Royalty Pharma’s Dazzling Debut Leads to Tepid Street Views

Royalty Pharma’s Dazzling Debut Leads to Tepid Street Views

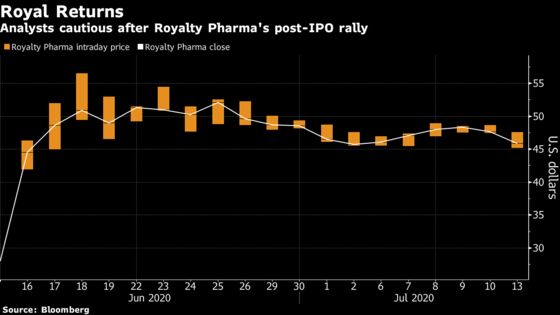

(Bloomberg) -- Coverage of Royalty Pharma Plc kicked off with a whimper instead of a bang after at least five analysts initiated with hold ratings and only three touted buy recommendations after one of the year’s largest U.S. initial public offerings.

Shares fell as much as 5% Monday, touching the lowest since June 17, after the lukewarm reviews. Citi summed it up for many on Wall Street: “Everything to love apart from the valuation,” analyst Andrew Baum wrote, noting a more than 60% surge for the stock since its June 15 debut. Royalty Pharma, which inks lucrative deals collecting future royalties on sales for drugs still in development, offers investors more than 12% rate of return on its capital investments, Baum said.

However, bulls pointed to the company’s size and influence. The company is a “leader in the royalty investing space” and the stock should be a new “core holding” for investors, BofA analyst Geoff Meacham said as he started coverage at buy.

Here’s what else analysts are saying:

Citi, Andrew Baum

The stock appears “fairly valued” against a net present value of $50 a share. Royalty Pharma “offers investors the opportunity to invest in a synthetic pipeline curated by an experienced capital allocation team.”

Management has been able to deliver an internal rate of return in excess of 12% and a cost of capital around 6%. Citi sees “competitive risks” pressuring those returns on future investments but thinks the Royalty team may be able to pull off a rate similar to historic levels.

Initiates coverage at neutral, price target $50.

BofA, Geoff Meacham

“Royalty’s financial flexibility and industry connections form a competitive moat.” The company controls 83% of the royalty investing space for deals of at least half a billion and all of the transactions that are over $1 billion.

“While changes in tax legislation or shareholder base could adversely affect Royalty’s historically low tax rate (we project a 0% tax rate in our model), this is not a near-term concern in our view, with Royalty having a strong incentive to manage the impact this would have to margins and net income.”

Starts at a buy with a price target of $55.

JPMorgan, Chris Schott

“Enviable position well reflected in valuation,” the analyst said starting coverage at neutral with a December 2020 price target of $50.

With “perpetual capital,” investment-grade credit, an efficient tax structure and experienced management, JPMorgan expects Royalty Pharma “to remain the leading royalty acquirer for the foreseeable future.” Shares, for now, are appropriately valued.

Morgan Stanley, David Risinger

The key bull and bear debate will be over Royalty’s internal rate of return. The bull case suggests the company continues to execute and “outgrow its competition” while the bear case suggests current biotech valuations are high compared to when Royalty signed its most profitable deals and new competitors are emerging.

Initiates at equalweight, price target $51.

©2020 Bloomberg L.P.