(Bloomberg Opinion) -- Investors have their first snapshot of what Ocado Group Plc’s trading looks like in exceptionally favorable trading conditions for its online supermarket business.

Its core customer-facing retail business, now a joint venture with Marks & Spencer Group Plc, lifted sales by 27% in the six months to May 31. The frantic buying of groceries driven by the pandemic began about halfway through the period, and so isn’t fully reflected in the numbers. Sales were running about 40% up going into the second half of the financial year.

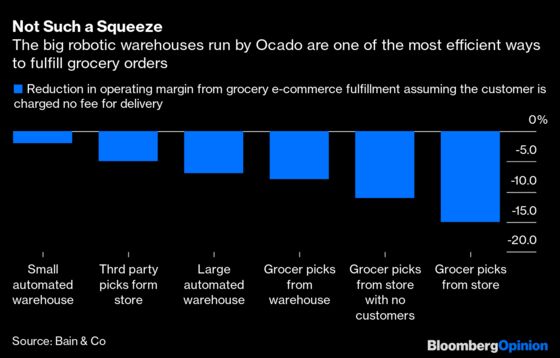

Ocado has always argued that its model, which generates economies of scale as orders are fulfilled in its huge robotic warehouses, is more profitable than supermarket employees plucking flour and toilet paper from shelves. The evidence supports that, with Ebitda (a measure of profit) in retail almost doubling to 46 million pounds ($58 million). But Ocado’s shortage of capacity prevented it from fully capturing demand, which was worth five times more in terms of revenue at the peak of the crisis.

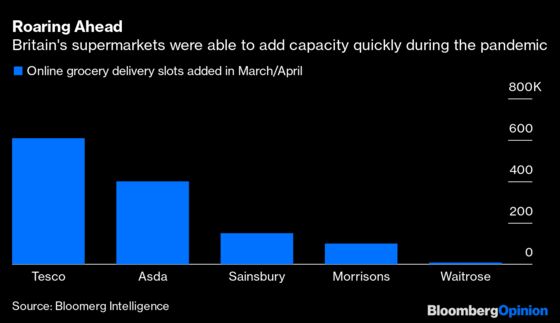

Much of that opportunity was taken by traditional retailers that were able to quickly increase their ability to fulfill online grocery orders from their vast store networks by adding more delivery vans.

The challenge for Ocado is to ensure it gets its share of the growing online grocery market rather than let it slip to the incumbent supermarkets. It’s building a smaller warehouse in southwest England, which takes half as long to construct as its traditional facilities. On Tuesday it said The Kroger Co., whose online operations it helps run, would build a mini-warehouse too.

These and other moves will add about 40% more capacity in the U.K. from next year. But they won’t be enough on their own. Where Ocado provides delivery services for other retailers, it should work with them to provide click-and-collect services from the stores. It should also find a way to enable its own customers to order online but collect from a designated location — in the U.K., M&S’s big store base provides such an opportunity.

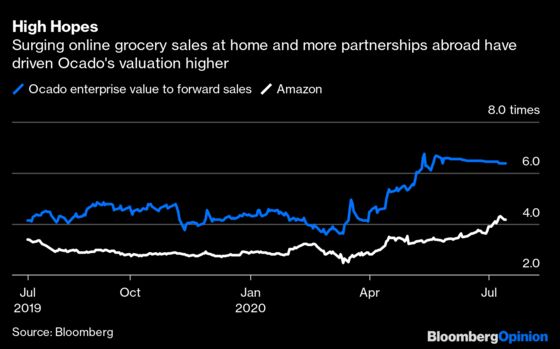

Shares in Ocado have risen nearly 60% since the start of this year, to about 20 pounds, valuing the company at 15 billion pounds. At a group level, it still makes a net loss as it continues to invest in growth.

Ocado has always divided investors. To some it is the best thing since a loaf of sliced bread arrived in a delivery van. To skeptics it is a money pit, devouring capital and never managing to make an adequate return.

For now, this is probably as good as it gets for Ocado. To justify investors’ faith in supporting a recent 1 billion pounds fundraising, the group must prove it can satisfy demand in its home market. And it must do so without suffering any slippage in its international roll-out. Investors’ expectations are riding on a lot going right.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.