Private Equity Binge Brings New Life to Wealth Advisers

Private Equity Buying Binge Brings New Life to Wealth Advisers

(Bloomberg) -- John Egan’s business is helping people plan for retirement. So it was logical he’d make moves to prepare for his own.

Egan struck a deal in 2016 to sell a majority of his firm to HighTower Advisors, a private equity-backed aggregator of registered investment advisers who collectively oversee more than $70 billion.

HighTower now manages back-office arrangements for Egan’s Madison, New Jersey, office while he spends more time recruiting clients and works out with a personal trainer. Since the deal, Egan’s assets under management have soared 50% to $475 million and he’s lost 15 pounds. He said he also hangs out more at home in the 15 hours a week HighTower has freed up.

“My wife said she wished it was only eight hours,” said Egan, 59.

Egan’s new life is part of a consolidation sweeping the wealth-advice industry, a trend largely driven by companies funded by private equity, like HighTower. Advisers managing $2.4 trillion are expected to sell, merge or open shop over the next 10 years, according to market researcher Cerulli Associates. Two-thirds of the deals will be driven by firm founders preparing for retirement, Cerulli said. Others are seeking capital for growth or startups. The debt frequently used to make the purchases is one reason some advisers are reluctant to sell.

Registered investment advisers, a $4.8 trillion industry, have averaged 10% compound annual growth in assets for the last five years, according to Cerulli. The 10 largest aggregators are growing at more than twice that pace. Their fees, typically 1% of assets under management, have remained steady even as mutual funds and brokerages keep cutting theirs.

Record Deals

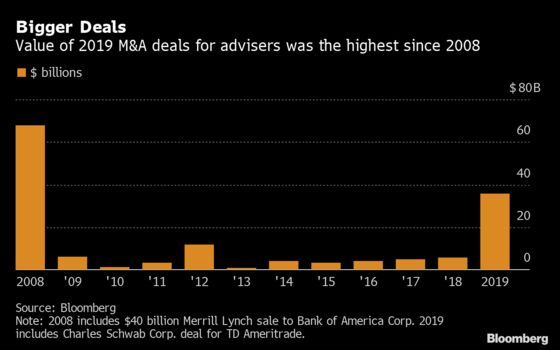

At least 85 firms traded hands in 2019, trailing only the record 92 transactions in 2018, according to data compiled by Bloomberg. Seven more deals were announced in the first week of 2020. Valuations also are at all-time highs, especially for sellers like Egan who agree to stick around and work to grow their businesses.

“In the last three to five years, you’ve see these super-regional firms with multiple offices finding leverage and momentum,” said John Langston, managing director of Republic Capital Partners, a Houston-based investment bank specializing in wealth-manager deals. “They have every advantage over their smaller competitors in size and scale.”

The wheeling and dealing may not last. Bank-based wealth managers, from whom many independent advisers split, aren’t standing still against the competition. Bear markets and industry disruptors from discount robo advisers to retail giants like Vanguard Group and Charles Schwab Corp. could change the value proposition.

Untested Models

“These consolidator models are relatively untested in a market downturn or even a more turbulent market,” said Marina Shtyrkov, a research analyst with Boston-based Cerulli.

Six out of the 10 largest consolidators of registered investment advisers have received external funding from private equity investors or venture capital firms, according to Cerulli. Other investors include banks, such as Goldman Sachs Group Inc., which spent $750 million for United Capital last year, and asset managers like Franklin Resources Inc., which said this month it would buy Athena Capital Advisors.

Adviser acquisitions, like most private equity transactions, rely heavily on leveraged-debt financing. HighTower was recapitalized and pledged $100 million for new strategic investments under a 2017 agreement with Thomas H. Lee Partners, a Boston-based private equity firm. HighTower currently has $430 million in debt due in January 2025, according to the company.

Chicago-based HighTower owns stakes in 107 advisory businesses in 34 states with $72.7 billion in assets. The firm provides cash to help the advisers grow their businesses and also offers support services. It lets its new affiliates keep their independent identities, which means clients don’t notice any change, according to Egan.

Flip It

Steve Morton chose to sell his firm in 2018 to another aggregator, partner-owned Captrust Financial Advisors. He said he selected Captrust because, unlike private equity-backed consolidators, Captrust has no debt and won’t be subject to a forced sale or refinancing.

“Nobody’s trying to flip it or pump earnings short term,” Morton said. “Everybody’s in it for the long term.” His Greensboro, North Carolina-based firm increased assets more than 16% to almost $470 million since the sale.

Like Egan, Morton said he can spend more time with clients -- even while he takes 12 weeks of vacation a year. He charges lower fees for trades and other services because Captrust’s scale gives it more negotiating leverage with vendors than his solo practice. Morton, 66, said he can ease into retirement while continuing to woo new clients.

“I’m looking forward to 2020 being a really fun growth year for us,” he said.

Neither Egan and Morton would disclose the value of their deals, but both said they received equity in the acquiring firm.

Meanwhile, the big players have been dealing. In November, Advisor Group, which operates a broker-dealer network with more than 7,000 advisers backed by New York-based buyout firm Reverence Capital Partners, agreed to pay $1.3 billion for publicly traded Ladenburg Thalmann Financial Services Inc. The transaction was financed with $875 million in debt, according to a Dec. 26 filing.

Big paybacks aren’t guaranteed. Focus Financial Partners, an aggregator whose largest shareholders are private equity firms Stone Point Capital and KKR & Co., has traded below its July 2018 $33-per-share initial public offering price since May. A key long-term issue is the level of leverage, according to analysts at Goldman Sachs.

Many wealth advisers worry that consolidation could lead to a misalignment of interests as founders lose control or private equity backers try to squeeze out profits. A survey released in December by HighTower found 70% of advisers said they are “anxious or worried” about the thought of partnering with an aggregator.

Not Egan. He said he sleeps easier now that HighTower is handling office leases, tech support and compliance.

“I’m back to spending 85% of my time with clients,” he said. “I’m back to loving what I do.”

To contact the reporter on this story: John Gittelsohn in Los Angeles at johngitt@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Bob Ivry, Josh Friedman

©2020 Bloomberg L.P.