Shell’s Plan to ‘Do It All’ With Cash Pile Hits a Speedbump

Shell’s Plan to ‘Do It All’ With Cash Pile Hits a Speedbump

(Bloomberg) -- Royal Dutch Shell Plc, this year’s best-performing European oil major before a big earnings miss on Thursday, has hit a speedbump.

In January, Chief Financial Officer Jessica Uhl said the company wanted to “do it all” at $60 oil -- complete a $25 billion share buyback program, cut debt, cover capital expenditures, pay the dividend and grow the company with a ballooning pile of cash. Things haven’t quite gone to plan.

Slowing economic growth amid the U.S.-China trade war pummeled the Anglo-Dutch major’s petrochemical sales, a global oversupply of liquefied natural gas caused prices to crash and refining margins slumped in the second quarter. Net income fell to the lowest since 2016, missing even the most bearish analyst estimate and driving the shares down by the most in three years.

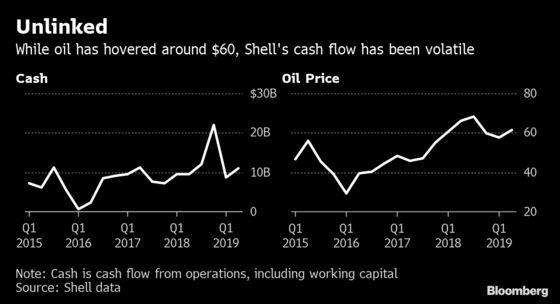

It also meant Shell wasn’t able to cover its interest, dividend and buyback payments of $7.1 billion with the free cash flow of $6.9 billion in the quarter, according to data provided by the company.

“We’ve seen some very severe macroeconomic headwinds,” Chief Executive Officer Ben van Beurden said in a Bloomberg TV interview. These conditions are unlikely to ease any time soon, according to Will Hares, an analyst at Bloomberg Intelligence.

Still, Shell fetched $61.26 for its oil in the three months, more than the $60 price at which it hoped to do it all. It was also higher than the $57.42 it got in the first quarter, when it posted stunning results.

Van Beurden on Thursday explained the real price at which it can cover spending next year is actually not $60 a barrel, but $65 because the company would have to account for inflation. That’s slightly higher than current Brent prices.

“If you it express it in money of the day, by next year we would be looking at $65,” he told reporters. “That still feels like a reasonable reference price to take.”

While crude was at levels that would’ve helped Shell meet earnings forecasts, other measures like lower natural gas prices and refining margins meant the company had a hard time, van Beurden told analysts on a conference call. Its massive oil and gas trading operations aren’t enough to offset a tough economic environment and “a meltdown in petrochemicals,” he said.

That’s not all. About 70% of Shell’s LNG contracts are linked to the price of Brent with about a four-month lag, van Beurden said. So not only does the company need oil to rise, it needs it to stay higher.

But these aren’t deterring Shell. It’s on track to meet its free cash flow goals for 2020, a measure van Beurden thinks is a better way to gauge the company. The oil major plans to deliver between $28 billion and $33 billion of cash by that metric, giving him confidence it’ll cover spending. The company also approved the next tranche of its buybacks, a $2.75 billion purchase.

“If we look at the continuation of our buyback program, we do take into account a range of scenarios that can happen to us,” van Beurden said. “The fact that we continue it is a sign of confidence that we believe in a whole range of reasonable macroeconomic outcomes, we can deliver it.”

To contact the reporter on this story: Kelly Gilblom in London at kgilblom@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Rakteem Katakey

©2019 Bloomberg L.P.