Settling the Wild West: Companies Put Down Stakes on U.K.'s AIM

Settling the Wild West: Companies Put Down Stakes on U.K.'s AIM

(Bloomberg Markets) -- Marcus Stuttard doesn’t like the expression “Wild West.”

The label gets used a lot to describe AIM, the London Stock Exchange’s junior market for growth companies, and the two words provoke a mirthless laugh. “I care more about our market users than I do about people occasionally deciding to throw a bit of mud that’s not well-founded,” says Stuttard, the head of AIM.

AIM, once seen as a stepping stone for hundreds of small companies wanting to list on the exchange’s main market, has been trying for years—decades even—to get past its reputation as a volatile venue where corporate blowups are commonplace.

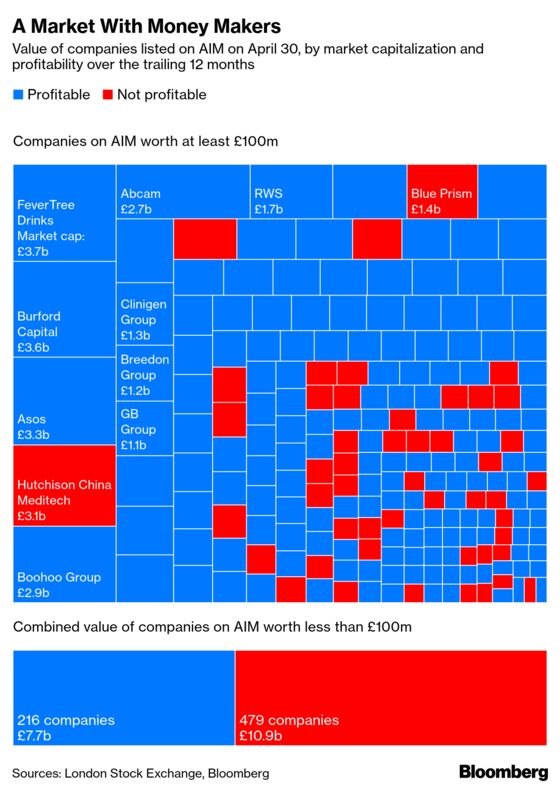

And for many investors and companies, it’s succeeded. A greater proportion of companies listed on AIM are profitable. Such stocks accounted for the highest percentage of the exchange’s market value in its history recently. Why? For one thing, more companies are staying on AIM even as their market valuations have ballooned.

So what’s changed?

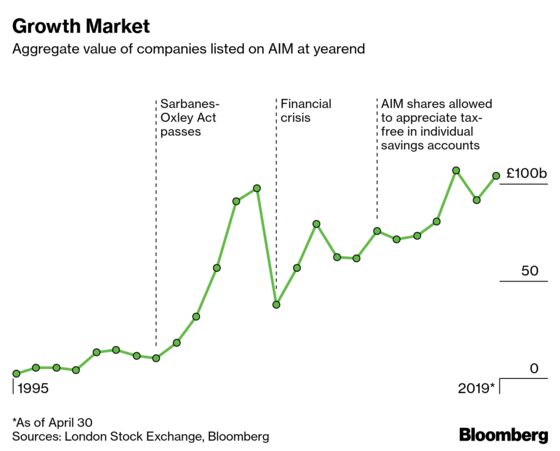

The types of companies on AIM are different. Started in June 1995, the submarket’s early years coincided with the dot-com boom, and it wasn’t immune when the bubble burst at the turn of the century. AIM went through another cycle of boom and bust as it pulled in listings by U.S. companies seeking to sidestep regulatory provisions of the 2002 Sarbanes-Oxley Act. Each bull market has led to a surge in listings, only to see some of those companies implode when the economy soured. Along the way, though, AIM has attracted companies from a wider variety of sectors, including consumer, health care, and industrials. Now, more than 10 years after the financial crisis, the market is thriving again.

Government measures have also helped. In 2013, AIM shares were allowed to be included in individual savings accounts for the first time, which meant investors wouldn’t be taxed on dividends or pay capital gains tax on profits. Another perk: Many AIM stocks are exempt from inheritance tax if they’ve been held for at least two years. Companies thus have less incentive to leap to the main board; they can now potentially have a stable investor base on AIM.

A number of U.K. household names have opted to stay on AIM, including online fashion retailer Asos Plc and premium tonic maker Fevertree Drinks Plc. This has pushed up valuations and helped improve the junior market’s reputation.

Asos is regarded as the first company that didn’t feel the need to move to the main market, says Phil Harris, a fund manager at EdenTree Investment Management Ltd. A spokesman for Asos says the company still doesn’t feel a need to move. “AIM works really well for us, and we have no compelling reason to change,” the spokesman says. “We keep it under review.” The London-based company listed at only 20 pence (26¢) in October 2001 and traded above £37 on May 15, a total return of 18,565%, or about 35% per year.

Shareholders used to expect companies to eventually move onto the “grown-up” main market. In fact, Harris says that 10 years ago, he would have been asking AIM companies that had grown sufficiently about whether it was time to consider transferring. These days, he doesn’t care which market they’re on. “It’s just not a conversation that ever comes up anymore,” he says.

What differentiates AIM from other growth markets around the world is its ability to marshal investors. Almost 60% of capital raised on European growth markets last year took place on London’s AIM. Helping drive that dominance are AIM’s so-called nominated advisers, or nomads, firms that guide companies during the listing process and in meeting their continuing obligations once they start trading. The nomads vet the companies they advise, which may make some investors more willing to invest.

Despite Brexit uncertainties, AIM companies raised almost £1.1 billion in the first three months of 2019 compared with only £424 million raised on eight other junior markets in Europe, according to accountancy company UHY Hacker Young Group. The number of initial public offerings on AIM slowed in that period, though, with only one listing in March, the lowest quarterly IPO activity in a decade.

The combined market valuation of the 904 companies listed on AIM was £97.6 billion at the end of March, with 46.6 billion shares traded that month, according to London Stock Exchange data. That compares with the main market’s aggregate valuation of £3.8 trillion.

For investors, AIM may offer the potential for higher returns, but it still comes with higher risks. Of the almost 4,000 companies that have listed on that market since its introduction, less than a quarter are still trading.

Part of what fueled AIM’s Wild West reputation were the mining and oil and gas companies that flocked to the market—only to delist a few years later. Those are sectors that Harris stays away from, because of the amount of travel that would be required to ensure that a company drilling in Africa, for example, has actually unearthed a viable amount of oil. “I don’t think they’re particularly interesting investments,” he says. “I don’t touch them, but I think that part of the market inevitably will always have that slightly more Wild West reputation.”

Even mining companies can decide to leave AIM. London-based Sirius Minerals Plc transferred to the main market in 2017. The company is developing the world’s biggest deposit of polyhalite, a mineral salt used as a fertilizer, at a site located in a national park in England’s eastern county of North Yorkshire. It expects production to start in 2021.

Nick King, Sirius Minerals’ general counsel and company secretary, says it was a natural evolution. “We felt it right to be seen to hold ourselves to the highest of standards, which was always our goal whilst on AIM,” he says. On the main market, the company’s reporting and disclosure requirements are higher because of its so-called premium listing, and items such as remuneration reports now require shareholder approval.

“Any perceived reputational issues for AIM are a bit unfair,” King says, adding that the submarket offers the opportunity for businesses without experience operating in a listed environment to develop appropriate systems and governance practices. “The trade-off for investors is that AIM businesses will be evolving these practices.”

Dozens of employees are immersed in their monitors on the trading floor of Winterflood Securities Ltd., located about a stone’s throw from the Thames River in London. The brokerage firm founded by financier Brian Winterflood was one of the original market makers when AIM started. Last year it was the leader in trading AIM shares, both by volume and value.

Ben Jowett, head of client sales and business development, has been with the company for more than two decades. He’s seen AIM outlive other European growth markets, including France’s Nouveau Marché, Germany’s Neuer Markt, and Italy’s Nuovo Mercato.

These days a lot of retail investors are placing orders through their smartphones and are attracted by the prospect of investing in a company that might one day strike oil or find gold, Jowett says. They’re also interested in tech stocks that may be developing game-changing technology, as well as companies that have the potential to grow exponentially.

The companies that get really big, such as Asos and Fevertree, trade more like FTSE companies, Jowett says. There’s so much activity that trades are largely matched via order books, in contrast to some other stocks that might need a market maker to be on the other side of a trade. As the big get bigger, it means they’re distorting the data. “We sometimes had to exclude Asos from our trading data to get a clearer picture of what was happening in the broader AIM market,” Jowett says.

Not everything is rosy on AIM. Because there’s more liquidity, making it easier for speculators to put on negative bets, AIM is increasingly becoming a hunting ground for short sellers. Asos, whose market valuation reached a record £6.5 billion in March 2018, became one of AIM’s most-shorted stocks by the end of that year after unexpectedly cutting its sales outlook, according to IHS Markit Ltd. data. IQE Plc, another short seller favorite, was the target of research reports by London-based ShadowFall Capital & Research LLP as well as Carson Block’s Muddy Waters Capital LLC last year. There were more activist short campaigns targeting AIM companies last year than in any other year, according to data that Activist Insight compiled.

AIM companies can sometimes seem to suffer from a lack of management oversight. Some make costly acquisitions. Recent high-profile collapses were U.K. bakery chain operator Patisserie Holdings Plc and Bargain Booze owner Conviviality Plc.

Defenders are quick to point out that those failures had nothing to do with the AIM market itself, noting that construction company Carillion Plc imploded on the main market.

“We’re not operating a zero-failure regime,” AIM’s Stuttard says. “One of the big benefits of the public markets is that they allocate capital efficiently, and that’s their role. It’s not to prevent failure.”

Stuttard joined the London Stock Exchange’s listing department in 1994, the year before AIM was introduced, and 2019 marks his 10-year anniversary as the head of AIM. His tenure has already exceeded the length of his predecessor, Martin Graham. Stuttard says he’s proud of the contribution AIM has made to the U.K. economy.

Meanwhile, there may be a new Wild West in London: a standard listing on the main market, “which is very cheap with no corporate governance,” says Scott Evans, a researcher at the London Business School. “Three of the brokers I’ve talked to have told me they find it staggering that people want to invest in a lot of standard-listed companies because there’s no corporate governance whatsoever.”

Stuttard bursts into laughter at the prospect that increased interest in standard listings will spell the death of AIM. “Absolutely not,” he says. “I think we’ve got the right balance, both with AIM and the main market, and it’s for companies to decide which market they want to go to.”

Pham covers European equities and equity markets at Bloomberg News in London.

To contact the editor responsible for this story: Jon Asmundsson at jasmundsson@bloomberg.net

©2019 Bloomberg L.P.