Oman Has Work to Do Before a Bond Sale With Ratings All Junk

Oman Has Some Work to Do Before Yielding to Lure of Bond Sale

(Bloomberg) -- Before Oman succumbs to the temptation of selling Eurobonds, some analysts say the sultanate will first need to convince the market it’s pushing through reforms to tame its budget deficit.

That sentiment was echoed late Tuesday by Moody’s Investors Service, which downgraded the nation’s credit rating to junk. Oman now has a sub-investment grade by all three major rating companies.

“Investors continue to demand a higher risk premium on Oman due to technical and economic reasons,” said Mohammad Ahsan, managing director of rates and fixed income at Mashreq Bank in Dubai, who expects the nation to sell bonds in March or April. But “it should tap the debt markets sooner rather than later,” he said, given the pause in U.S. interest rate increases.

| Highlights of Moody’s comments and market reaction: |

|---|

|

|

|

|

|

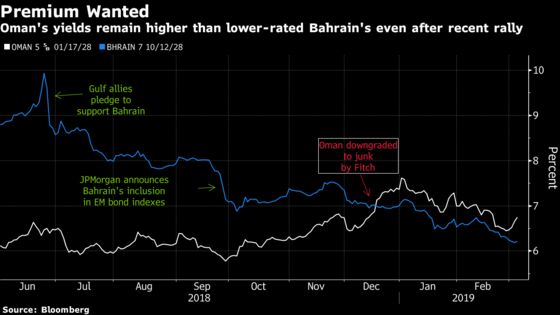

Not only have concerns over Oman’s dwindling buffers sparked a debate on whether it will need a bailout similar to the one that Bahrain got last year, analysts are also questioning if the sultanate can keep its borrowing in check. Its budget shortfall is among the largest of all the sovereigns tracked by Fitch Ratings, which downgraded its debt to below investment grade in December.

Debt sold by the government and companies in Oman had a record monthly gain in February, according to Bloomberg Barclays indexes going back to 2014. Still, yields on Oman’s bonds due 2028 remain higher than similarly rated peers and even lower-rated Bahrain’s. The gap widened as Oman’s yields rose this week.

While the Gulf Arab monarchy plans to slash its borrowing for 2019 by as much as 70 percent and rely on asset sales to plug its budget deficit, Jean-Michel Saliba, a London-based economist at Bank of America Merrill Lynch, isn’t convinced they won’t keep tapping the market if oil prices and fiscal discipline disappoint.

“Authorities would still need to increase domestic or external borrowing to cover for the projected shortfall, even with current asset sales plans,” Saliba wrote in a report.

The Bandwagon

If Oman does tap the international bond market, it would join a plethora of governments who sought to take advantage of sudden surge in risk appetite.

Qatar is returning to international capital markets with a three-part dollar bond sale after Saudi Arabia raised $7.5 billion in January. Sharjah, the third-biggest sheikhdom in the United Arab Emirates, is asking banks to help arrange the sale of Islamic dollar bonds.

Oman will probably raise $2 billion to $3 billion in bonds and loans, a senior government official said in February.

“It would make sense for them to tap the market when they are confident they have a good and credible story to tell in terms of their efforts to control deficits and when they can be relatively certain in their assessment for what will be needed to be raised this year,” said Abdul Kadir Hussain, the head of fixed-income asset management at Dubai-based Arqaam Capital. “It could all easily unravel if they come to market without a good story.”

To contact the reporter on this story: Netty Ismail in Dubai at nismail3@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Robert Brand

©2019 Bloomberg L.P.