Investors Should Stick to Their (Accounting) Principles

(Bloomberg Opinion) -- Net-off revenues, employee share compensation, fair value of convertible notes, deferred revenues.

Sea Ltd. offers many reasons why you should maybe ignore the standard way businesses report their financial results and focus instead on the Southeast Asian internet company’s preferred method.

To be fair, the Singapore-based and U.S.-listed company isn’t hiding its numbers based on generally accepted accounting principles, or GAAP. But Sea’s fourth-quarter report makes clear which lens it hopes investors will use to view the company's performance.

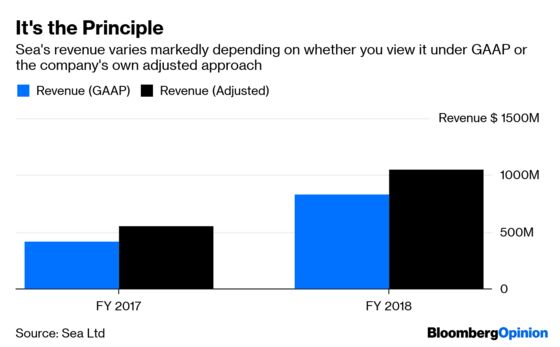

Leading the press release is news that full-year adjusted revenue climbed to $1.05 billion – and it’s noted that this is 10.4 percent higher than the company’s latest guidance. That’s an 89 percent increase from a year earlier. Dig down to page 7, though, and you’ll discover that the GAAP figure was more than 20 percent lower at $827 million. Interestingly, if the release had led with this figure the company could have correctly pointed out that GAAP sales doubled from a year earlier.

The discrepancy is even wider for the fourth quarter, where adjusted revenue is 37 percent higher than the GAAP measure.

Two things are behind the variance. At the digital entertainment unit, Sea uses adjusted revenue to approximate the cash spent by game users in the applicable period (a calculation that includes changes in deferred revenue). GAAP, by contrast, recognizes revenue over the anticipated life of the game in question. Sea’s approach allows it to show 63 percent growth in digital entertainment revenue for the fourth quarter, compared to just 46 percent under GAAP. There’s a 76 percent difference between the two dollar amounts.

Further, albeit smaller, differences come up at its e-commerce and other services businesses, where Sea adds back some revenues that are adjusted under GAAP to account for sales incentives. These changes not only affect the top-line number, but shift derived metrics such as marketing as a ratio of revenue. Investors watch this figure closely to see how efficient a company is at converting ad spend into revenue, and whether or not a business has momentum and word-of-mouth value.

At the bottom line, Sea is also suggesting you don’t concentrate on pesky costs such as employee share-based compensation and changes in the fair value of convertible notes. Attempts by companies to paper over share compensation is a bugbear of mine, because it’s akin to saying that we should ignore the fact that they pay their staff. Convertible notes also shouldn’t be ignored because financing is a real cost of doing business, and if a company wants to take the option of selling convertibles then it should accept the vagaries of accounting for them.

Sea isn’t alone in cherry-picking numbers and offering them as “adjusted” figures. Even Ford Motor Co. and Newell Brands Inc. take that approach, as my colleague Stephen Gandel noted recently. Research by Audit Analytics found that 277 companies in the S&P 500 Index give guidance using their chosen formula, he points out.

But there’s a reason why we have standards, and that’s so everyone is on the same page and we’re comparing apples to apples.

Investors shouldn’t forget that creating bespoke financial numbers (sometimes derided as “earnings without the bad stuff”) was the hip thing for tech companies 20 years ago. We all know how that ended.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.