India Credit Crunch Eases as Shadow Bank Bond Sales Rebound

Indian NBFCs are selling the most local-currency bonds since before a financial crisis engulfed the sector two years ago

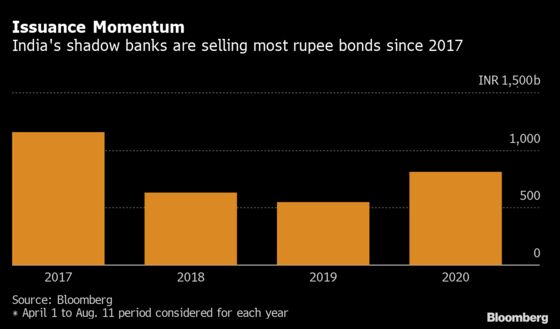

(Bloomberg) -- Indian shadow lenders are selling the most local-currency bonds since before a financial crisis engulfed the sector two years ago, in a sign that record stimulus is easing their fundraising burden.

The financiers have raised 860 billion rupees ($11.5 billion) through rupee notes since April 1, making it the best start to a financial year since 2017. Offerings from non-bank firms had declined in 2018 and 2019 as at least three shadow lenders defaulted on their repayments, battering investor demand for the sector’s debt.

More cash for shadow banks is good news for the Indian economy, which relies on these firms to provide financing to everyone from tailors to business giants. Non-bank lending is crucial in supporting Asia’s third-largest economy, which is forecast to contract for the first time in four decades this year due to fallout from the coronavirus pandemic.

To help non-bank financiers counter the economic impact of the outbreak, the government in May announced a 300 billion rupee credit line for these financiers, and said it will fully guarantee investment-grade securities issued under this plan.

To further assist lower-rated shadow banks, the administration agreed to also provide a partial guarantee to debt rated AA and below, injecting another 450 billion rupees. The central bank, meanwhile, funded banks’ purchases of bonds issued by these lenders to the tune of 128.5 billion rupees.

But challenges remain, with signs investor demand for the debt is uneven. It’s largely banks, which have to implement the economic stimulus steps, that are buying notes sold by shadow lenders. Other key players in the local credit market, such as mutual funds, halved their holdings of the bonds in the two-year period to June.

Moody’s Investors Service warned in June that the stress among these lenders may be deeper and broader than it thought and S&P Global Ratings cut credit scores of several such firms citing liquidity risks.

The financiers are at least benefiting from lower borrowing costs as a result of the stimulus package. Spreads on top-rated three-year bonds issued by non-bank companies fell 122 basis points in July, the steepest monthly drop since August 2013.

©2020 Bloomberg L.P.