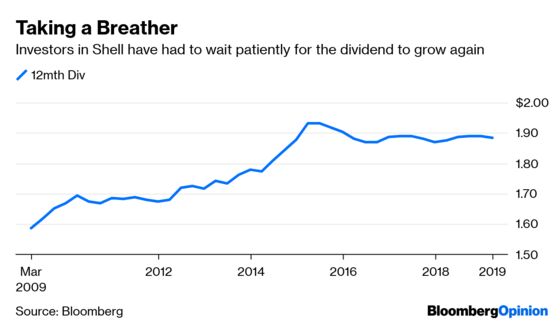

Given Shell expects to lift operating cash flow by $10 billion come 2025, investors might have hoped that the company could at last make a pledge to raise the annual dividend, having held it flat the last four years. But Shell has shown restraint, giving no guidance as to the mix of dividends and share buybacks within the headline number.

This makes sense as the dividend is still a serious drain on Shell’s financial resources. With the 2016 acquisition of BG Group and the oil price slump, the company had to resort to paying it partly in shares. Only recently has it returned to a full cash payout. Debt reduction following the takeover hasn’t been linear. A sudden turn in the macroeconomic environment would put the dividend under pressure once more.

Meanwhile, investment demands persist. Shell needs to spend $20 billion on capex just to maintain the current business. Debt remains too high. Add in dividends and interest, and around two-thirds of Shell’s operating cashflow is already spoken for. The remainder is allocated between “discretionary” buybacks and growth capex. It’s quite tight.

The latter is capped by Shell at $12 billion. Hardly any of this is allocated to discovering and producing oil. Rather, at least half is for downstream activities such as chemicals, lubricants and gasoline retailing, and just a fraction is allocated to Shell’s vision of becoming the world’s largest electricity company by the 2030s. There’s a caveat: a large, opportunistic M&A deal would require busting through that ceiling – while eating into funds available for a buyback and debt reduction.

Against that backdrop, Shell is in no position to raise the dividend just yet. By contrast, returning cash through share buybacks helps reduce the overall dividend bill by stealth by reducing the number of shares on which it is paid. With the shares yielding 6%, the trade makes sense. A dividend increase will come one day. For now, income investors should be glad the payout never got cut.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.