Quants Now Trade Exotic Stuff. But Can They Handle Illiquid?

Quants Now Trade Exotic Stuff. But Can They Handle Illiquidity?

(Bloomberg) -- The search for elusive alpha is sending a handful of computer-driven hedge funds trawling the remotest corners of financial markets.

They’re a subset of the trend-following strategies known as commodity trading advisers, or CTAs, that were popular when central banks pushed up stocks and bonds over the past decade. Now a few of them are seeking uncorrelated returns and a little extra alpha in anything from cheese and Turkish scrap steel to obscure chemicals or eggs in China.

With at least $7 billion invested across at least eight such funds, up from one fund and $1 billion five years ago, these alternative CTAs remain very much a niche strategy. But trend-following funds have been blamed in the past for amplifying selloffs in some of the most liquid assets, because they tend to rely on similar models. As more money is targeting much smaller markets, even some managers warn of risks if funds pile into the same trade or unforeseen events cause a selloff.

“These assets are less arbitrated and subject to wider moves,” said Philippe Ferreira, a Paris-based senior cross-asset strategist at Lyxor Asset Management, which invests in hedge funds.

Investors have flocked to exotic trend followers because they promise diversification and a way to shield portfolios from broad market shocks. Electricity markets in Northern Europe, for instance, may be relatively more dependent on rainfall in Norway than on global market trends. Prices of purified terephthalic acid, a chemical used to make polyester, depend on sales of yoga pants or plastic bottles.

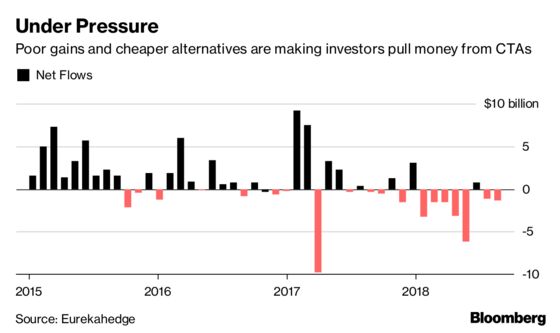

Worst Loss

“We’re looking for exposure to markets that are more likely to be less correlated with broad market indices and global economic factors," said Antoine Forterre, co-Chief Executive officer of the AHL unit of Man Group that runs computer-driven funds.

For a long time, there was only one prominent fund -- AHL Evolution, run by the quantitative unit of Man Group Plc -- targeting such niche markets, though some firms included exotic assets in their main funds. It’s still the largest fund in the group and has returned 416 percent since its start in 2005 with no down year. The Eurekahedge CTA/Managed Futures Hedge Fund Index has risen about 128 percent during the period.

| Fund | YTD Return | 2017 Return | Launch |

|---|---|---|---|

| Gresham Quant ACAR | 26.2 | 12.9 | 2017 |

| Systematica Alternative Market | 2 | 24.1 | 2015 |

| Aspect Alternative Markets | 2.9 | -- | 2017 |

| Florin Court* | 2.4 | 7.7 | 2017 |

| AHL Evolution Frontier | 1.9 | 16.4 | 2015 |

| Devet Capital Alternative Markets | 0.4 | -- | 2018 |

| AHL Evolution | 0.1 | 17.9 | 2005 |

| GAM Systematic Discovery Fund | -- | -- | 2017 |

| SG Trend Index | -3.2 | 1.5 |

YTD returns through September

*Florin Court switched strategy to focus on exotic assets in April last year

Source: Website, investor reports

Since last year, five new funds have joined the fray from money managers such as Aspect Capital and GAM Holding AG. One reason is that traditional trend-following funds struggled this year as volatility returned and some investors shifted to cheaper smart beta funds.

After attracting net inflows of about $51 billion in three years through 2017, investors pulled about $14 billion this year, according to Eurekahedge. The strategy suffered its worst loss in years in February when a particularly popular trade -- a bet that volatility would remain low -- imploded in sudden market selloff. They are suffering another tough month in October, with the SG Trend Index, which tracks returns for 10 such funds, down 5.4 percent through Oct. 18.

Their alternative siblings, by contrast, have mostly made money this year, attracting investors. The latest stamp of approval came from the pension funds for New York City’s police and fire departments, which in August allocated a combined $134 million to London-based Florin Court Capital that runs one of these money pools.

Cambridge Associates, a consultant which guides some of the world’s largest pensions and endowments on where to invest, approved alternative market fund Gresham Quant ACAR earlier this year, according to people with knowledge of the matter. CERN Pension Fund, which invests for employees of the European nuclear physics research organization, allocated $10 million to the AHL Evolution last year even as it cut exposure to hedge funds, according to its annual report.

Spokesmen for Cambridge Associates and Gresham Investment Management declined to comment.

‘First Mover’

Critics fear that their popularity could become their biggest enemy as more money chases higher returns in relatively small markets. Often, firms will use over-the-counter contracts to place their bets because there’s no exchange where futures on these assets are traded. That means fewer buyers when markets go south, and it means fewer data points for the computer models to build on.

Fund mangers acknowledge that crowded trades in alternative markets could pose a risk, but they argue the strategy will always be a niche, the icing on the cake for sophisticated investors who understand the illiquidity risk. They also say that such funds will be capped because there’s a limit to how much money each can put to work in their exotic markets.

“Growth of such strategies should be naturally limited by the liquidity and tradability of the underlying alternative markets and the first mover is likely to take all," said Nicolas Roth, head of alternative assets at Geneva-based investment firm Reyl & Cie.

‘More Persistent’

“Some of the funds launching into this space are probably surfing the marketing gimmick," he said, cautioning investors to be “wary of the package and look into the engine."

Scott Kerson, head of systematic strategies at Gresham Investment Management, which runs one of the top-performing funds this year, says there’s another reason why returns for exotic CTAs may prove resilient. While traditional funds often trade futures among themselves, exotic quants tend to deal with an actual producer or consumer who will ultimately have a use for the asset.

“They are an inherently different type of participant, and are trying to solve a different problem,” Kerson said. “We aren’t competing over the same source of returns, and that means those returns may be more persistent.”

To contact the reporter on this story: Nishant Kumar in London at nkumar173@bloomberg.net

To contact the editors responsible for this story: Sree Vidya Bhaktavatsalam at sbhaktavatsa@bloomberg.net, Christian Baumgaertel

©2018 Bloomberg L.P.