Pipeline Funds Imperiled With Even MLPGuy Seeing Their End

Pipeline Funds Imperiled With Even MLPGuy Seeing Their End

(Bloomberg) -- Even the man who calls himself “MLPGuy” is now forecasting the end of funds dedicated to the unique corporate structure known as the master limited partnership.

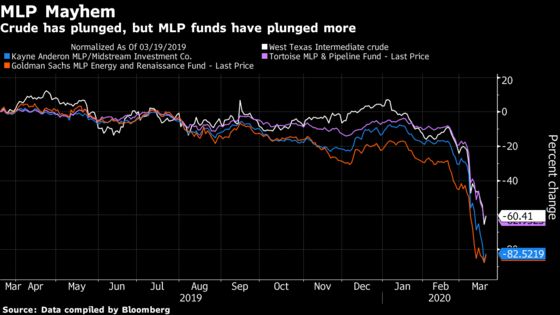

At one time, MLPs were a preferred strategy for oil and gas pipeline companies seeking to secure certain tax advantages. But those advantages were weakened by the federal government in 2018, causing many energy companies to abandon the structure. Now, the toxic combination of an oil price war and the Covid-19 pandemic is colliding with stress among the funds that hold MLPs, forcing them to join a selling spree that has caused pipeline partnerships to get hit even harder than other energy stocks.

Goldman Sachs earlier this month said it had decided to “effectively eliminate the net leverage” of two of its funds, its MLP Income Opportunities Fund and MLP and Energy Renaissance Fund. Days later, Kayne Anderson said its pipeline funds had sold securities to bolster its cash position. A representative for Goldman Sachs declined to comment, and Kayne Anderson didn’t respond to requests for comment.

“We’re seeing the death of the MLP-dedicated manager group, and that’s happening faster than anyone was expecting,” said Hinds Howard, a portfolio manager at CBRE Clarion Securities LLC who’s made a name for himself as the MLPGuy in his online blog. “We’re going to continue to see what we’re seeing now, which is daily carnage.”

As of Friday’s close, Energy Transfer LP is down 49% since March 6, the last trading day before crude prices crashed below $40 a barrel. Enterprise Products Partners LP has fallen 35%. Meanwhile, smaller MLPs, like DCP Midstream Partners LP and Plains All American Pipeline LP, are down 65% and 53%, respectively.

The number of pipeline partnerships has plummeted in the last few years after the 2014-2016 crude price collapse triggered a series of cuts to quarterly payouts long-considered sacrosanct to traditional MLP investors. In 2018, the shift away from MLPs ramped up after the U.S. changed its policy on the way partnerships are taxed. But even as companies shifted to more traditional corporate models, asset management firms continued to offer products dedicated specifically to MLPs.

Open-end funds dedicated to MLPs continued to offer $17.3 billion in assets as of last month, according to Wells Fargo Securities analysts. Comparable closed-end funds managed $12.7 billion. Those funds work like this: asset managers pool a group of investors’ money, load up the fund with pipeline stocks and borrow money against their assets in order to buy more.

It works until it doesn’t. With MLPs plunging, fund managers are forced to sell stock to comply with asset coverage requirements.

Fitch Ratings on Tuesday downgraded a number of closed-end energy funds due to “unprecedented declines” in their net asset values. The group included MLP-dedicated funds, including Kayne Anderson’s and the Center Coast Brookfield MLP & Energy Infrastructure Fund.

Compared to other sectors, “closed-end funds in the MLP sector represent a larger portion of the investor base, and they’re all forced to sell at the same time,” said Greg Fayvilevich, senior director at Fitch who specializes in asset management. “There’s very severe forced-selling versus other asset classes we’re watching.”

To be sure, not everyone agrees with MLPGuy.

”From an investor perspective, if you’re primarily interested in the midstream space for yield, you’re going to want a product that’s more exposed to MLPs,” said Stacey Morris, director of research for Alerian, which owns the best-known MLP index.

Alerian ran a “stress test” on its MLP Index last week, and assumed companies had to cut their distributions by 75%, according to Morris. “The yields on this index are still higher than REITs or utilities,” she said, using the acronym for real estate investment trusts.

One of the biggest managers in the space, Tortoise, attempted to assuage jitters in a March 11 letter to investors. The Kansas-based firm acknowledged that it’s technically possible for its closed-end funds to go to zero, but that it doesn’t think it’s likely. “It remains to be seen what will happen going forward, yet we know forced deleveraging will stop and are confident that the coronavirus will pass and that commodity prices will improve,” Tortoise said.

What Bloomberg Intelligence Says

”MLP funds are seeing a major call for redemptions, a trend that had begun well before the COVID-19 and OPEC+ developments and has only worsened since with a massive selloff in the sector. MLPs will have to cut distributions and capex and withstand what may seem to be irrational movements in the market as the group has been out of favor for over two years even prior to recent events.”

-- Bloomberg Intelligence analyst Michael Kay

Because of the relatively unpopular tax form required of MLP investors and weaker corporate governance standards, pipeline partnerships have struggled to attract institutional investors. And even retail investors, who liked MLPs for their quarterly payouts, may hesitate before dipping back into a sector that will likely experience another round of distribution cuts.

“They have to cut them in half across the board,” said Tyler Hardt, a Florida-based portfolio manager for Pelican Bay Capital Management. He sent a letter to investors that blamed his Dynamic Income Allocation Portfolio’s poor performance over the last few weeks on its MLP holdings.

“The week before, I thought MLPs were the cheapest asset class on the planet,” Hardt said, referring to the first week of March. “That all changed. I literally sold every MLP I had on Monday. It was painful, and it was 50% too late, but it is what it is.”

©2020 Bloomberg L.P.