PDVSA Bond Traders Ensnared as Debt Ban Threatens Default

PDVSA Bond Traders Ensnared as U.S. Trade Ban Threatens Default

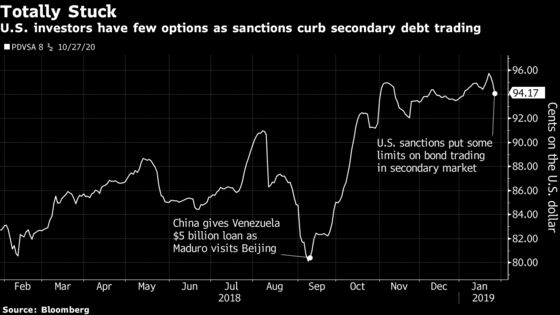

(Bloomberg) -- Trading in bonds issued by Venezuela’s state oil giant PDVSA ground to a halt Tuesday after the Trump administration included the securities in sweeping sanctions against Nicolas Maduro’s regime.

The measures forbid U.S. citizens from buying the debt on the secondary market, leaving them with two options: sell to someone abroad or hang on to the notes. Yet ambiguity from the Treasury Department is leading some investors outside the U.S. to also refrain from trading them, according to Cecely Hugh, investment counsel in emerging-market debt at Aberdeen Standard Investments in London. She said a strict interpretation could imply that firms with U.S. employees would also be restricted.

Traders at some major U.S. hedge funds said their lawyers advised them not to touch the bonds for now without further guidance from Treasury’s Office of Foreign Assets Control. Trading volume on PDVSA’s debt was down 99.9 percent on Tuesday from its five-week average, according to Trace, FINRA’s bond-price reporting system.

“There’s no way out,” said Ray Zucaro, the chief investment officer at RVX Asset Management in Miami, who holds PDVSA bonds. “Who is going to buy them? Locals are broke or out in the streets and Europeans will expect similar trading bans.”

What Bloomberg Intelligence Says"There are likely no direct comparisons that would provide a useful template for Venezuela’s debt crisis, yet some precedents -- Argentina, Iraq and Ecuador -- have matched the sheer size and complexity of a potential restructuring of the country’s debt. These mostly involved a new regime and International Monetary Fund assistance after agreements on a package of reforms."--Jaimin Patel, America’s corporate credit analyst Click here to view the research |

Meantime, the U.S. sanctions make a default on PDVSA’s 2020 notes, the one bond Venezuela has continued to service while skipping more than $9 billion in payments, all but guaranteed, according to Francisco Rodriguez, the chief economist at Torino Capital in New York.

The consequences of default are much higher on those bonds since they’re backed by a first-priority lien on a 50.1 percent stake in Citgo Holding Inc., PDVSA’s U.S. refining arm. But there’s little reason for Maduro’s government to pay after Washington handed control of Venezuelan bank accounts in the U.S. to National Assembly President Juan Guaido, whom the Trump administration recognizes as interim leader.

“PDVSA has no incentive to pay it given the loss of Citgo, nor even the capacity to do so,” Rodriguez said.

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: David Papadopoulos at papadopoulos@bloomberg.net, Rita Nazareth, Brendan Walsh

©2019 Bloomberg L.P.