Risky Mortgages on Rise in Areas Most Vulnerable to Brexit

Risky Mortgages on the Rise in Areas Most Vulnerable to Brexit

(Bloomberg) -- Lenders are ramping up riskier mortgage lending in the north of England just as property values start to fall and interest rates increase.

That could be bad news for banks and home-loan providers in a region that’s already facing a hit to its wealth from the U.K.’s withdrawal from the European Union, no matter what kind of agreement is reached. It also threatens to hurt the economy there as borrowers cut back on spending to meet rising mortgage payments.

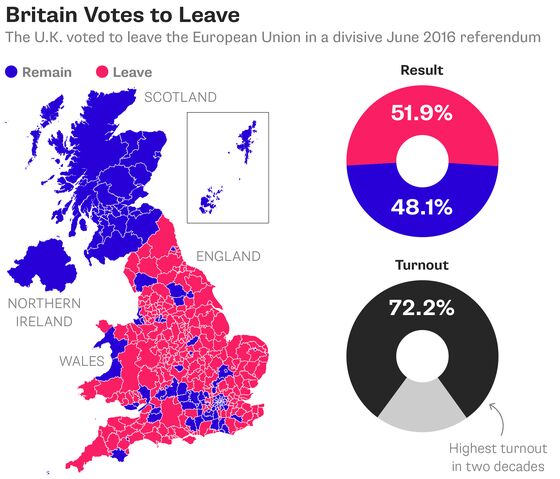

With the risk of a no-deal Brexit increasing, any subsequent squeeze on incomes and rise in unemployment could turn the region’s housing market from a slowdown into a slump. The north, where most people voted for Brexit, is more vulnerable than London to an economic downturn following the withdrawal because of its greater reliance on manufacturing for export.

“Brexit will be very bad news for all regions outside London, which is much more diversified and less dependent on the EU for its well-being,” said Jane Pollard, professor of economic geography at Newcastle University. “Levels of financial vulnerability will be particularly pronounced in areas like the north east” and “even people with quite reasonable incomes who are heavily indebted have little buffer if something goes wrong.”

Home prices fell almost 1 percent in the north west of England in June from a month earlier, and were down 0.3 percent in the north east and 0.5 percent in Yorkshire and the Humber area. Housing’s heading “for the doldrums,” Simon Croft, a broker in the spa town of Harrogate, said in a survey published by the Royal Institution of Chartered Surveyors this month, while realtors in Liverpool and Sheffield warned of a slowdown.

As high prices deter buyers and price declines ripple out from London, competition among lenders for those choosing to buy or remortgage is rising. The consequent pressure on margins contributed to a fall in pretax profit at Yorkshire Building Society in the first half and Nationwide Building Society in the three months through June.

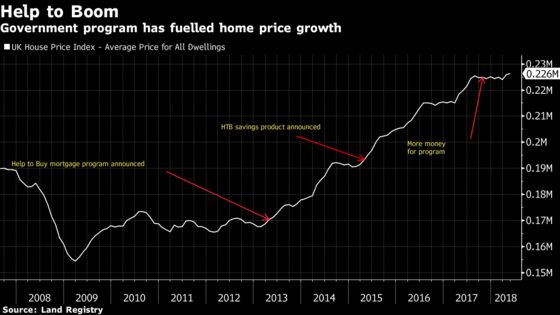

Lenders have been increasing the amount of low-deposit loans they give to homebuyers in recent years, as cheap borrowing rates and government programs to encourage purchases lift demand. That led Bank of England executive director Alex Brazier to say in April that credit supply for homeowners is loosening, a remark that so far hasn’t been heeded by banks when it comes to small-deposit borrowers.

Almost a third of homebuyers in the north west of England had a small deposit, defined by property surveyor e.Surv as 15 percent or less, when they bought or remortgaged their homes in June. That compares with just over a quarter in April. In Yorkshire, which the government estimates would be less affected by Brexit, more than 33 percent of borrowers had a low down payment.

Prices in the north east fell 0.6 percent in June from a year earlier, making it the second worst-performing region after London, according to data published by the Office for National Statistics on Wednesday.

Low-Deposit Lending Rises |

| Region | June | May | April |

| Yorkshire | 33.7% | 32.6% | 30.8% |

| North West | 32.1% | 32.1% | 26.6% |

| London | 16.2% | 13.8% | 14.9% |

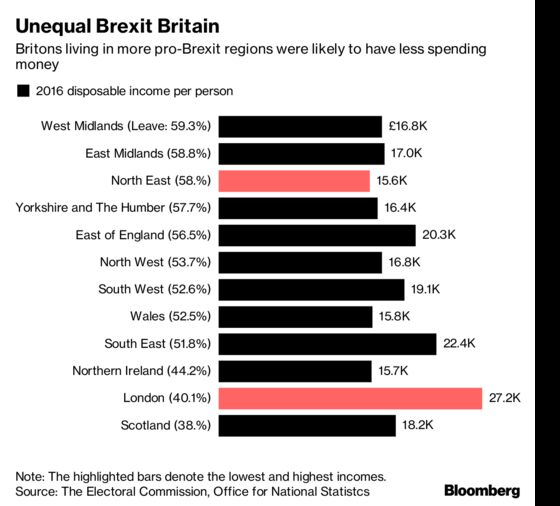

While U.K. homeowners don’t tend to default on their mortgages, even during times of recession, they often cut back on spending, potentially leading to a deeper downturn. That could hurt the north’s economy because people living there often have little money to turn to when times get harder. The north east, for example, has the lowest level of savings and investments in England, with almost 60 percent of adults having less than 10,000 pounds ($12,717). That compares with 47 percent in London.

“People will prefer to use the income and savings they have to pay the mortgage, so what’s likely to happen is they’ll cut from other expenses, starting with traveling,” said Ismail Erturk, a senior lecturer on banking at Manchester Business School. “GDP will be impacted in the first instance, rather than the housing market.”

There may be other problems stored up in the wider market. More vulnerable borrowers than previously thought may have been given mortgages in the U.K. in recent years because the proportion of high loan-to-income loans has been rising consistently over time, according to a BOE staff paper published in December.

Mortgage costs may also increase faster than interest rates because a cheap lending program operated by the central bank for lenders, some of which was used to fund home loans, ended earlier this year.

| What Our Economists Say A no-deal Brexit would have a bigger initial impact on London house prices, as it will have an immediate hit on sentiment and migration projections. It will then percolate to northern regions as the economic realities hit home and local economies that are more dependent on exports to the EU struggle more. -- Niraj Shah, Bloomberg Economics |

“The areas that’ll be hit worst if we leave the EU -- depending on the terms -- are the places that voted for Brexit in the first place, where there are lower skill and education levels,” said Paul Cheshire, professor of economic geography at the London School of Economics. “If I were a lender, I would be really cautious about giving low-deposit loans and be looking carefully at the borrowers’ circumstances.”

To contact the reporters on this story: Elizabeth Burden in London at eburden6@bloomberg.net;Neil Callanan in London at ncallanan@bloomberg.net

To contact the editors responsible for this story: Sree Vidya Bhaktavatsalam at sbhaktavatsa@bloomberg.net, Andrew Blackman, Paul Armstrong

©2018 Bloomberg L.P.