Oil Bulls Stick to Their Guns as Saudis Say Job Isn't Complete

Oil Bulls Stick to Their Guns Ahead of Make-or-Break OPEC Summit

(Bloomberg) -- OPEC can make or break oil’s bull run, and hedge funds are betting the cartel will keep fueling the rally.

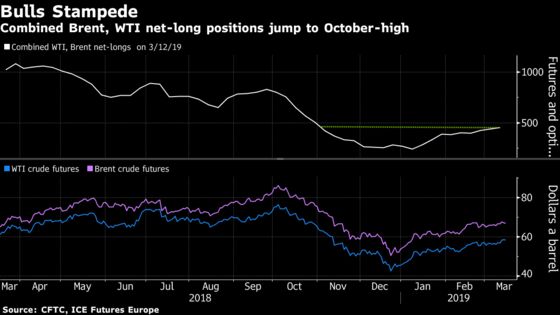

Money managers increased wagers on rising West Texas Intermediate and Brent crude prices to the highest since October ahead of a key meeting of top exporters in Azerbaijan over the weekend. OPEC and its partners need to “stay the course” until June as the group’s job is “nowhere near complete” in terms of restoring oil-market fundamentals, Saudi Energy Minister Khalid Al-Falih said late Sunday.

“As long as we come out of the weekend with stasis, the hedge funds will consider that a positive sign and will continue to support the bull run,” Ashley Petersen, an oil analyst at Stratas Advisors LLC in New York, said before the meeting.

OPEC has signaled commitment to its deal to cut output, helping spur a rally of more than 30 percent for both benchmarks since late December. Plus, sanctions on Iran and Venezuela have helped to tighten global oil supply.

WTI ended the week more than 4 percent higher, at $58.52 a barrel, just pennies below a four-month high. Brent had a weekly gain of 2 percent, to $67.16.

Saudi Arabia is said to have pledged a bigger-than-required cut in crude shipments to its customers in April, and Russia has said it was speeding up its progressive reduction of production.

“The speculative community is starting to get bullish,” Bill O’Grady, chief market strategist at Confluence Investment Management in St. Louis, Missouri, said before the meeting. “The Saudis appear pretty committed to trying to keep supplies constrained and generally, if the Saudis are willing to put that out there, the rest of the cartel usually goes along.”

But there was less full-throated support for extending the OPEC+ output-cuts agreement from Russia and Iraq -- the pact’s other two biggest producers. Russian Energy Minister Alexander Novak said Sunday that uncertainties arising from production in Venezuela and Iran make it difficult for the coalition to determine its next step before May or June.

Hedge funds’ WTI net-long position -- the difference between bets on higher prices and wagers on a drop -- climbed 4 percent to 157,648 futures and options in the week ended March 12, according to the U.S. Commodity Futures Trading Commission. Longs rose for a third straight week, while shorts dropped 7 percent during the period.

At the beginning of the year, there were fears that U.S. production growth “was going to explode, demand is going to crumble, and what are we going to do with an excess of oil?,” Petersen said. “Now, we’re actually getting data that shows the sky isn’t falling and positions are reacting accordingly.”

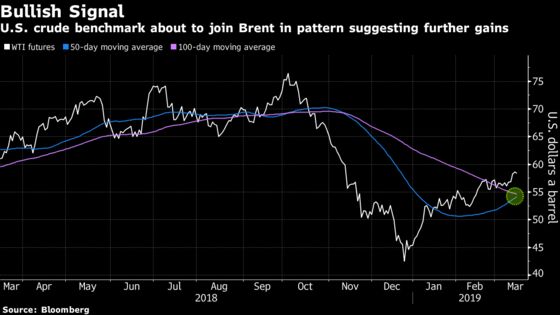

Another reason for hedge funds to become more optimistic on crude: technicals. WTI’s 50-day moving average is poised to cross above its 100-day moving average-- a bullish signal that often invites buyers into the market. Brent’s 50-day average crossed above its 100-day line on Friday.

Not everyone was optimistic, though. Investors have rushed to short one of the top oil exchange-traded funds as crude prices hover near four-month highs. Short interest in the $1.86 billion SPDR S&P Oil & Gas Exploration & Production ETF made up close to 35 percent of the fund’s outstanding shares, the most since 2014, according to Markit data.

| OTHER POSITIONS: |

|

To contact the reporters on this story: Jessica Summers in New York at jsummers24@bloomberg.net;Ben Foldy in New York at bfoldy@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Carlos Caminada, Catherine Traywick

©2019 Bloomberg L.P.