Banks Are on the Hook for $760 Million of Munis in PG&E Downfall

Banks Are on the Hook for $760 Million of Munis in PG&E Downfall

(Bloomberg) -- The impending bankruptcy of PG&E Corp. is threatening to foist large liabilities on five banks that have agreed to act as buyers of last resort for more than $760 million of bonds that the teetering utility issued through California government agencies.

The company’s announcement Monday that it plans to seek protection from creditors triggered an surge of selling by owners of the floating-rate securities, causing dealers to push up the yields to draw buyers. If the selling persists and new investors can’t be lined up, the banks have committed to buy the bonds at full face value, leaving them potentially exposed to losses.

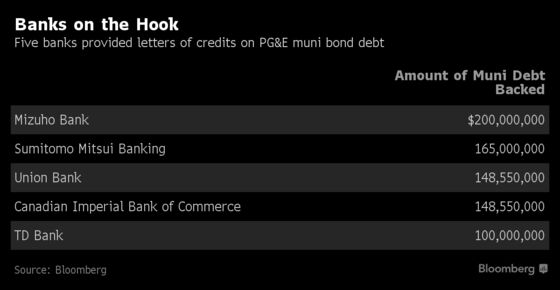

Sumitomo Mitsui Banking Corp., Mizuho Bank Ltd., Mitsubishi UFJ Financial Group Inc.’s Union Bank, the Toronto-Dominion Bank and the Canadian Imperial Bank of Commerce have provided such letters-of-credit for about $762 million of the $920 million of municipal debt issued on behalf of PG&E, according securities filings. Such guarantees are widely used for floating-rate debt and banks typically have an "unconditional" commitment to pay principal and interest if the borrower defaults, according to the market’s regulator.

Adjustable-rate PG&E backed municipal debt without a bank guarantee is trading for about 78 cents on the dollar, showing that investors are bracing for losses.

"Those letters of credit insulate muni holders," said Matt Fabian, a partner at Municipal Market Analytics. "There’s no real risk for the muni holders. It’s all about the banks."

The power company’s financial strains have brought renewed attention to the floating-rate municipal market, where governments can issue debt that doesn’t mature for decades at short-term rates because investors frequently have the option to sell the securities back at 100 cents on the dollar. That market -- where businesses can raise money for projects with a public benefit -- was roiled during the wave of selling amid the credit crisis of 2008, when the fallout helped push Jefferson County, Alabama, into a then-record bankruptcy.

There have been no disclosures showing that the banks had to buy any unwanted securities during this week’s selling, and bondholders recovered their full investment after the company’s last bankruptcy.

Spokespeople for TD Bank, MUFG, CIBC, Mizuho, and SMBC declined to comment. James Noonan, a PG&E spokesman, declined to comment specifically on the company’s municipal debt.

The banks’ guarantees have insulated the municipal market from the impact of PG&E’s distress, which was brought on by deadly California wildfires that have left it facing as much as $30 billion of liabilities. The Vanguard Group, a major owner of PG&E’s municipal bonds, said all but $2 million of its holdings are backed by banks. In a Jan. 11 report to clients this week, Barclays Plc analysts told bondholders that they face little risk of losses because of the letters-of-credit guarantees.

But the banks face more uncertainty if they wind up holding a large chunk of the debt. While bondholders remained whole after PG&E emerged from its 2001 bankruptcy, when Jefferson County went bankrupt, banks that had to purchase the variable-rate sewer bonds unloaded by investors had to take a haircut.

Union Bank’s letters of credit on PG&E-backed municipals expire in June, while the others expire in 2020. If PG&E avoids bankruptcy for now, it’s unlikely that another bank would be willing to step in after the current pacts expire, said Josh Perry, an analyst for Brown Advisory.

To contact the reporters on this story: Amanda Albright in New York at aalbright4@bloomberg.net;Martin Z. Braun in New York at mbraun6@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Michael B. Marois

©2019 Bloomberg L.P.