Investment Robots Are Listening to CEOs and Reading Your Twitter Feed

Investment Robots Are Listening to CEOs and Reading Your Twitter Feed

(Bloomberg) -- In less than a decade, Danske Bank A/S changed auditors four times before a $230 billion money-laundering scandal hammered its share price.

It’s those type of red flags that PanAgora Asset Management Inc. wishes its factor-investing models could capture. So now it’s trained them to. The Boston firm has programmed robots to look beyond financial statements and market prices, trying to adapt cutting-edge data science to a brand of quant trading that before now had little use for it.

“We want to buy good-quality companies that are going to grow at a reasonable price,” said George Mussalli, a chief investment officer at the $46 billion manager. “But the question is how do you define that, and those definitions need to evolve over time.”

Statistical-arbitrage shops and macro funds have spent millions for exclusive data to uncover sources of consistent returns. Stock pickers famously count cars parked outside Walmart or track oil tankers to inform trades.

But peers in the traditional world of factors typically watched from the sidelines. The allocation styles, which slice up indexes to exploit behavioral anomalies like momentum and low volatility, were nothing if not time-tested. Why mess with success?

Now, newfangled inputs are everywhere as traders upgrade misfiring models. Everything from an executive’s tone and corporate culture to social media are sliced and diced for algorithmic intel in this corner of the systematic world.

At O’Shaughnessy Asset Management in Connecticut, quants are poised to incorporate patent data into their value portfolio to track intangible assets powering the knowledge economy. Over at BNP Paribas Asset Management, a team is investigating whether market sentiment derived from news stories can help define momentum strategies, or even serve as a standalone indicator.

Neuberger Berman Breton Hill, for one, is using credit-card data -- an established favorite among discretionary hedge funds -- to help estimate sales across consumer industries in real time.

“If you’re exactly following the way academics defined factors 30 years ago, then you’re using really old technology and I would just say no one would want to use an Apple IIe to manage their spreadsheets anymore,” said Ray Carroll, chief investment officer of the Toronto-based firm. “There’s just way more data available. If you don’t take advantage of all those things, I can guarantee you your competitors will.”

Booming Market

Funds of all stripes are paying up for fresh data to distinguish strategies from those popularized by smart-beta ETFs, which have more than doubled over the last five years to nearly $900 billion. The market for big data and related services overall is estimated to be worth $200 billion next year compared with $130 billion in 2017, according to a JPMorgan Chase & Co. report.

At its heart the quant philosophy tracks inputs researched by academics like Nobel Laureate Eugene Fama and Ken French. But defining those attributes has always been how funds proved their mettle, with some more wedded to purely mathematical nodes than others. Each generation seeks to refine old indicators and unearth new ones.

“You run your five Fama-French factors and hope that the historical performance holds up. But it just doesn’t work anymore -- there’s just too much capital,’’ said Benjamin Dunn, president at Alpha Theory Advisors. “Investors are choosing a wider mosaic of factors to look at.’’

To Saeed Amen, this industry push to identity trends beyond the purely financial spurred him to write a book on alternative data due next year.

“If you just look at price data in isolation, you’re not getting the full picture,” said the founder of Cuemacro Ltd. He’s responding to trends such as traders gathering satellite images to predict retail trends and using Twitter to forecast jobs data.

A team at Deutsche Bank AG has developed models that quantify a company’s intangible assets like corporate culture and product development by using natural-language processing to scan regulatory filings and news stories. The bank is now working on developing new products based on the insight, according to Spyros Mesomeris, a quant research chief at Deutsche.

Data Deluge

The task is far from straightforward. There’s the tedium of organizing the numbers and mapping them onto stocks, while building data sets with sufficient breadth and history needed for trading. Even fielding sales pitches is becoming tiresome. There are now more than 400 data providers compared with about 100 in 2008, according to AlternativeData.org. Bloomberg LP, the parent of Bloomberg News, provides clients with access to alternative data.

AQR Capital Management, a pioneer of factor investing, has been skeptical, while alternative data only informs some strategies at PanAgora. After all the factor strategy exploits tried-and-tested sources of return, and practitioners aren’t sure new ones can be easily discovered.

Even Patrick O’Shaughnessy at OSAM doubts stuff like satellite imagery will prove the industry’s saving grace.

“Alternative data may be useful for extending advantages in traditional factors -- value investing or momentum may get better because of new data but it will still be value and momentum -- but probably not for building new factors,” he said from Stamford, Connecticut.

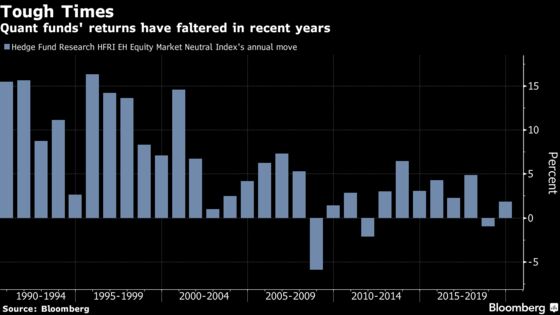

But the systematic money can hardly afford to dismiss opportunities to crack trading signals conspicuous to the human eye but blind to factor models. High-profile closures of several computer-driven funds and the dispiriting performance of quant-like hedge funds have underscored the urgency of upgrading their approach.

“I don’t see alternative data as a replacement of traditional academic metrics -- I see it as an enhancement,” said Deutsche Bank’s Mesomeris.

--With assistance from Samuel Potter.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Sid Verma, James Hertling

©2019 Bloomberg L.P.