Nine Years of Falling Short on Inflation: BOJ Decision Day Guide

Nine Years of Falling Short on Inflation: BOJ Decision Day Guide

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

Governor Haruhiko Kuroda will face a grilling Thursday when the central bank releases a new forecast expected to show Japan will fall short of its inflation target after nine years of unprecedented stimulus.

The Bank of Japan’s initial price projection for the year starting in April 2021 and its growth forecasts will be the main focuses of the meeting, though neither is expected to budge the needle on policy. All but three of 48 economists surveyed by Bloomberg expect the central bank to maintain its yield curve control program and asset purchases at the meeting.

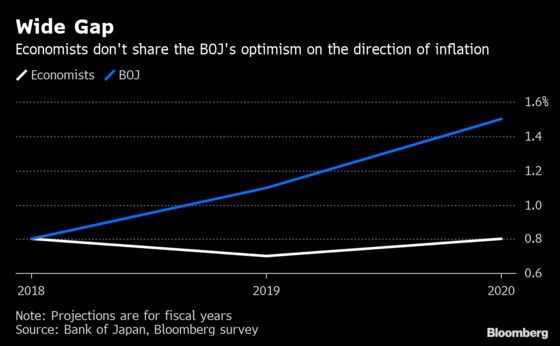

Economists predict the fiscal 2021 price forecast will be its lowest new projection looking two years into the future since Kuroda took the helm of the BOJ in 2013, promising 2 percent inflation in about two years. It would also mean that Kuroda is at risk of failing to hit the target before his second term ends in 2023.

While the forecast will further demonstrate the central bank’s failure to achieve its inflation goal, the governor is expected to stick to his line that momentum in prices has been maintained given that the forecasts still show an upward trajectory.

Weaker Growth

The central bank is also likely to consider trimming some of its growth projections to reflect weaker output and export data, according to people familiar with the matter. That would fit in with the dimmer assessment of the economy the central bank gave at its last meeting.

Again Kuroda is likely to reiterate his view that the economy will pick up in the second half of the year. Investors will closely monitor whether the governor’s confidence in that view has strengthened following signs of a stabilization in economic growth in China, Japan’s biggest trading partner.

Should the governor express more pessimism over Japan’s economic strength, that could fuel a growing view that the BOJ’s next policy move will be further easing should the economy and prices buckle after a sales tax hike later in the year.

The policy statement and the quarterly outlook report are typically released around midday followed by a press conference by Kuroda at 3:30 p.m.

What Bloomberg’s Economist Says

“The Bank of Japan heads into a policy board meeting this week with downside risks to the economy alive and well... We expect it to remain on hold, but there is sure to be lively discussion about the pros and cons of its stimulus -- with inflation still weak while further signs of strain emerge.”

Yuki Masujima, economist

Click here to read more

What to look for

- The BOJ currently sees inflation including the sales tax effect averaging 1.1 percent in fiscal 2019 and 1.5 percent in fiscal 2020. Its forecast for the following year is likely to be higher than both of those but below 1.8 percent, the current lowest forecast two years into the future.

- Kuroda’s views on the property market will take on extra significance following the BOJ’s semi-annual financial system report last week warning on the high level of real estate loans. With the prospect of no achievement of the inflation target, Kuroda will be asked about how to manage accumulating side effects.

- Oil prices, a huge swing factor for Japan’s inflation, soared after the U.S. announced its scrapping of waivers for countries buying Iranian crude despite sanctions. A rise of oil is positive for BOJ’s price efforts but could cool household sentiment before a sales tax hike in October.

- If asked about the sales tax in light of comments by an ally of Prime Minister Shinzo Abe on the chance for another delay, Kuroda is likely to reiterate his support for restoring fiscal health, hinting at the need to go ahead with the increase.

Policy Recap

- Pledge to keep interest rates extremely low for an extended period of time.

- A rate of -0.1 percent on some reserves financial institutions keep at the central bank.

- Yield target of about zero percent for 10-year Japanese government bonds, with a trading range of about 0.2 percentage point on either side of the mark.

- A target of increasing JGB holdings by about 80 trillion yen ($715 billion) a year is now secondary to controlling interest rates. The actual pace of purchases has fallen to well below half that rate.

- A guideline to increase holdings of exchange-traded funds by 6 trillion yen a year. Actual purchases vary widely from month to month, depending on market conditions.

To contact the reporter on this story: Toru Fujioka in Tokyo at tfujioka1@bloomberg.net

To contact the editors responsible for this story: Brett Miller at bmiller30@bloomberg.net, Paul Jackson, Henry Hoenig

©2019 Bloomberg L.P.