Saudi ‘Whatever It Takes’ Runs into Oil Market's ‘Whatever’

(Bloomberg Opinion) -- Sometimes it can feel like your world is coming apart. In Saudi Arabia’s case, that is unfortunately somewhat true. Which is presumably why reports the country is considering all options to halt the slide in oil prices have bubbled to the surface over the past 24 hours.

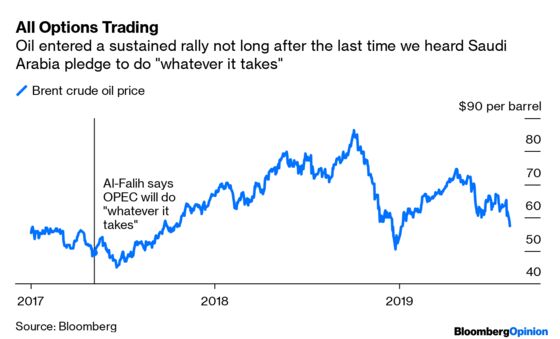

This isn’t the first time Saudi Arabia has deployed the whatever-it-takes weapon to beat back the bears. In May 2017, energy minister Khalid Al-Falih used that exact phrase when Brent crude had slipped below $50 a barrel. It sparked a brief rally, followed by a brief dip again, that ultimately segued into a sustained march toward $86 by the fall of 2018.

It’s different this time.

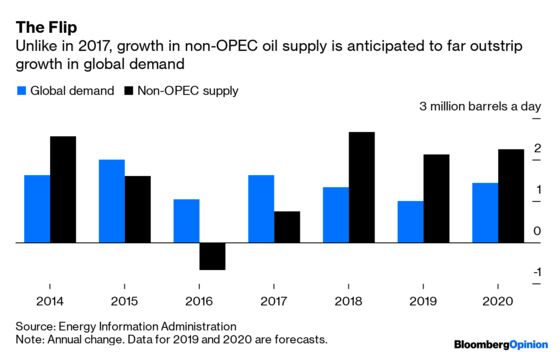

As bleak as things seemed to OPEC in May 2017, the organization actually had some favorable trends going its way. One of these was its own hesitancy to deliver on the production cuts agreed in late 2016. Apart from Saudi Arabia and the involuntary “discipline” of Venezuela and Angola, the rest of the group didn’t collectively get with the program until toward the end of 2017 (see this). In other words, there was plenty of room in May 2017 for many members just to do something, never mind whatever it took. Plus, U.S. sanctions against Iran were yet to kick in. Meanwhile, low oil prices were boosting global demand and suppressing non-OPEC supply, as U.S. shale operators were only just beginning to emerge from the shock of 2016.

None of this holds true today. Saudi Arabia already bears a disproportionate share of the OPEC+ cuts and relies on just a handful of others (including Russia) to maintain credibility on this front. Iran’s output is down by 1.6 million barrels a day already. And the balance between global oil demand growth and non-OPEC supply has reversed completely:

Signs of weakening economic growth are cropping up all over amid the escalating trade war between China and the U.S. This is the biggest obstacle to Saudi Arabia’s jawboning working this time. While Riyadh may be willing to do what it takes, both Washington and Beijing appear to be of a similar mind in their confrontation – and that is unambiguously bearish for oil.

It’s worth remembering that Al-Falih only recently said something along similarly aggressive lines when he mused about wanting to slash oil inventories by more than 200 million barrels. Yet the market remains unshocked and not the slightest bit awed (even with the shadow of actual conflict in Saudi Arabia’s neighborhood lurking in the background). Cutting supply further into a weakening market could leave Saudi Arabia with lower market share and not necessarily much extra revenue to show for it. This latest intervention appeared to bump Brent crude up from $56 a barrel to $58 overnight, but as of writing this Thursday morning it is back below $57.

On the same day Saudi Arabia’s apparent resolve made its way to the ears of the press, shale bellwether Pioneer Natural Resources Co. was extolling the virtues of low leverage and higher payouts to shareholders on an earnings call. Annualize the company’s latest quarterly buybacks and throw in its dividend increase, and Pioneer now yields 5.3% – more than Exxon Mobil Corp. Quite a remarkable change of approach for a fracker that was aiming for the equivalent of a shale moonshot in production growth only two years ago.

In other words, lower prices are having an impact in terms of moderating the shale boom. Letting them continue to do so would ultimately do much to rebalance supply with demand. The problem for Saudi Arabia is that “ultimately” is a ways away and, much as an outbreak of bankruptcy across Texas would help, the country’s own dependence on oil presents it with a more existential challenge. Hence, using language any central banker would recognize these days, Riyadh is trying to hold back a literal tide. And like the bankers, it may find a trade war exceeds its capabilities.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.