Noxious Trade Talk Fumes Dull S&P Bears’ Senses: Taking Stock

Noxious Trade Talk Fumes Dull S&P Bears’ Senses: Taking Stock

(Bloomberg) -- We’re on our third straight day riding the fumes of optimism over the same concept -- loosening the timeline on the imposition of higher tariffs upon the Chinese in the trade war. We had the slightest hints, then a continuation without a rebuttal, and now the latest Bloomberg reports peg a possible delay at 60 days (still just according to people familiar with no explicit confirmation) assuming the talks go right.

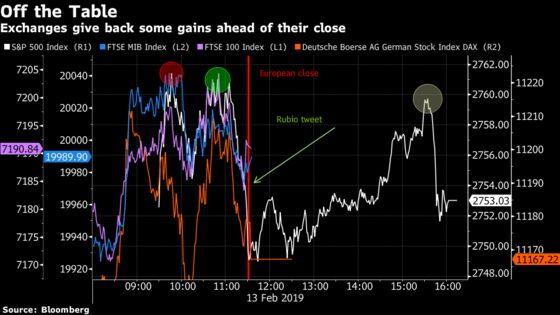

That last point is important to note given the action we saw in U.S. and European bourses Wednesday heading in their respective closes. Though Senator Marco Rubio’s tweet suggesting he was proposing legislation to bring taxation rates for buybacks inline with dividends definitely sapped some energy from the S&P around 11:30am, the weakness initially appeared as we reached some of the top of the day’s ranges and as European exchanges neared a close.

And think, would YOU want to be long heading into the trade talks that began today between Chinese Vice Premier Liu He, U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin? We know the sides are far apart on enforcement and other key issues, but the risk/reward needs to be there. S&P valuations are approaching their November highs, and you have to ask yourself -- if a deal is made tomorrow, where should it be?

MKM strategists led by Michael Darda in a note Wednesday wrote that a 20% gain in the S&P for 2019 (citing history that suggests its possible after a Fed pause that "isn’t too late to avoid a recession") or more wouldn’t be out of the question. Their official target is 3060, which implies 5% upside from the highs seen in 2018, with the rationale being a continued rebound in the forward equity multiple (2018 peaked near 20x, according to Darda).

Chips and Dips

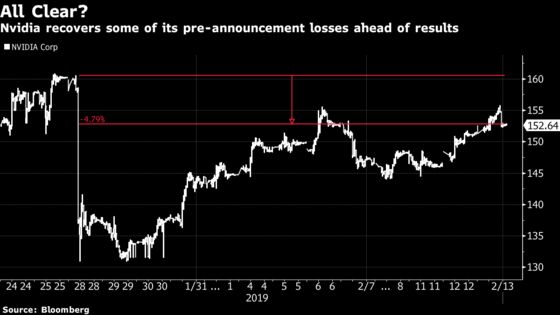

I wouldn’t normally spend any time previewing a company that has, for all intents and purposes, already provided their results, but in light of the Apple circumstance that changed their narrative after pre-announcing, and the fact that the subject of this section, Nvidia, has twice revised down the quarter in question, it seems warranted. Citigroup analysts also discussed the state of semiconductors recently, noting Nvidia was among the “most popular long/most asked about" stocks in their discussions with investors.

The gaming chipmaker has proved some of the knee-jerk naysayers wrong (analysts in the wake of the pre-announcement in late January were calling for shares to drop to anywhere from $130 down to $100), with a bounce that RBC describes as having occurred given that the "decks" are cleared near term after their disclosures. I went into detail about how NVDA massively whiffed on Q4 forecasts back in November and again two weeks ago and we’ll see if the third time is the charm. Deutsche Bank analysts see the April quarter risks as "skewed to the downside," with headwinds likely due to datacenter “lumpiness” as described by Intel and others. Morgan Stanley notes that “prospects for a 2h recovery in memory spending are fading quickly.”

Cisco will likely provide a lift to the entire tech segment today, ahead of Nvidia’s results, and another crucial one to watch post-market will be Applied Materials. Shares of the semiconductor manufacturer rose when its peer Lam Research reported in late January, and outperform-rated RBC recently wrote that its "unlikely" demand worsens from this point. The analysts also note that "operating margins could surprise to the upside despite lowered expectations from a revenue perspective."

Lucky Number 13

Also on offer for post-market activity are the closely watched quarterly filings on investment manager holdings for the fourth quarter of 2018, known as 13F-HRs. It only captures a snapshot of holdings as of December 31 (~45 days ago mind you), but that rarely stops traders from loading up on some key themes and one-off holdings (think: did Buffett pare down any major holding? What else did he or Appaloosa’s Tepper load up on for the quarter?).

The quarter will offer a plethora of narratives given the massive equity market sell-off that began in October. Which funds got lucky and avoided the brunt by piling into defensive names that outperformed? Who bottom fished for depressed names? Who is bound to be outperforming in 2019 after piling into industrials, energy and real estate (the top 3 performing sectors this year).

And in specific names, who built (or dumped) stakes right ahead of the Apple warning? Did Third Point, Jana, Appaloosa, Coatue and Druckenmiller’s family office reverse their bearish tilt on Facebook from the third quarter? After dumping stakes in EA ahead of its video game launches (and potentially rotating into peers ATVI, TTWO), did any funds pile back in and hold stakes through the Christmas selling season? The last point becomes even more interesting in light of the Activision/EA saga discussed in Tuesday’s Taking Stock. Lastly, there’s the M&A wrinkle, especially in light of the mega mergers in Celgene/BMY and BB&T/Suntrust. You can find stories in real time via TOPLive and NI Hedge.

Sectors in Focus Today

- Senior living facilities after BKD’s forecast missed and HCP’s views missed

- CSCO earnings beat, with ERIC and NOK in Europe outperforming, watch AKAM, JNPR

- Beauty names as Avon Products gave up some of its large pre-market gains on results; shares were also on a tear after Bill Miller’s positive comments in late January; shares remain up 53% since his CNBC interview

- Beverage names (like MNST) as KO results disappoint

- Consumer goods names after GOOS, YETI surprise to the upside

- Semi-cap equipment ahead of AMAT results (see LRCX, MKSI PLAB)

- Accessory stocks after FOSL’s disastrous results post-market, which continued the theme after Tapestry issues

- Mattress names and suppliers like PRPL, LEG after SNBR results beat and TPX results missed

- Hotels in focus after HLT’s results Wednesday pre-market and Hyatt post market both beat

- Gold miners after Kinross and Goldcorp both report; KGC beat, while GG took an impairment related to the Newmont deal

Notes from the Sell Side

Macquarie is out with a double upgrade of integrated oil giant Exxon Mobil, citing its scale in the Permian, its larger Guyana opportunities and its expansion in LNG. Analysts expect the final investment decision for Mozambique in 2019 and an expansion phase in Qatar in which XOM will have a large presence. The $83 price target assumes nearly 9% upside from the last close.

Synchrony Financial is indicated higher after Goldman Sachs analysts become bulls, expecting 23% upside to the now buy-rated (from neutral) shares. Analyst Ryan Nash expects shares to outperform as contract renewal overhangs on 4 of its 5 largest partners have been removed, credit normalization has subsided, the company has a "robust" capital return program, and the valuation sits at a discount to peers.

Tick-by-Tick Guide to Today’s Actionable Events

- Today: Confirmation hearing for prospective FHFA head Mark Calabria (+FMCC, FNMA earnings)

- HUM, IT investor day

- 7:00am -- Charlie Munger on CNBC

- 8:00am -- EMR investor meeting, AIG, YETI earnings call

- 8:30am -- Jan PPI, Initial jobless claims, continuing claims

- 8:30am -- Dec Retail sales

- 8:30am -- KO, ZTS earnings call

- 9:00am -- MRO earnings call

- 10:00am -- Nov Business inventories

- 10:00am -- DUK earnings call

- 10:30am -- EIA Natural gas inventories

- 11:00am -- BMY at Guggenheim Healthcare Talks Idea Forum

- 11:30pm -- MNOV analyst meeting11:50am -- JNPR at Goldman Sachs Tech and

- Internet conference

- 12:00pm -- Brexit motion vote in U.K. Parliament (another vote scheduled for Feb. 27 as well)

- 1:50pm -- CSCO at Goldman Sachs Tech and Internet conference

- 2:00pm -- SGEN at Guggenheim Healthcare Talks Idea Forum

- 4:01pm -- AMAT earnings

- 4:05pm -- CBS earnings

- 4:20pm -- NVDA earnings

- 4:30pm -- AMAT, CBS earnings call

- 5:30pm -- NVDA earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.