Oil Declines as Concern of Steep Recession Counters OPEC+ Cut

Oil Edges Up as Market Mulls Potency of OPEC+ Production Cuts

(Bloomberg) -- Oil declined as projections for the steepest recession in almost a century outweighed planned output cuts from the world’s biggest producers.

Futures in New York fell as much as 5.7% amid persistent concerns of a massive supply glut. The International Monetary Fund estimated on Tuesday that global gross domestic product will shrink 3% this year, signaling that energy demand will plunge, and could be worse than anticipated if the coronavirus lingers or returns.

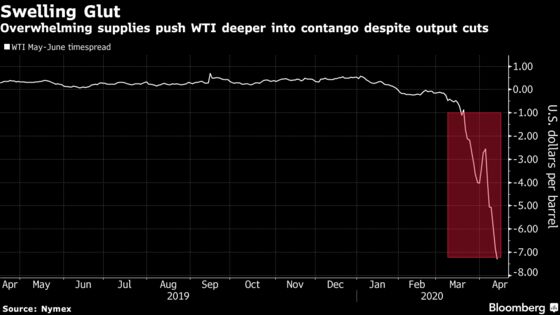

At the same time, a key timespread on the American benchmark -- a gauge of the health of the market -- is at its weakest level in more than a decade as speculation grows that the main U.S. storage hub will fill to capacity.

This weekend’s OPEC+ deal to slash production by 9.7 million barrels a day amounts to the largest coordinated cut in history, but the decision doesn’t go into effect until May and is still dwarfed by the decline in oil consumption as the coronavirus pandemic keeps multiple countries in lockdown.

“There is some general concern about oversupply and maybe the cut isn’t going to be big enough,” Phil Flynn, senior market analyst at Price Futures Group Inc., said. “The cut doesn’t do you a lot of good until the end of the month.”

The curbs will start removing almost a 10th of global output. Saudi Energy Minister Prince Abdulaziz bin Salman said Monday that the kingdom is ready to trim production even further if needed, but will only cut if others in the alliance reduce their supply accordingly. He also said the more bearish demand forecasts may be too pessimistic, so the alliance may not need to make deeper cuts.

| Prices: |

|---|

|

West Texas Intermediate crude for May fell 62 cents to $21.79 a barrel at 10:06 a.m. New York time. The front-month contract was trading almost $7 below the contract for the following month, the biggest discount since 2009. That structure -- known as contango -- expanded after stockpiles at Cushing, Oklahoma, rose by the most since at least 2004 last week.

The move has also been exacerbated by the U.S. Oil Fund ETF selling its holdings of May futures and buying June. The fund held about 37,000 futures on Tuesday, according to its website.

Texas oil regulators are scheduled Tuesday to discuss supply restrictions in response to the price crash, but KPMG International sees a low probability that cuts will be instituted. Texas pumps more oil than every OPEC member except Saudi Arabia. The U.S. was conspicuous as a hold-out on global output curbs, instead leaving it up to individual companies to steer production decisions.

| Other oil-market news |

|---|

|

©2020 Bloomberg L.P.