Oil Resumes Rally as Stockpiles Seen Lower, China Eyes Tax Cuts

Oil Halts Drop Near $51 on Stockpile Optimism and Equity Rebound

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- Oil climbed as investors anticipated another decline in U.S. crude inventories and China promised to slash taxes to avert an economic slowdown.

Futures in New York rose 3.2 percent after sinking during the past two sessions. American stockpiles probably fell for the sixth time in seven weeks, according to a Bloomberg survey of analysts before government data due Wednesday. After trading closed, an industry report offered a more tepid view on demand, with big increases in U.S. gasoline and diesel inventories.

The U.S. Energy Department, meanwhile, forecast continued growth for world oil demand.

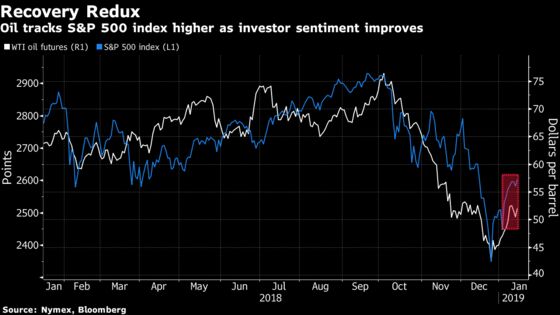

Oil resumed its New Year’s advance along with major equity indexes after China said it would cut taxes to counter any slowdown. While prices remain more than 30 percent below October’s four-year high, they’ve rallied in 2019 on signs of shrinking supplies and indications the global economy can avoid a worst-case scenario.

“The Chinese are throwing everything they can" at their economy, said John Kilduff, founding partner at hedge fund Again Capital LLC. “That’s the big key to oil markets, especially when you have OPEC and Russia starting to rein in production."

West Texas Intermediate for February delivery climbed $1.60 to $52.11 a barrel at the close of trading on the New York Mercantile Exchange. Prices dipped slightly to $51.91 after the American Petroleum Institute was said to report gasoline and distillate stockpiles grew by a combined 9.2 million barrels last week.

Brent for March settlement gained $1.65 to $60.64 on the London-based ICE Futures Europe exchange, and traded at an $8.25 premium to WTI for the same month.

U.S. crude inventories fell by 560,000 barrels last week, the API was said to report. A separate survey by Bloomberg on Tuesday forecast nationwide stockpiles probably declined by 2.5 million barrels. If confirmed by government data due on Wednesday, that will keep inventories near the lowest level since early November.

“It was very doom and gloom in December but we had no official data to back that up," said Ashley Petersen, lead oil market analyst at Stratas Advisors in New York. “Now the data that’s coming back is not really that bad. It may be pointing toward a slowdown, but it doesn’t look like a contraction, and those are two very different worlds."

| Other oil-market news: |

|---|

|

--With assistance from Heesu Lee, Grant Smith and Michelle Kim.

To contact the reporter on this story: Alex Nussbaum in New York at anussbaum1@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Joe Carroll, Christine Buurma

©2019 Bloomberg L.P.