Saudi Crown Prince Says Jobs, Investment on Track as Doubts Grow

Saudi Crown Prince Says Jobs, Investment on Track as Doubts Grow

(Bloomberg) -- Saudi Arabia’s ambitious attempt to overhaul its oil-dependent economy is on track and indicators that suggest otherwise -- like a surge in unemployment and a slump in foreign investment -- will soon change direction, the kingdom’s crown prince said.

The jobless rate, now the highest in more than a decade at 12.9 percent, will start falling next year as higher oil prices permit more government spending, Mohammed bin Salman said in an interview in Riyadh.

During an 80-minute conversation, the kingdom’s de facto ruler sought to dispel suggestions that his economic reboot has stalled. Skepticism has grown amid delays in what was supposed to be the plan’s centerpiece, a $100 billion share sale in oil giant Saudi Aramco. The prince’s crackdown on business leaders accused of corruption, and his aggressive response to critics at home and abroad, have added to investor jitters.

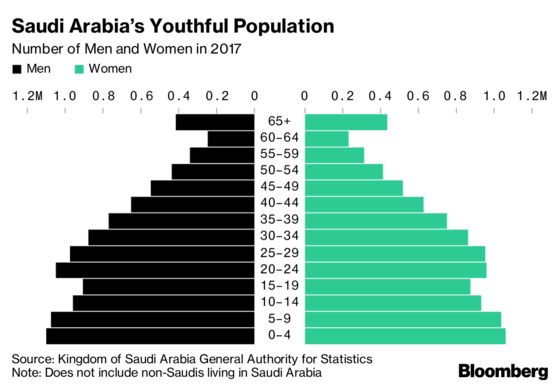

While Aramco has grabbed headlines, unemployment may be the most crucial measure for Prince Mohammed. He’s trying to trim a welfare system based on state distribution of oil revenues -- handouts have long been seen as key to Saudi Arabia’s stability. The 33-year-old crown prince aims to show that the kingdom’s youthful population can prosper without them.

Economists who support that goal have seen evidence of backsliding, citing plans to boost public hiring, and the reversal of pay cuts for civil servants. Prince Mohammed said private business will also be hiring, and he dismissed the criticism. “So what should we do?” he said. “Should we not use the money that is coming from oil?”

The prince said the figure he’s watching is the share of wages in the budget. He said it’s down from 50 percent in 2015 to 42 percent today, and “in 2020, I believe it will be below 40 percent.”

Read More on the crown prince’s interview...

|

Foreign direct investment into Saudi Arabia plunged about 80 percent last year, according to a United Nations report. That’s a net figure, and the prince said it was largely driven by the sale of a foreign-owned bank stake to Saudi investors. He said early data show a 90 percent rebound in FDI in the first half of this year. That would still leave the figure well short of 2016 levels.

‘Side Effects’

More broadly, Prince Mohammed said the central elements of his Vision 2030 plan, including the $100 billion Aramco sale and the effort to boost non-oil revenue, remain on course. He described the rise in unemployment as an inevitable side effect of the decision to change direction after the 2014 oil crash.

In the three years that followed, authorities slashed spending, cut subsidies and imposed value-added taxes. “You cannot do the restructuring without the side effects,” said Prince Mohammed, surrounded by a handful of advisers in his office. “The unemployment rate will start to decline from 2019.”

The prince shrugged off concerns -- shared even by some of his supporters -- that by raising expectations so high, he’s setting the entire project up for a fall if he can’t deliver.

“If you aim low, that means it’s an easy target. That means no one will try to work hard to achieve it,” he said. “We aim high. If we achieve 100 percent, great. If we achieve more, even greater. If we achieve 50 percent, great. Better than achieving nothing.”

The government expects the economy to expand 2.1 percent this year, after contracting in 2017 for the first time since the aftershock of the global financial crisis in 2009. Yet official estimates show growth staying below 2.5 percent through 2021. At that pace, many economists say, the economy won’t create enough jobs for young Saudis.

From 2000 to 2014, the Saudi economy grew an average of 4 percent a year, according to the International Monetary Fund.

Part of Prince Mohammed’s turn back toward government stimulus will be financed by the proceeds of what was billed as a drive against corruption. Dozens of royal family members and business leaders were rounded up and detained at the Ritz Carlton hotel in Riyadh, during a purge that sent shock waves through business circles inside and outside the kingdom.

Prince Mohammed said that more than $35 billion has been collected from settlement deals that officials predict will eventually reap more than $100 billion.

He said 40 percent of the amount “is being transferred in cash, and 60 percent is mostly assets.” The former is going to the Saudi treasury, Prince Mohammed said, while the confiscated companies and properties are being managed by a state entity called Istidama.

“Two years from now and the case will be totally closed,” he said.

--With assistance from Riad Hamade and Stephanie Flanders.

To contact the reporters on this story: Alaa Shahine in Dubai at asalha@bloomberg.net;Vivian Nereim in Riyadh at vnereim@bloomberg.net;Nayla Razzouk in Dubai at nrazzouk2@bloomberg.net

To contact the editors responsible for this story: Alaa Shahine at asalha@bloomberg.net, Ben Holland

©2018 Bloomberg L.P.