Oil Rises as U.S. Shutdown Ends While Venezuela Tensions Mount

Futures in New York extended gains on Friday, paring most of a weekly loss. U.S.

(Bloomberg) -- Oil closed higher for the third day in a row as a deal to reopen the U.S. government eased investor fears while political turmoil in Venezuela roiled one of the world’s biggest suppliers of heavy crude.

Futures in New York rose 1.1 percent, gaining steam on reports President Donald Trump agreed to a three-week pause in the government shutdown to pursue border-security talks with Democrats. In Caracas, President Nicolas Maduro and Juan Guaido, the opposition leader, gave dueling speeches while the United Nations Security Council prepared to meet tomorrow on the crisis.

“There’s some optimism now that the government shutdown, at least temporarily, may be behind us," said Brian Kessens, who helps manage $16 billion in energy assets at Tortoise in Leawood, Kansas. “That’s got markets feeling a little bit better."

West Texas Intermediate crude for March delivery climbed 56 cents to $53.69 a barrel at the close of trading on the New York Mercantile Exchange. Brent for March settlement advanced 55 cents to $61.64 on the London-based ICE Futures Europe exchange, and traded at a $7.95 premium to WTI.

Despite those gains, both grades finished lower for the week, enduring their first weekly loss in 2019. Prices leaped about 20 percent to start the year, buoyed by output cuts by OPEC, Russia and other major producers. But the rally has faltered amid shaky economic forecasts and record production of U.S. crude.

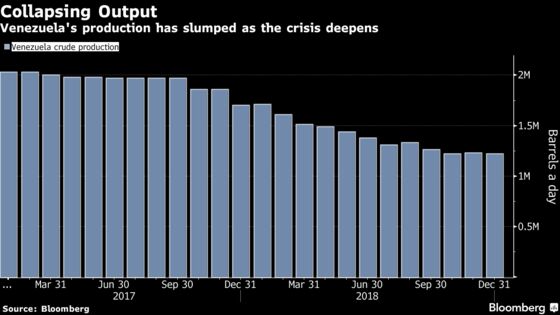

Troubles in Venezuela, owner of the world’s biggest oil reserves, provided a boost as the week wound to a close. The Latin American nation could see crude production drop by a third this year, analysts at Fitch Solutions said Friday.

“There’s an upward bias here, considering there’s supply-side outages and potential ones lurking,” Michael Tran, an RBC Capital Markets LLC commodity strategist, said by telephone. “The market could be tighter than what people previously anticipated.”

In a news conference, Guaido, who declared himself acting president this week, said he’s preparing to dismiss the head of state-run oil company Petroleos de Venezuela SA as well as the board of its Houston-based refining arm, Citgo Petroleum Corp., taking on two of the power centers that help to bankroll the Maduro government.

The OPEC member has already seen its output drop 50 percent in five years as a spiraling economic crisis takes its toll on the oil industry. Even without new U.S. sanctions, Venezuela’s production -- currently about 1.2 million barrels a day -- may lose a further 300,000 to 500,000 barrels a day, RBC estimates.

Internal conflict could result in a much bigger and longer-lasting disruption. Even if Maduro’s government is replaced, “the road back for Venezuela will be extremely arduous given the depths of the economic and humanitarian crisis,” Tran and fellow RBC analyst Helima Croft wrote in a note.

| Other oil-market news: |

|---|

|

--With assistance from Heesu Lee, Sharon Cho, Tsuyoshi Inajima, Javier Blas, Michelle Kim and Grant Smith.

To contact the reporter on this story: Alex Nussbaum in New York at anussbaum1@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Carlos Caminada, Christine Buurma

©2019 Bloomberg L.P.