This U.K. Inflation Hedge Actually Offers No Relief From U.K. Inflation

This U.K. Inflation Hedge Actually Offers No Refuge From U.K. Inflation

(Bloomberg) -- Given the global nervousness about rising inflation, you’d think bonds specifically designed to hedge against the fallout would be on a roll.

But when it comes to U.K. index-linked debt, that’s not the case. And the signs are that the asset class will struggle to live up to its label for a while yet.

The securities, ostensibly designed to protect holders from the corrosive effects of rising consumer prices, have performed worse than any counterparts from the Group of Seven economies in the past month, losing investors 5.9%. For comparison, U.S. Treasury Inflation-Protected Securities, or TIPS, have gained 0.3%, while German linkers have dropped 0.6%.

The reason why Britain’s inflation bonds have performed so badly has much to do with their duration, a measure of their sensitivity to likely changes in interest rates. U.K. linkers have the longest duration relative to those from other developed economies. And with the Bank of England poised to become the first major central bank to raise borrowing costs, a move higher in yields make them less attractive as an inflation hedge.

“We see yields going up materially in the coming months due to inflation,” said Mark Dowding, the chief investment officer at BlueBay Asset Management in London. “The best inflation hedge for U.K. in this environment is to be outright short duration. With a small move in yields, investors could lose more in inflation-linked bonds than they do on conventional bonds because of their long duration.”

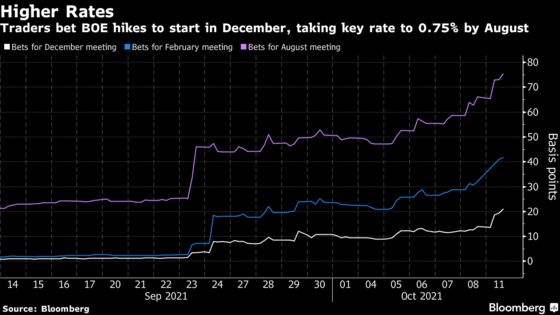

The Bank of England’s view that the current spurt in inflation will be transitory is coming under growing scrutiny from investors amid a combination of soaring energy prices, supply-chain disruptions and rising wages. Traders are loading up on bets for faster rate hikes, with money markets now fully pricing in the first move from the central bank of around 20 basis points by the year-end, a move that would lift Britain’s benchmark rate to 0.75% in the first half of 2022.

U.K. linkers would be more in favor if inflation remained elevated without much risk of policy tightening, such as in late 2007 and early 2008. That was when Britain’s central bank was grappling with the fallout from the global financial crisis at a time of high oil prices. Policy makers were eventually forced to cut interest rates.

Conditions are very different now. Bank of England Governor Andrew Bailey warned over the weekend of a potentially “very damaging” inflationary spike unless policy makers take action. Data from the U.K. tax authority released Tuesday showed payrolls rose back above their pre-pandemic levels last month, climbing by a record 207,000. Job vacancies increased to 1.2 million, also an all-time high.

Payouts from index-linked bonds increase with inflation, a key reason they are considered a good hedge against rising consumer prices. Investors can also profit from taking a directional bet that yields will fall and generate price gains or that breakeven rates -- a market-based gauge of inflation expectations -- will rise.

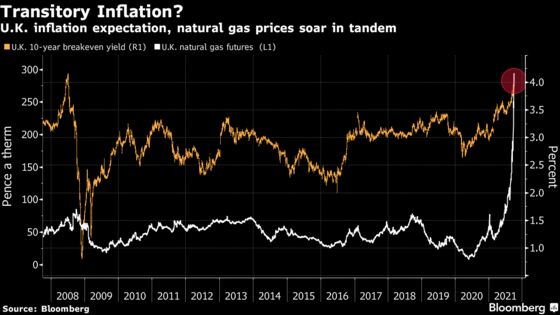

For Goldman Sachs Group Inc., two important market-based measures are already stretched, leaving little room for further profits. U.K 10-year real yields -- nominal yields minus inflation -- are currently about minus 280 basis points. The breakeven rate rose to 408 basis points, the highest since 2008, and is holding at 391 basis points.

“U.K. real yields are very low, making the cost of inflation protection quite expensive,” said Christian Mueller-Glissmann, the London-based managing director of portfolio strategy and asset allocation at Goldman. “A lot is already in the price and longer-dated U.K. linkers are vulnerable to rising real yields. Investors might find a better hedge from investing in commodities, which don’t have the same duration and valuation issues.”

©2021 Bloomberg L.P.