Ratings, Vote And Eskom Overshadow South Africa's Bond Plans

Ratings, Election and Eskom Overshadow South Africa's Bond Plans

(Bloomberg) -- South Africa may have to pay a premium if it taps international bond markets before a credit-rating review later this month and elections in May, according to investors who attended meetings with Treasury officials in London.

The discussions are moving to Boston on Wednesday after two days in London. Though they were billed as budget updates, the Treasury said last month it was considering selling as much as $2 billion of Eurobonds before the end March, depending on market conditions.

With U.S. rates hovering around the lowest in a year, selling debt may seem like a good idea right now. But uncertainty around the credit rating and election outcome, as well as doubts about the sustainability of the state-owned electricity company Eskom Holdings SOC Ltd., would add as much as 10 to 12 basis points to the price, according to Richard Segal, a senior emerging-markets analyst in London at Manulife Asset Management, which oversees $364 billion.

“Most of the discussion was about Eskom, ratings, the fiscal path and how to restore growth,” said Segal, who attended a meeting on Monday. “I came away more convinced that there are no easy answers. We would evaluate any new issue regardless, although timing wise we would expect more of a concession given the uncertainty.”

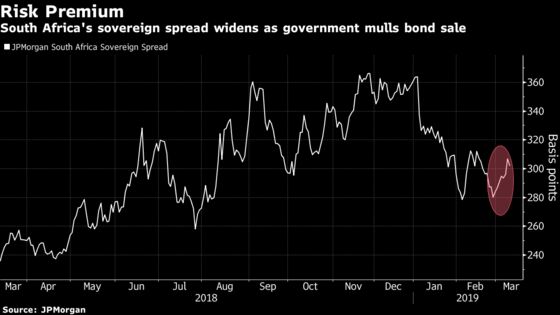

The premium investors demand to hold South African dollar bonds rather than U.S. Treasuries has widened 22 basis points since the beginning of March to 303 basis points, still well lower than the 366 it reached in November. The nation’s Eurobond due October 2028 rose on Wednesday, with the yield falling a basis points to 5.31 percent.

South Africa last tapped international markets in May, when it sold $2 billion of dollar bonds. While it said in October it was planning a second sale this fiscal year, adverse market conditions sparked by crises in Turkey and Argentina put that on hold. A drop in U.S. Treasury rates and renewed appetite for emerging-market assets have opened the window again.

Complicating the issue is the credit-rating review scheduled for March 29 by Moody’s Investors Service, the only major rating company still to assess South Africa at investment level. S&P Global Ratings and Fitch Ratings downgraded the country to junk in 2017. Much also depends on the outcome of the May election, where President Cyril Ramaphosa needs a strong mandate to push through economic reforms.

“I believe most investors will remain cautious of South Africa here, partly due to unattractive valuations, the Moody’s rating uncertainty, low growth dynamics and the risks involved in implementing a successful Eskom unbundling,” said Mohammed Elmi, an emerging-market portfolio manager at Federated Investors U.K. in London.

Eskom’s biggest union threatened a week-long shutdown at the South African power utility ahead of national elections in May. The National Union of Mineworkers opposes the government’s plans to split Eskom into generation, transmission and distribution units. Eskom has 419 billion rand ($29 billion) of debt, isn’t selling enough power to cover its interest payments and operational costs, and says it has 16,000 more workers than it needs.

South Africa has already met its target for foreign funding this fiscal year and is planning to raise another $8 billion over the next three years, according to budget documents. That means it can issue opportunistically, Tshepiso Moahloli, chief director of liability management, said last month. But it may be better to wait until investors have more clarity on the policy path, said Segal at Manulife.

“Everything will take time and they can’t do anything before the elections,” Segal said. “My perception is, no issuance before the elections in May.”

--With assistance from Colleen Goko.

To contact the reporter on this story: Selcuk Gokoluk in London at sgokoluk@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Robert Brand, Constantine Courcoulas

©2019 Bloomberg L.P.