Picking China’s Bond Bailout Winners Can Net 30% Returns in Weeks

Picking China’s Bond Bailout Winners Can Net 30% Returns in Weeks

(Bloomberg) -- Venturing beyond bonds from state-owned issuers in China often involves more than just assessing credit risk. Investors need to make a call on whether authorities will bail out the borrower.

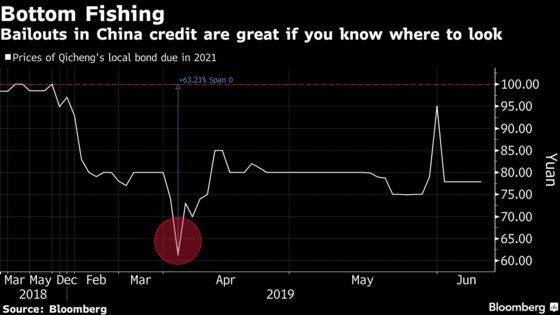

Make a good call on that, and the rewards can be great. Any trader that took the plunge a month ago on buying the debt of distressed Chinese local oil refiner Shandong Qicheng Petroleum Chemical Industry Co. got paid handsomely for the effort. They would have earned almost 30% in three weeks.

It would have been a brave move: the company warned in a public statement on June 4 that it had “lost refinancing abilities.” But less than three weeks later, another statement said it had repaid all overdue loans, and cited help from local officials and regulators in its financial obligations.

Chinese authorities have been trying to wind back implicit debt guarantees in the world’s second-biggest bond market, to introduce pricing based on credit risk -- and improve the returns on capital over time. The trouble is that any sudden, universal withdrawal could trigger a systemic collapse. That means some borrowers get rescued, though even experts struggle with predicting officials’ decisions.

“It is good comfort to bondholders that the government intervenes and reinforces the implicit government support,” said Owen Gallimore, head of credit strategy at Australia & New Zealand Banking Group in Singapore. “But it will surely lead to some moral hazard,” he said, referring to borrowers taking on extra risk in anticipation of official aid.

A counterpoint to the oil refiner -- at least until now -- is Tewoo Group Co., a state-held commodities trader whose government ownership would otherwise have argued for official support. Fitch Ratings decided in April that the public guarantee was less iron-clad than it thought, slashing Tewoo’s credit score by six steps in one go. One offshore Tewoo bond hit a record low below 40 cents on the dollar Wednesday.

In the case of the Shandong oil refiner, authorities had one strong incentive to jump in: averting a further daisy chain of defaults. The eastern province, China’s third-wealthiest, has been a kind of ground zero for private companies offering guarantees of each others’ debt as a means of encouraging creditors to extend funding. The problem is that trouble at one issuer then quickly spreads.

And Qicheng was knee-deep in that practice. Here’s the sequence of events for Qicheng’s finances:

- The company reported a 32% surge in net profit last year, and said it won a license to import crude oil and claimed a slot among the nation’s top 10 independent refiners -- underscoring in the minds of some observers a healthy underlying business.

- On June 4, Qicheng disclosed it had guaranteed a total of 3.82 billion yuan ($554 million) of other companies’ borrowing, and might need to pay out most of that tally because some of the beneficiaries were either bankrupt or had stopped operating. The contingent liabilities accounted for nearly half of net assets as of the end of 2018.

- The company also said that it had defaulted on more than 230 million yuan of debt and that several banks had withdrawn credit.

- On June 20, the company said it had repaid all overdue loans and “made progress” in resolving risks associated with the debt guarantees it had extended, citing “the assistance from city and county governments and financial regulators.”

- The government of Dongying city took the lead in sorting some of Qicheng’s debt guarantees, the company said.

- Qicheng also said bank lending had returned to "normal" and the impact of debt guarantees on its business operations had been “gradually mitigated.”

- On June 26, it made early repayment of nearly 740 million yuan on all of its three bonds, which were originally due in 2021, and the coupons accrued.

Repeated phone calls, and a fax, to Dongying city offices seeking comment on the rescue went unanswered.

“The government won’t let the cross-guarantee crisis deepen because it has a serious cascading effect,” said Jean Zou, a Guangzhou-based an analyst with commodities researcher ICIS-China. “Qicheng is one of the largest oil refiners in Dongying and is a significant contributor to local economic growth.”

Any investors with that insight on June 4 would have raked in an over 28% return on Qicheng’s most actively traded bond when it redeemed at par three weeks later.

To contact Bloomberg News staff for this story: Tongjian Dong in Shanghai at tdong28@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Sarah Chen in Beijing at schen514@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Fran Wang, Christopher Anstey

©2019 Bloomberg L.P.

With assistance from Bloomberg