Private Equity Tests Ground for Looser Loans in Australia

Private Equity Tests Ground for Looser Loans in Australia

(Bloomberg) -- Private equity firms are increasingly seeking loans with slacker terms to help fund buyouts of Australian businesses, creating a testing ground for these kinds of deals in the Asia-Pacific leveraged finance market. But it’s not without risk.

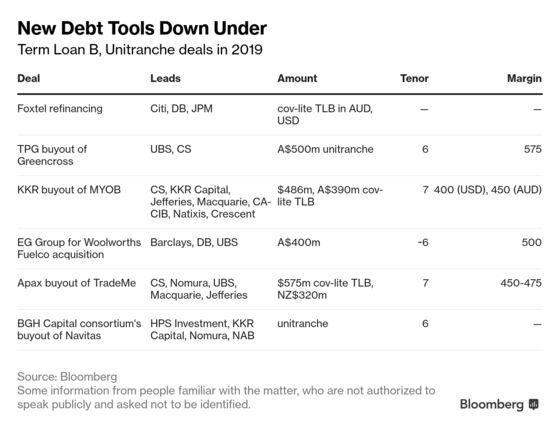

Sponsors such as TPG Capital and KKR & Co. are turning to so-called unitranche financing and covenant-lite term loan B, which are more common in the U.S. and Europe. These sorts of funding are typically characterized by higher leverage, longer tenors, little amortization and fewer lender protections.

“We found a lack of covenants and more pointy leverage in some of the transactions that you would have seen in the U.S. and Europe coming into the Australian market,” said Bob Sahota, the co-founder of Revolution Asset Management, an investor in leveraged buyout loans. “We don’t say we’ll never do a covenant-lite deal, but for us, it has to be for an absolute rock-solid credit.”

“In the U.S., covenant-lite started with the best and brightest credits and the same terms started to be given to smaller companies,” Sahota said in an interview in Sydney. “If that happens in Australia, you’re better off not investing,” because you don’t get to test the safeguards in covenants until the company starts to underperform or there’s an economic downturn, he said.

Private capital available for fund managers globally reached $2 trillion as of June 2018, with the proportion targeting Asia doubling to 18 percent from 2006, according to data from Preqin. In Australia, an array of asset managers have been raising new funds in recent months to invest in private debt, which has primarily been the domain of banks.

- Revolution Asset in December held the first close of its Private Debt Fund I, which partially invests in leveraged buyout loans in Australia and New Zealand, at around A$200 million ($142 million). Further closes are scheduled for April and June.

- Perpetual Ltd. is seeking as much as A$400 million for a fund that will invest in credit and fixed-income assets.

- Metrics Credit Partners in March raised A$300 million for a fund that will buy private credit instruments, with a focus on sub-investment grade.

“We’ve seen a significant broadening of the investor base for Australian dollar Term Loan Bs, with increasing interest coming from institutional investors located both onshore in Australia and offshore in Asia,” said Andrew Ashman, Singapore-based head of loan syndicate for Asia Pacific at Barclays Bank Plc.

Unitranche fuses senior and subordinated parts of debt financing under a single agreement and is typically bilateral or involves fewer lenders than traditional buyout loans or corporate facilities.

About 80 percent of leveraged loans outstanding globally have “covenant-lite" features with fewer financial checks, compared to 15 percent a decade ago, S&P Global Ratings said in a March 12 report.

With the vast firepower of private equity groups and private credit there’s a lot of capacity for deals, Gary Stead, managing director in Sydney at HPS Investment Partners LLC, said at a conference in Sydney. His firm is active in offering unitranche products in Australia. “The question is, when do we start to see bad transactions where the supply exceeds demand?”

More Views

- “Offshore investors are attracted to the stable legal jurisdiction and the opportunity to gain exposure to Australian credit in size,” said Barclays’ Ashman.

- “There is strong investor preference for defensive, stable sectors and for companies with low volatility in earnings,” he said. “Certain sectors, such as retail and mining services, will remain challenging.”

- “Hopefully covenant-lite isn’t a permanent feature of the market in Australia, but if it is, we’ll just do less of it and pick the credits that we really like,” Revolution’s Sahota said. “We don’t extend those terms to every company.”

To contact the reporter on this story: Mariko Ishikawa in Sydney at mishikawa9@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Beth Thomas, Ken McCallum

©2019 Bloomberg L.P.