Powell’s Gut Punch to Equities May Be a Belly Rub: Taking Stock

Powell’s Gut Punch to Equities May Be a Belly Rub: Taking Stock

(Bloomberg) -- The eye of the needle to thread can’t be narrowed further.

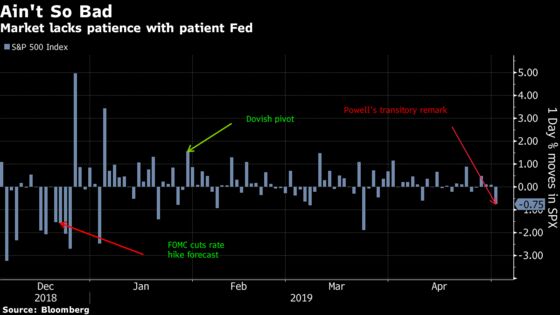

Fed Chairman Powell, as history has told us before, failed to deliver in the short term for the stock market (not that that is his job), adding yet another down session for equities on decision day (just one of the 10 meetings over which he has presided led to the SPX ending higher). And we can be honest, it wasn’t pretty for stocks -- this wasn’t was a nebulous result, despite the statement’s wording appearing dovish at first blush. Stocks had their second worst day of performance under Powell’s meeting tenure, ironically beat out for the top (most negative) spot by the December meeting which set the stage for the "pivot" in January. Despite that "hawkish hike" in December, as it was referred to at the time, the FOMC had actually moved the other direction, lowering their forecast for the number of hikes expected in 2019 to 2 from 3.

The consensus from the FOMC meeting was that prospects for a rate cut (did we really think that was coming?) are now fading. Fed fund futures were anticipating a near 24% chance of a rate cut in June, and a slightly higher chance (32%) in July -- those are now ~6% and 16% respectively. The culprit? The idea that inflation will at some point return -- “transitory” were his words used to describe impacts that are keeping inflation below target.

But should equity investors be worried? Powell made overtures to some of the most concerning aspects of the 4Q downturn having dissipated -- mainly that data from China and Europe was showing some improvement. Is that a reason to throw the baby out with the bath water?

The knee jerk reaction should be expected -- money came out of growth names (with the exception of Apple and select positive earnings stories like the cruise liners and hotels) and into defensive sectors. It’s not hard to blame the selling, though you can argue it may be more of an air pocket of buyers than mass panic.

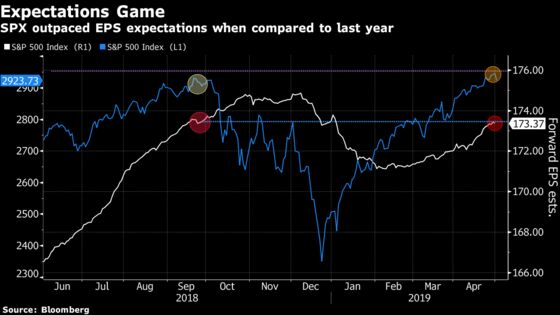

This is being borne out early with S&P futures higher by nearly 10 handles (most of the world’s indices are still processing yesterday’s news after being closed for May Day). Many strategists have long noted the risk/reward at these elevated levels leaving much to be desired. But by and large, earnings season has exceeded the heavily lowered expectations, and as shown below, its possible to argue large caps may have gotten a bit ahead of themselves.

The S&P, in setting in new records, exceeded last year’s levels when blended forward EPS expectations were at approximately the same level. Is it so bad? Rate hikes are still not being priced in any time soon, and so one can assume, with earnings season about halfway through, expectations will only rise. Only one sector, energy, has failed to surprise to the upside in the aggregate (though 12 S5ENRS names have beat to 7 that missed, according to data compiled by Bloomberg). All others have surprised, with consumer discretionary names surprising the most, to the tune of 22%. The energy segment will also likely weigh today after Wednesday’s EIA crude inventories surged, putting additional pressure on the supply dynamic (WTI and Brent are both down more than 1%).

Breadth of Fresh Air

As the large caps may have gotten ahead of themselves (we’ve been talking about Apple, Alphabet and others for days now), small caps are still waiting their turn.

To some degree that is expected as the first part of earnings season is mostly dominated by some of the larger players, and given the season is unfolding slightly better than expected, it should come as no surprise. But before everyone puts their rally caps on, its worth looking at the breadth for a confirmation, as Janney analysts wrote earlier this week.

Their technical analysts have been watching for the Russell 2000 to breakout above 1600 in order to confirm the moves in the larger benchmarks. They highlight the need for continued closes above 1600 as framing the move toward 1700.

There are more than 180 members of the small cap index reporting today, nearly 10% of the membership, and so there is opportunity in the index to confirm direction. Some names of note include: YETI (just beat with shares looking higher), ERI, PLNT, PCTY, AMKR, DAN, PTCT, SSYS, LPSN, FNKO, ONDK, WW and NVCR, according to data compiled by Bloomberg.

Sectors in Focus Today

- Recent IPOs remain in focus (LYFT, ZM, PINS, SILK, SWAV) with Beyond Meat priced its IPO at the top end of its range, while Uber received a few initiations after the bell

- Apple suppliers and peers (SWKS, AVGO, CRUS, QRVO, OLED, MXIM, NXPI) with QCOM, CRUS results failing to inspire. QCOM did receive a few upgrades this morning, but is still indicated to open to below its last close. Bloomberg Intelligence wrote that QCOM was seeing “weak” high-end handset sales in China which is affect revenue and earnings

- Payments companies after Square’s 2Q forecasts missed ests. Shares fell 7% after results and are attracting defenses from Guggenheim and Keybanc here early. The latter’s analyst Josh Beck raised his estimates on the back of expected “tailwinds” from various product lines and remains a buyer of the name

- E&Ps as oil prices fall after inventory data from the EIA

- Video games makers ahead of ATVI results today (EA reports next week) as Zynga raised their outlook. Bloomberg Intelligence analyst Matthew Kanterman wrote that the company’s "strength across its portfolio is driving results above guidance and estimates for bookings and adjusted Ebitda, and these trends are sustainable as key games continue to grow"; Shares are up 15% in the pre-market and have already attracted upgrades from the likes of Baird

- Auto suppliers after Volkswagen shares jumped following growth in operating profit and “surprisingly strong” earnings, Citi wrote. U.S. traded suppliers that count more than 10% of their revenue from the Germany automaker include GNTX, SUP, LEA, BWA, ADNT, MGA

Notes From the Sell Side

Estée Lauder was downgraded to sector perform from outperform at RBC Capital Markets, a move that ends a nearly decade-long bullish stance from the firm, which called the stock “a beautiful company with a beautiful valuation.” While it remains “one of the best managed companies across our coverage,” it doesn’t expect the company can maintain its level of top-line growth over the longer term: “While EL is clearly firing on all cylinders, even the biggest bulls on the stock would have to admit these trends are not sustainable.”

The Mosaic Co. was lowered to neutral from buy at BofAML, which cited a closure on the Mississippi River. Because “barge traffic on the Mississippi River is still not able to move north of Missouri,” this likely leaves “the northern Cornbelt short of fertilizer later this spring when farmer fieldwork restarts.” Citing channel checks, analyst Steve Byrne wrote that “post-spring inventories at distributors could be long as some fertilizer applications could be skipped, leading to lower summer-fill prices. In addition, BofAML wrote that there was a risk of lower phosphate prices in 2019 and 2020, citing a recent conference call with the CEO of Saudi phosphate producer Ma’aden.

Tick-By-Tick to Today’s Actionable Events

- MLHR investor day

- DVA earnings estimated

- 7:30am -- Investment Company Institute hosts “A Conversation with SEC Chairman Jay Clayton” at its annual general membership meeting in Washington

- 7:30am -- April Challenger Job Cuts

- 8:00am -- K earnings; TEVA, BCE CN, YETI earnings call

- 8:01am -- CADE investor day

- 8:30am -- 1Q Prelim. Nonfarm Productivity, Unit labor costs

- 8:30am -- Weekly Initial Jobless Claims, Continuing Claims

- 8:30am -- CAR, UAA, YRI CN earnings calls

- 9:00am -- CF earnings call

- 9:30am -- K earnings call

- 9:45am -- Weekly Bloomberg Consumer Comfort

- 10:00am -- March Factory Orders, Durable Goods Orders, Final Cap Goods Orders

- 1:00pm -- CAT investor meeting

- 4:01pm -- GILD earnings

- 4:05pm -- CBS, EXPE, FSLR earnings

- 4:15pm -- ATVI earnings

- 4:30pm -- ATVI, FSLR, GILD, CBS, EXPE earnings calls

--With assistance from Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.