S&P 500 Bulls Make Peace With Valuations at 2018 Meltdown Levels

S&P 500 Bulls Make Peace With Valuations at 2018 Meltdown Levels

(Bloomberg) -- While the S&P 500’s valuation chart may be giving some investors flashbacks to the 2018 market meltdown, the bulls remain resolute.

Corporate earnings are expected to fall for a second quarter in a row as the reporting season begins in earnest this week. Meanwhile, share prices keep rising, with the benchmark gauge notching fresh records in the early days of 2020.

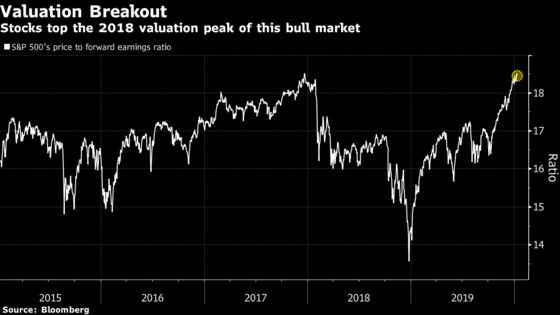

On the surface, such a disconnect can be unsettling. It has driven the S&P 500’s price-to-earnings multiple above the levels reached in early 2018, which preceded a drop of more than 10% in a matter of weeks.

While the valuation chart may look scary, some strategists have come out with explanations about why this time is different. They mainly point to the Federal Reserve. In 2018, the central bank was mired in a campaign of raising interest rates. Last year, they cut them three times.

“Investors are becoming comfortable with the notion that equities valuations can re-rate higher in an environment of benign inflation, accommodative Fed, stable to improving growth outlook, along with significant cash on the sidelines,” said Tom Lee, co-founder at Fundstrat Global Advisors LLC. Further expansions are likely, and each one-point increase in the price-to-earnings ratio is equivalent to a 5% gain for the S&P 500, he said.

Valuations have surfaced as a hot issue after the S&P 500 rallied almost 30% last year, with almost all the gains underpinned by multiple expansions. At current levels, stocks are trading at the richest valuations since the internet bubble burst.

The multiple-driven rally has had Goldman Sachs Group Inc. fielding client calls about parallels between now and the turn of the century. The firm’s strategists led by David Kostin suggested it’s too early to worry, pointing out that the S&P 500’s current forward P/E ratio of 19 is well below the multiple of 23 at the start of 1999.

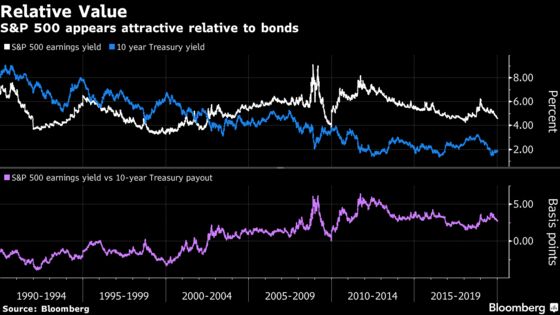

Stocks also are more attractively valued relative to fixed income, Kostin and his team argue. The S&P 500’s earnings yield, a measure that’s inverse of the P/E ratio, now stands about 340 basis points above the 10-year yield. By contrast, stocks offered a yield that’s 26 basis points below Treasuries 21 years ago.

At Bank of America, strategists led by Michael Hartnett see the potential for stocks to keep rising until the index’s forward P/E ratio hits 20. For early signs of market trouble, watch high-yield bonds, chipmakers, homebuilders and financial shares, as the underperformance of these groups served as prelude to a top in 2018, they say.

At some level, the elevation in multiples is the market’s way of predicting better earnings ahead. Such optimism doesn’t always pan out, as was the case in the late 1990s. In 2018, however, earnings did surge, partly helped by President Donald Trump’s tax cuts. S&P 500 profits ended the year about 10% higher than what analysts expected in January, according to data compiled by Bloomberg Intelligence.

This time, while growth is stagnating, analysts see a rebound coming. Profit expansion will accelerate to 9% this year from 1.5% last year and exceed 10% in 2021, estimates show. With the S&P 500 hovering at 3,265, stocks look expensive trading at 20.3 times 2019 earnings. But based on profits for the next two years, they look less stretched at a multiple of 18.6 and 16.8, respectively.

The market is “relying on the upcoming earnings season to deliver a positive tone, which seems more likely to come from revisions to guidance than recent revenues and profits,” said Michael Shaoul, chief executive officer at Marketfield Asset Management LLC. “Although some may dismiss this as ‘hope’ rather than ‘reality,’ it does seem likely that a good deal of corporate investment was put on hold between mid‐2018 and late 2019 and that a turn in corporate sentiment might actually have some measurable real world effect.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Richard Richtmyer, Brendan Walsh

©2020 Bloomberg L.P.