Obamacare Markets Stabilize as Premiums Remain High for Many

Obamacare Markets Stabilize as Premiums Remain High for Many

(Bloomberg) -- When insurance customers log onto the Affordable Care Act’s sign-up websites Thursday, they’ll find that health-care coverage prices are high but largely stable, after months of tinkering by the Trump administration.

While many of Obamacare’s core elements remain intact, other pieces have been weakened or removed. President Donald Trump pledged to “let ObamaCare implode,” and cut some of the law’s subsidies. Congress neutered a mandate to buy coverage, and the administration has promoted cheaper plans with fewer benefits.

The sign-up season for coverage next year comes five days before a mid-term election seen as a referendum on Trump and his agenda. Polls have showed that voters consider health care a top issue, and the administration has been eager to take credit for the stabilizing insurance premiums in the Affordable Care Act. On average, the premium for typical plans in the 39 states that use the federal healthcare.gov website will drop 1.5 percent in Trump’s third year in office, the administration said.

Trump “took decisive action to stabilize insurance markets and expand choices for American consumers,” Health and Human Services Secretary Alex Azar said in a September speech. For next year, a benchmark “silver” plan -- which provides a mid-level of coverage -- will cost $406 a month for a 27-year-old, before any subsidies, according to data from the U.S. Centers for Medicare and Medicaid services. Prices vary by region, age, and coverage level.

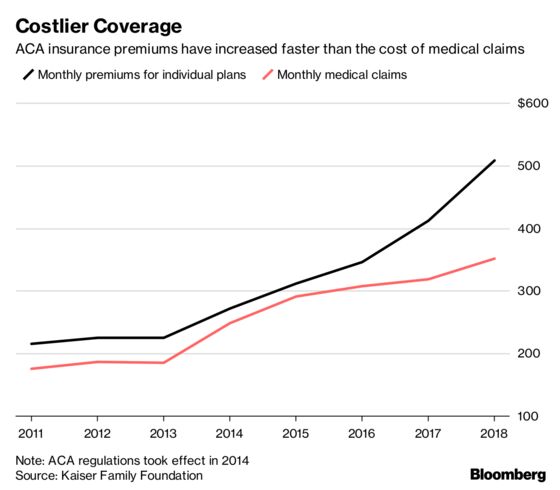

Premiums might have been lower still without some of the administration’s actions, according to one study. The price for ACA health plans is 16 percent higher than if the administration and Congress hadn’t cut subsidies to insurers, repealed a mandate that all Americans have coverage or pay a fine, and promoted cheaper forms of coverage, according to an analysis from the Kaiser Family Foundation, a health research group.

Some of the downward pressure on rates this year comes after particularly sharp increases in past years, according to Cynthia Cox, director of health reform and private insurance at Kaiser.

In Tennessee, Cox said, premiums for ACA plans exceeded medical costs by some of the highest margins in the country in 2017, then went up in 2018 anyway. For 2019, they’ll fall by 26 percent, according to CMS data. Rate changes in other states including Missouri, Pennsylvania, and New Hampshire followed a similar pattern.

Past premium increases have made the markets more attractive for some insurers.

“It’s incredible what a 60 percent rate increase actually does to your earnings,” Molina Healthcare Inc. Chief Executive Officer Joseph Zubretsky said at the company’s investor day May 31, according to a transcript. The company is expanding its ACA offerings in Utah and Wisconsin next year, states it had previously exited.

Compared to this year, 23 additional health insurers will offer coverage during open enrollment, according to CMS. Companies including Cigna Corp. and Anthem Inc. are selling in areas they had left, the agency said. Only five states on the federal exchange will have just one insurer, compared with 10 in 2018, according to the agency.

“Average rates are still too high,” Seema Verma, the agency’s administrator, said on Oct. 11. “If we are going to truly offer affordable, high quality health care, ultimately the law needs to change.”

A spokesman from Verma’s agency declined to offer a projection on how many people will sign up for coverage through the exchanges for next year.

Still Expensive

The plans are expensive for people who don’t get help. About 15 million Americans bought coverage in the individual market last year, and 8 million of them got federal subsidies to help them afford it, according to Kaiser Family Foundation data. More Americans are also in plans with high deductibles -- forcing them to pay more out of pocket when they use care.

Paul Tellez, a 48-year-old attorney at a small firm in El Paso, Texas, said he pays almost $1,000 a month to insure himself, his wife, and their young daughter on the ACA market. That’s after subsidies lowered the cost by about $200. Premiums for his current plan went up so much last year, he said, he considered dropping coverage.

“I’m just trying prepare myself for the sticker shock,” Tellez said.

When he looked on healthcare.gov last week, the site said Tellez’s estimated income of $85,000 next year disqualified him from getting a tax credit. His monthly health insurance bill already approaches his $1,300 mortgage payment.

Tellez takes medication for diabetes and high blood pressure. In May, he went to the emergency room for what he called a “raging bloody nose” that doctors cauterized. The incident cost him about $5,000 because he hadn’t met his plan’s deductible.

He’s skeptical of the short-term health plans that the Trump administration is promoting as less expensive alternatives. Tellez had a short-term policy between jobs about six years ago. “Reading the fine print, it didn’t cover much of anything,” he said. “They’re just a bunch of flim-flam.”

New Plans

Another Trump administration rule will let groups offer what are known as association health plans. The Nebraska Farm Bureau is offering such a plan with insurer Medica. It would let small farmers, ranchers, and other agricultural businesses to band together to buy health plans similar to what large employers offer.

Other policies from the Trump administration could boost those short-term and association plans. One proposal would give states more leeway over the type of coverage that can be sold, and would let states steer ACA subsidies toward short-term policies and association health plans, including some that don’t cover pre-existing conditions.

The proposal won’t likely take effect until 2020.

To contact the reporters on this story: John Tozzi in New York at jtozzi2@bloomberg.net;Blake Dodge in New York at bdodge4@bloomberg.net

To contact the editors responsible for this story: Drew Armstrong at darmstrong17@bloomberg.net, Timothy Annett

©2018 Bloomberg L.P.