Shake Shack’s Business Model Slammed by Virus as Sales Plunge

Shake Shack’s Business Model Slammed by Virus as Sales Plunge

(Bloomberg) -- Shake Shack Inc. faces “outsized near-term risk” related to the impact of Covid-19, given its exposure to high-traffic, tourist areas and a lack of drive-thrus, analysts across Wall Street warned.

The company’s sales plunged 70% over the last two weeks with “significant declines expected to continue as stores operate as to-go and delivery only,” Credit Suisse analyst Lauren Silberman wrote. The bank downgraded its rating of shares to neutral from outperform and nearly halved its price target to $40.

While the fast-casual chain is boosting its delivery business through a number of third-party services, “a lack of drive thrus will hurt results,” Bloomberg Intelligence analyst Michael Halen wrote.

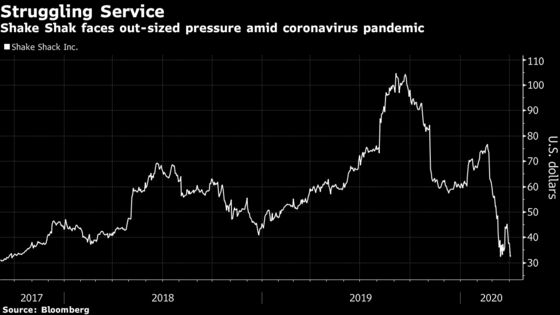

Shake Shack shares fell as much as 7% on Friday after the company said sales at U.S. company-owned stores that remain open are down between 50% and 90% when compared to the same period last year. The stock has fallen 30% over the past six sessions and is trading near its lowest level since September 2017.

Here’s what analysts are saying:

Credit Suisse, Lauren Silberman

“We expect the company to face meaningful declines for the foreseeable future.”

The company “has also reduced staffing and operating expenses across all Shacks, noting cost of goods sold are largely variable, labor is partially variable, rent is mostly fixed and operating expenses are about half variable.”

“Given uncertainty regarding the timing of a recovery (particularly in urban markets), a return to normalized sales levels and resumption of new unit growth, we are moving to the sidelines.”

Downgrades to neutral, price target slashed to $40 from $76.

Raymond James, Brian Vaccaro

“The magnitude of recent comp declines (down 70%, range of down 50-90%) was a bit worse than feared, with potential additional closures as the situation unfolds.”

“Sharp comp declines and uncertainty as to when unit growth could resume (key factor supporting historically high valuation) creates further potential downside risk.”

Maintains underperform rating and cut estimates based on the dropping comparable sales.

What Bloomberg Intelligence Says

“Shake Shack’s 1H sales and margins are poised to drop sharply due to shuttered U.S. dining rooms and other social-distancing tactics to reduce the spread of coronavirus, in our view. The chain temporarily shifted to off-premise only in mid-March and will likely close stores and reduce hours of operation in April.”

--Analyst Michael Halen

--Click here for the research

MKM Partners, Brett Levy

“With a higher % of units in urban markets, and many without drive-thru capabilities, this could represent an ongoing pressure point.”

Maintains neutral rating and $70 price target.

©2020 Bloomberg L.P.