Nomura Says ‘50 Cent’ Has Banks Scrambling for VIX Hedges

Nomura Says ‘50 Cent’ Has Wall Street Scrambling for VIX Hedges

(Bloomberg) -- The re-emergence of a huge U.S. equity volatility buyer has banks scrambling to hedge the other side of the trades and is even affecting levels on the Cboe Volatility Index, according to Nomura Securities International.

In July, a big purchaser accumulated protection against a major sell-off in U.S. stocks over the next month on the so-called VIX, in activity similar to that of the volatility buyer known as “50 Cent” given a penchant for hedging at that level in large amounts. And there’s someone on the other side of all those purchases.

Dealers are short a series of VIX calls, especially those with strike prices in the 20 to 24 range, “in massive size due to the ‘50 Cent’ entity’s massive hedging program flows,” Nomura strategist Charlie McElligott wrote via email on Wednesday. “This fund’s return to the VIX options market has the Street beyond capacity because as dealers get short this VIX upside, they have to go out and buy all sorts of crash protection due to their synthetic position.”

JPMorgan Chase & Co. sees 20 as particularly key for VIX.

“We are seeing relatively elevated gamma imbalance tilted toward the calls, with large concentration around the 20 strikes,“ said Peng Cheng, a JPMorgan global quantitative and derivatives strategist. “Since dealers are likely to be short gamma, one would expect ‘reverse pinning,’ i.e. VIX futures to be repelled away from the 20 strike. Therefore the 20 level is likely to be a floor/support for the VIX August future.”

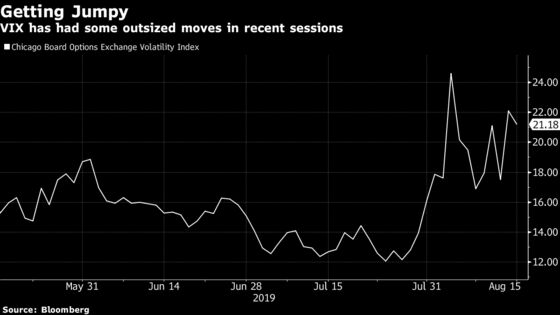

The VIX closed down 4.2% at 21.18 on Thursday, while VIX volatility (VVIX) fell 1.5% but remained near its highest levels since October 2018. Six of the VIX’s last nine sessions have seen double-digit percentage moves as markets are whipsawed by U.S.-China trade developments and geopolitical tensions. Skew, the cost of bearish options compared with bullish ones, has gotten expensive and forced investors to look hard for cheap protection. And the MOVE Index, which measures prices swings in Treasuries, is the highest since February 2016.

“VIX, volatility of volatility (VVIX) and skew have been saying over course of July that we were either going to crash up or crash down,” McElligott wrote. “So clearly all this short gamma for dealers in the VIX complex means chase-y moves in either direction, especially with the rates volatility spasm.”

--With assistance from Luke Kawa.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Dave Liedtka, Rita Nazareth

©2019 Bloomberg L.P.