Now Repo Distortions Emerge in Europe’s $9 Trillion Market

The $9 trillion market is becoming increasingly fragmented, according to the Bank for International Settlements.

(Bloomberg) --

The European repo market may have escaped the kind of turmoil that engulfed the U.S. financial system this year, but that doesn’t mean all is calm.

The 8 trillion-euro ($9 trillion) market is becoming increasingly fragmented, according to the Bank for International Settlements. While this hasn’t caused harm yet, it raises the risk that cash may not flow through the system properly, BIS said in its quarterly review. That’s what caused chaos in the U.S. almost three months ago.

Trading repos -- repurchase agreements where bonds are used as collateral for short-term loans -- acts as the essential plumbing for the wider fixed-income market. The Federal Reserve was forced to take action to calm the U.S. repo market after rates spiked in mid-September. Some fear a similar event later this month, when year-end liquidity needs renew the pressure.

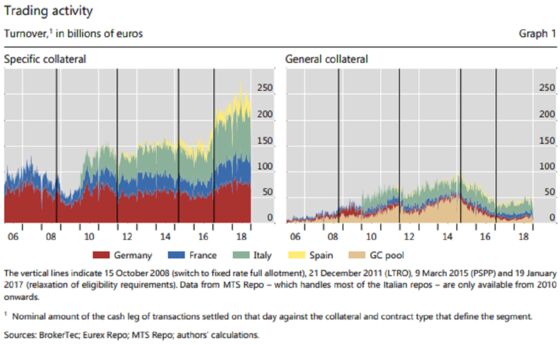

The BIS study found the European repo market has in recent years been driven by investors seeking specific collateral rather than funding. That exacerbates a segmentation along collateral lines, where liquidity, price and behavior of securities all vary by geography and some traders specialize in bonds issued by their own government.

The whole trend has gained strength thanks to central bank stimulus, which simultaneously increased funding liquidity but removed collateral, the BIS said.

“This may impede the redistribution of liquidity,” authors Patrick Schaffner, Angelo Ranaldo and Kostas Tsatsaronis wrote in the report.

Repo Breakdown

There are roughly two segments in the repo market -- general collateral repo and specific collateral repos. The former is primarily for borrowing and lending of cash, while the latter is driven by collateral needs and transactions specifying particular securities.

Within both segments, liquidity in Europe varied according to the home country of the collateral, the BIS said. The most-traded specific repo was German. Spanish and Italian collateral segments demonstrated lower and more volatile liquidity on average.

Market participants tend to specialize in one or just a few segments, the BIS found, contributing to the fragmentation.

The risk is that it all “may hinder arbitrage activity across collateral segments,” according to the report.

For now, the ECB’s short-term euro rate, the wholesale euro unsecured overnight borrowing cost for the region’s banks, is betraying few signs there might be trouble brewing beneath the surface.

“It remains unclear whether the importance of collateral demand in reshaping the repo market’s dynamics is a permanent shift or only a consequence of the central bank’s balance sheet expansion,” the BIS said. “In either case, these efforts have amplified the trend towards market segmentation.”

--With assistance from Richard Jones.

To contact the reporter on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Cecile Gutscher

©2019 Bloomberg L.P.