Oil Declines as Saudi Output Restoration Calms Market Fears

Oil markets are grappling with uncertainty over how long it will take Saudi Arabia to restore output.

(Bloomberg) --

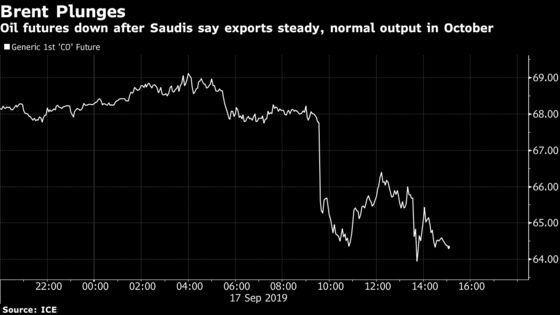

Oil sank from a 3 1/2-month high amid signs Saudi Arabia is restoring production after a debilitating weekend attack on key installations.

Futures closed 6.5% lower in London after the Saudi state oil company said it revived 41% of capacity at a key crude-processing complex just days after a devastating aerial attack that wrecked vital equipment and rocked global energy markets. The global benchmark sank to an intraday low of $63.55 a barrel.

The announcement followed conflicting media reports about the pace and probable duration of Saudi Aramco’s efforts to repair the damaged Abqaiq facility. Despite the kingdom’s reassurances at a media briefing in Jeddah, crude remained almost 7% higher than the pre-attack price, a signal of the risk premium factored in by traders.

The Saudis pledged to lift output capacity to 11 million barrels a day by the end of this month and grow to 12 million in November, Energy Minister Prince Abdulaziz bin Salman said at the briefing. Customers will be getting their supplies, and the company will tap reserves if needed to fulfill commitments, he said.

Oil futures swung wildly in London and New York for the past two days after the attack on the Abqaiq complex and an important oil field crippled Saudi production and prompted U.S. Secretary of State Mike Pompeo to allege Iran was behind the incident.

Adding to the bearish sentiment, the industry-funded American Petroleum Institute reported a 592,000-barrel increase in stocks for the week ended September 13, in contrast with analyst expectations for a 2.25 million-barrel decline. If government data Wednesday confirms the stock increase, it would break a four-week streak of inventory declines. The API also reported an 846,000-barrel drop in stocks at Cushing, Oklahoma, and a combined 3.6 million barrel build in gasoline and distillate inventories.

Brent for November delivery fell $4.87 to $64.15 a barrel on the ICE Futures Europe exchange at 5:11 p.m. in New York.

West Texas Intermediate for October delivery fell $4.09 to $58.81 on the New York Mercantile Exchange. The U.S. benchmark’s discount to Brent for the same month was $5.47 a barrel.

Meanwhile, U.S. President Donald Trump said he saw no reason to allow refiners to dip into the nation’s emergency reserves.

“I don’t think we need to. Oil has not gone up very much,” Trump told reporters Tuesday aboard Air Force One. “There’s a lot of oil in the world.“

| For more on the Saudi attacks and oil market |

|---|

|

Saudi Aramco is firing up idle offshore oil fields -- part of its cushion of spare capacity -- to replace some lost production, a person familiar with the matter said. Some customers are being asked to accept different grades of crude. The kingdom’s domestic inventories are sufficient to cover about 26 days of exports, according to consultant Rystad Energy A/S.

--With assistance from Joe Carroll.

To contact the reporters on this story: David Marino in New York at dmarino4@bloomberg.net;Sheela Tobben in New York at vtobben@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Mike Jeffers, Catherine Traywick

©2019 Bloomberg L.P.