Power Swing Puts Borrowers in Ascendancy in European Loan Market

Power Swing Puts Borrowers in Ascendancy in European Loan Market

(Bloomberg) -- Europe’s leveraged loan market swung from fractious to frantic during the third quarter. Fierce demand again overtook supply in September as lenders eyed a weakening pipeline and scrambled for assets. But widening CLO liabilities and potential triggers for volatility may mean that borrowers won’t have it all their own way in the final months of the year.

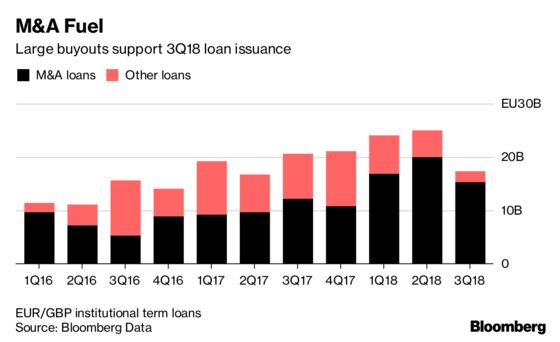

Third-quarter new issuance of 17.4 billion euros ($20.1 billion) puts the market about 17 percent ahead over the same period last year, so it ought to be on track to beat last year’s total. But the flow of M&A transactions is expected to slow, having powered the market all year.

- European institutional loan issuance: EU66.5b YTD vs EU77.8b in FY2017

- M&A-linked issuance: EU52.2b YTD vs EU41.8b in FY2017

“The pipeline looks lighter than normal for this time of the year which partly explains the technical demand we are witnessing at the moment,” said Kristian Orssten, head of EMEA debt capital markets at JPMorgan Chase Bank NA.

At the same time, a long queue of buyers are hunting for assets to fill their portfolios. These are not only the numerous established and newly arrived CLOs, but also managers of burgeoning unlevered loan accounts including some from investors based in parts of Asia.

"We hear there are a significant number of insurance, pension and sovereign funds actively requesting separately managed account proposals from managers," said Joseph Bishay, head of European leveraged finance capital markets at Bank of America Merrill Lynch.

Reflex Action

Based on this outlook for supply and demand, the fourth quarter is shaping up to be a borrower-friendly market, to investors’ deep disappointment. Their mid-year coup has ended sooner and more abruptly than they were expecting.

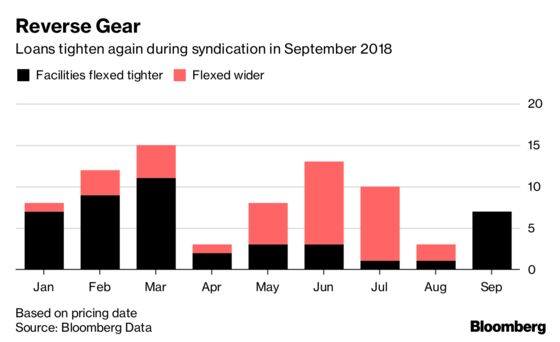

As market conditions swung, companies that raised leveraged loans in July had a very different syndication experience to those that came in September.

- Seven loan facilities priced in September after flexing tighter, the most since March.

Before the August break, investors hung back from new deals, and successfully demanded higher pricing and better documentation. Some sold paper into a softening secondary market to make room for new assets, others hoarded cash in the expectation of a huge autumn pipeline and thereby squeezed liquidity.

But when September rolled around, bringing the long-awaited LBOs for Thomson Reuters Corp.’s carve-out Refinitiv and AkzoNobel Specialty Chemicals, buyers flooded in again.

Demand from core loan investors for those deals was boosted by non-traditional players, attracted by the scale and liquidity of these deals. Both raised huge oversubscriptions across their U.S. and European bonds and loans, allowing them to make minimal changes to documentations and to flex pricing tighter. Lenders were scaled back more than expected, and saw the paper fiercely bid on the break amid a rapidly rising secondary market.

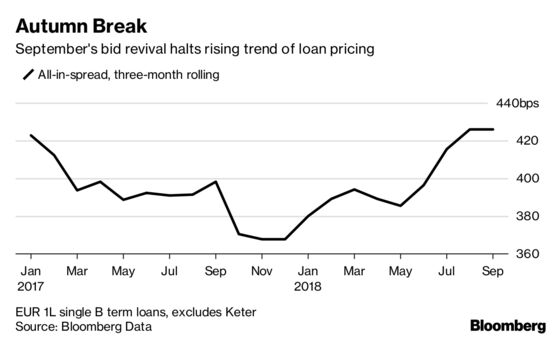

Although average new-issue spreads have risen versus the second quarter, many borrowers found in the aftermath of the two jumbo LBOs that they could cut margins by around 50 basis points or more versus where they launched.

- Avg all-in spread 426 bps in 3Q18 (excluding Keter), vs 396 bps in 2Q18, for single B first-lien EUR-denom. loans

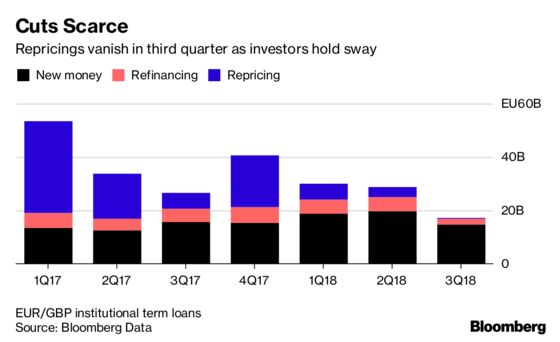

Given an apparently light M&A pipeline and a plethora of loans bid above par, the way is now open for opportunistic deals in the fourth quarter. These could include dividend recapitalizations for companies that have delevered or refinancings to switch existing second-lien loans into first-lien.

There could also be some repricings. One of the last deals to launch before the third quarter closed was a repricing request for cross-border borrower Dealogic LLC and if pricing conditions remain very tight through the coming weeks others may try to follow suit. But investors hope for relatively few of these requests since the most expensive transactions of the year are still within their call protection period.

One Way or Another

Despite all this, it’s not a given that the market will be a one-way bet in borrowers’ favor. Bankers and fund managers point to several reasons to think that the fourth quarter could be more nuanced.

First and foremost, the cost of CLO triple-A liabilities has widened during the third quarter. New vehicles priced at 90-100 basis points in September, narrowing the gap between the cost of servicing CLO notes and the incoming interest payments from the loan portfolio.

- Average spread for European CLO triple A notes: 92 bps in 3Q18 vs 80 bps in 2Q18.

This won’t stop CLOs from printing but they may come more slowly with the thinner arbitrage impeding the bid from this vital part of the investor base and making the supply-demand picture more complex.

“We are being quite cautious about how deep we go into some of the tightly priced paper. The fourth quarter will be all about supply and demand again, but it’s less easy to dissect what will happen. There are conflicting forces acting on the market as CLOs liabilities widen and loan supply slows,” said Martin Horne, head of global high yield investments at Barings.

On the documentation front, meanwhile, Refinitiv and AkzoNobel Specialty Chemicals may have steamrolled over attempts to improve aggressive terms, but arrangers don’t expect lenders to be so compliant on every European deal.

“I still expect to see an ongoing debate for European transactions around structure and covenants -- especially in loans -- as we have had all year,” said Tim Morgan, head of high yield syndicate at HSBC Bank Plc in London, adding that there will be flexibility for better credits.

Similarly, on opportunistic deals, an arranger describes the market as "quite fragile" and says that sponsors shouldn’t conclude from new-issue oversubscriptions that every opportunistic deal can get done.

Beyond the internal dynamics of the market, spells of volatility could be provoked by rising rates, Brexit negotiations, Italian budget woes, trade tariffs and other factors. And the more large or cross-border deals there are in the market, the more likely it becomes that European loans feel some impact from broader turbulence.

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

--With assistance from Gianluca Ansaldi.

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, V. Ramakrishnan

©2018 Bloomberg L.P.