Oil Suffers Worst Week in Almost 3 Years Amid Broader Malaise

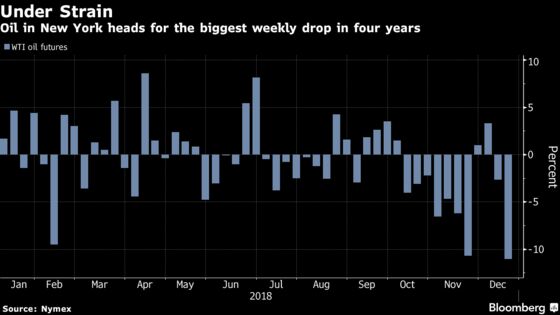

Futures in New York are on course for a 9.7 percent decline this week.

(Bloomberg) -- Oil capped its biggest weekly decline since 2016 on concerns that weakening economic growth and surging U.S. supply will lead to a surplus next year, overwhelming OPEC’s efforts to stabilize the market.

Futures sank 11 percent this week in New York, the most since January 2016. Crude joined a sell-off in wider financial markets after an interest rate increase by the Federal Reserve and the threat of a U.S. government shutdown added to economic uncertainty. Meanwhile, investors remain skeptical that cuts agreed by OPEC and its allies are sufficient to avert a looming oil glut.

"Traders are still concerned with the global slowdown and assets selling off as well," said Kyle Cooper, a Houston-based consultant at Ion Energy Group LLC. "There’s also concern about the government shutdown looming."

Crude has slumped on fears the relentless expansion in American shale will undermine efforts by OPEC and its partners to balance the market. Concerns over growth persist even as Fed Chairman Jerome Powell promised to be more cautious on raising rates next year, while a closely watched speech by Chinese President Xi Jinping offered no new reforms to stimulate the world’s second-largest economy.

West Texas Intermediate for February delivery fell 29 cents to settle $45.59 a barrel on the New York Mercantile Exchange. The U.S. benchmark is down 38 percent this quarter.

Brent for February settlement slipped 53 cents to $53.82 a barrel on London’s ICE Futures Europe exchange. Prices were down 10.7 percent for the week and have lost 35 percent since September. The global benchmark crude traded at an $8.23 premium to WTI.

Oil’s slump persisted this week on broader market turmoil spurred by a plunge in global equities after the U.S. central bank lowered the forecast for 2019 economic growth to 2.3 percent from 2.5 percent in September. The S&P 500 Index sank as much as 1.4 percent, reversing an earlier gain fueled by conciliatory comments on interest rates from a Federal Reserve official.

“It’s a bears’ world,” said Stephen Brennock, an analyst at PVM Oil Associates Ltd. “At the heart of this subdued backdrop is a bearish bias on the supply side,” while at the same time, “oil demand prospects have dimmed as storm clouds gather over the global economy.”

Meanwhile, President Donald Trump warned of a lengthy partial government shutdown if Democrats don’t back a stopgap spending measure that includes money to build a wall along the U.S.-Mexico border. The demand comes hours before a deadline to approve the must-pass legislation.

OPEC and its allies was expected to give greater clarity on their strategy to stabilize oil markets on Friday by publishing a list of production cuts agreed by each country, according to people familiar with the matter. The figures to be published are in line with expectations, showing that participating nations will curb output by about 3 percent, mostly from October levels, delegates said.

| Other oil-market news: |

|---|

|

To contact the reporters on this story: Grant Smith in London at gsmith52@bloomberg.net;Catherine Ngai in New York at cngai16@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Mike Jeffers

©2018 Bloomberg L.P.