Riskiest Bank Capital Cheaper in Gulf Than for UBS or HSBC

Riskiest Bank Capital Comes Cheaper in Gulf Than for UBS or HSBC

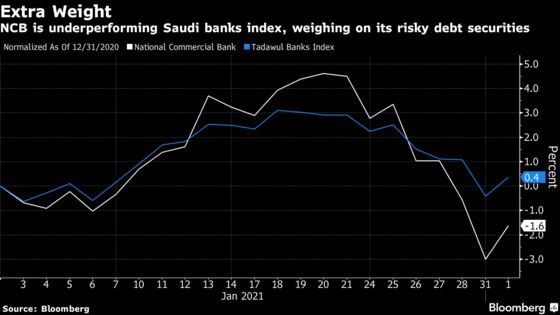

(Bloomberg) -- The sale by Saudi Arabia’s biggest bank of a high-risk type of bond -- at better rates than larger international peers -- is spurring concerns that investors are mispricing risk amid booming global valuations.

National Commercial Bank last month issued Additional Tier 1 notes at 3.5%, the lowest yield yet for the instrument from the region. That’s also cheaper than issuances over the past six months by higher-rated firms including HSBC Holdings Plc, UBS Group AG and Standard Chartered Plc. Also known as AT1, the notes are the first type of bank debt to suffer losses in a crisis.

Jeddah-based NCB, which is in the middle of a $15 billion takeover of a local rival, saw demand for four times the amount of the securities on offer at the Jan. 21 sale. The clamor defied the fallout from the global pandemic, a 14% drop in oil since the start of 2020 and a warning by Fitch Ratings in November that a jump in impairment charges may pressure banks’ creditworthiness.

Read more: NCB Revising Revenue Up and Provisioning Less on Early Signals

Introduced after the global financial crisis, AT1s are typically repaid by banks before call options expire to display their financial strength. Banks in the Middle East have issued $17.9 billion of AT1 securities, according to data compiled by Bloomberg.

There have been instances where AT1 bonds have blown up. India last year banned individual investors from buying the securities after seizing one of the nation’s lenders.

The rush to snap up NCB’s securities also followed decisions by two Omani lenders not to call AT1 instruments worth a combined $600 million last year, which may have been a result of tougher refinancing conditions, said Redmond Ramsdale, the London-based head of Middle East bank ratings at Fitch.

Buying NCB shares may have been a better bet because they trade at an average dividend yield of 3.9% over the past five years, according to Mohammad Ahsan, managing director of rates and fixed income at Mashreq Bank in Dubai.

Risk-Return

“Investors in the AT1 sukuk have opted for an inefficient risk-return payoff -- a lower yield at the same risk,” he said. Demand for the notes was driven by Shariah-compliant funds that cannot invest in equities.

“The issue size was overstretched for a debut AT1 deal, not only for NCB, but for the first such a sale in public market from Saudi Arabia,” according to Chirag Doshi, the chief investment officer at Qatar Insurance Co. in Doha, who manages $7 billion of portfolio assets. Pricing was aggressive relative to recent sales by global peers, he said.

NCB said it met all discretionary payments on local outstanding instruments through the pandemic. The decision to issue AT1s internationally “was based on its assessment of how best to efficiently manage the bank’s capital,” the lender said in an email.

This factored into the pricing and that the AT1s “are trading around par, has vindicated the assessment of investors,” NCB said.

Share Gains

NCB’s six-year AT1s traded at 99.85 to the dollar by 10:06 a.m. in London on Tuesday, while the lender’s share price rose as much as 3.9% on Saudi Arabia’s stock exchange, the most in more than a month. UBS’s AT1s, issued at 5.125% in July, last traded in January at 107.38, while those of HSBC and Standard Chartered are also at a premium to face value.

Yields that are higher than those available in other debt markets across most developed countries will continue to draw investors to investment-grade Gulf banks.

Fitch expects about $3.4 billion worth of AT1s to be called this year, compared with $3 billion last year, said Ramsdale. “We expect demand from investors for regional AT1 securities to remain strong.”

©2021 Bloomberg L.P.