Sydney Property Prices Face Further Drop, RBA Says

Sydney Property Prices Face Further Drop, RBA Says

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

Sydney property prices face “further downward pressure” due to an extended apartment construction pipeline as risks to Australian households have risen, the central bank said.

In its semi-annual assessment of the financial system Friday, the Reserve Bank cited the danger of a “sharper downturn” in the global economy. It said while banks’ profits remain healthy, increased scrutiny and weaker property and housing credit meant “greater-than-usual uncertainty” about their outlook.

“Risks to the household sector have increased over the past six months given weak housing market conditions,” the RBA said. “Indicators of financial stress remain low outside the mining-exposed regions. However, the value of housing loans in arrears has drifted up from very low levels.”

In the event of a spike in unemployment or sharper decline in property prices, the RBA would almost certainly resume easing to buttress households grappling with record debt and stagnant wages. Australian banks, the world’s most exposed to residential property, would come under further pressure; largest lender Commonwealth Bank of Australia is already reportedly working on a plan to to cut over 10,000 jobs amid slower earnings growth.

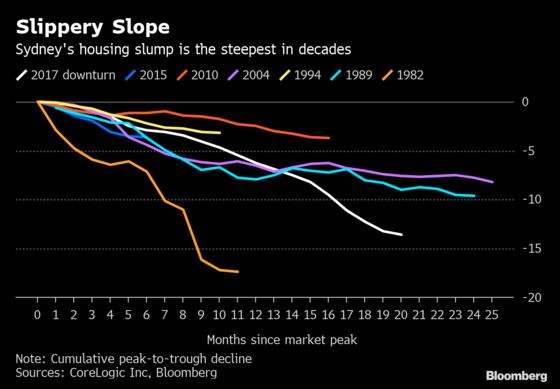

Australia is in uncharted territory right now as property prices in Sydney and Melbourne -- accounting for almost 40 percent of the total -- tumble while unemployment and interest rates remain low. Furthermore, the surge in the housing market between 2012 and 2017 means only buyers late in the boom are at risk of having a loan worth more than their home.

As a result, today’s Financial Stability Review focused heavily on highlighting the potential threats at home and abroad, while noting that at present there are no imminent dangers.

“Global economic growth has slowed and downside risks to activity seem to have risen,” the central bank said. “This increases the likelihood of a sharp decline in growth which could be detrimental to financial stability.”

The review warned that China’s “delicate balance” between stimulating a slowing economy and addressing financial stability risks “could falter.”

RBA’s Debelle Says Solving Jobs-GDP Puzzle Key to Rate Outlook

The RBA in February dropped a tightening bias in favor of a neutral stance for the cash rate, which has stood at a record-low 1.5 percent since 2016, in response to weaker consumer spending that dragged on economic growth. It’s now relying on unemployment at an eight-year low of 4.9 percent to ensure households stay solvent.

The central bank again highlighted Australians’ high debt levels, saying while households remain in a good position to meet their commitments, it increases the system’s vulnerabilities to a “sharp deterioration” in economic conditions.

The RBA estimated Sydney and Melbourne house prices remain 40 to 50 percent higher than in 2012. But, it said: “the large ongoing increase in the supply of apartments, particularly in Sydney, will put further downward pressure on prices.” Sydney property is down almost 14 percent from its 2017 peak.

No Buffer

While households have an average financial buffer of a little over 2-1/2 years on their mortgages at current interest rates, almost 30 percent of loans have no or little buffer, the report showed.

Meantime, in the western city of Perth and northern city of Darwin, property has slumped 18 and 27 percent respectively since their 2014 peaks. Underscoring the struggles of the former mining regions, the RBA said Queensland, Western Australia and the Northern Territory account for about 90 percent of all mortgage debt in negative equity.

Still, the RBA remained confident that the financial system is more resilient following a wide-ranging inquiry into misconduct and recommendations for improvement, higher capital levels and tighter lending standards.

It noted that banks’ stress tests indicate they can withstand double-digit unemployment and house-price falls exceeding 30 percent. It also said they’d held up well in real, if smaller, stress tests occurring in Western Australia.

To contact the reporter on this story: Michael Heath in Sydney at mheath1@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, Chris Bourke, Victoria Batchelor

©2019 Bloomberg L.P.