Piggy Banks and Punishment: How the Ruble's Oil Link Came Apart

Piggy Banks and Punishment: How the Ruble's Oil Link Came Apart

(Bloomberg) -- The last time crude fell off a cliff in late 2015, it took the currency of the world’s biggest energy exporter along for the ride. As Brent lurched below $30 a barrel, Russia’s ruble plummeted to its weakest level on record.

Last month, with oil charting its steepest drop in a decade, a comparable move in the ruble was nowhere to be seen.

A multitude of factors -- from central bank measures to sanctions -- have contributed to the shift. Below is a summary of the biggest contributors and how they have eroded the link.

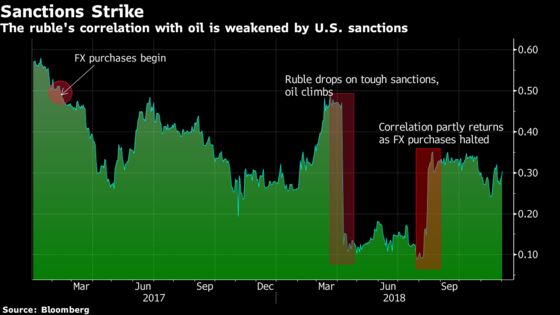

Where’s the correlation?

Back in February 2017, the central bank started sawing the ruble-crude link apart in a bid to restrain swings in the local currency. The so-called budget rule vacuumed up all additional revenue when oil was above $40 and used it to buy foreign currency for the nation’s piggy bank of international reserves.

The result? The correlation faded as the ruble traded in a range of about 55 to 61 rubles per dollar between February 2017 and April this year; volatility dropped about 20 percent as the foreign exchange purchases limited fluctuations. Meanwhile, oil swung from as low as $45 per barrel in the period to beyond $70, a difference of almost 60 percent.

What was the impact of sanctions?

The oil link weakened even more. In April, the U.S. introduced the toughest penalties yet on Russian companies as punishment for alleged elections meddling. That sent the ruble tumbling and distracted attention from a big leg up in oil prices.

Eventually, in August, with emerging-markets currencies on the decline and the threat of additional sanctions increasing, the central bank paused the hard-currency buying.

Did that re-establish the oil link?

As the chart shows, it came back, but only in part. Even though the currency conversions are on hold, the Finance Ministry still squirrels away the oil windfall, pulling rubles out of circulation from the economy and taking some of the pressure off the exchange rate.

After August, investors ignored crude blasting past $80 per barrel to the highest level in four years as the risk of new penalties mounted before U.S. midterm elections. Overall, foreigners pulled 500 billion rubles ($7.5 billion) from local bonds in the rout that started in April.

So geopolitics is the new oil?

It certainly looks that way: the currency’s correlation to foreign investments in the nation’s debt is climbing. And in November, it was the midterm results, the whiff of a sanctions delay, and jitters over Ukraine that pulled the Russian currency this way and that -- not the nosedive in crude. By the end of the month, the ruble had lost just 1.6 percent compared with Brent’s 20 percent tumble.

What could bring back the oil correlation?

If the retreat in oil prices resumes after this week’s bounce and Russia’s export blend heads for the crucial $40-per-barrel level at which the budget breaks even, then the ruble will feel crude’s pull and the link may start to return.

Equally, should the prospect of harsh sanctions on Russia’s sovereign bonds and banks dissipate next year (or if the penalties that finally emerge prove toothless), then geopolitics will loosen their hold. Normally, that would leave the currency more exposed to the oil price. But don’t forget those hard currency purchases -- they’re due to resume. Whether they’ll be big enough to mute oil’s impact is a different matter.

--With assistance from Kira Zavyalova.

To contact the reporter on this story: Áine Quinn in Moscow at aquinn38@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Alex Nicholson, Natasha Doff

©2018 Bloomberg L.P.