New Highs? Check. FAANG Highs? Nope. Now What?: Taking Stock

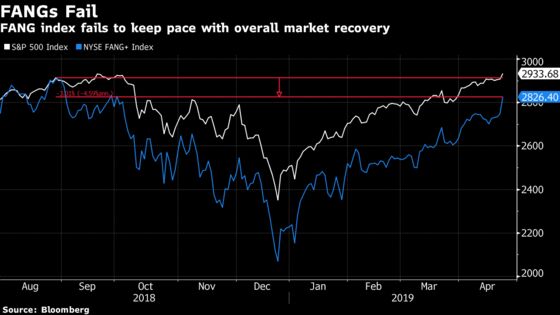

FAANGs have yet to recover their highs from before the selloff.

(Bloomberg) -- I won’t talk about the all-time highs set in the S&P 500 yesterday.

But the bottom line is that earnings illuminated screens with green from the get-go Tuesday, and once we hit the intraday-high, the appetite held, staying in a 2-point range around 2,933 for what felt like hours in the afternoon. And guess who led? The market’s old friends in the FAANGs (FAAMG), as if they had been waiting for a signal from other few earnings reports to participate in the rally they’ve largely failed to lead.

Sure, it helped that health care appeared to finally get cheap enough for dip buyers, partially assisted by more voices from the Street. UBS chose to take on new coverage in the managed care segment and Bernstein defended the space, writing they "see potential value in knocked-down" stocks. But by and large, a motley crew was responsible for taking the bull market by the horns.

Whoa Nelly

How’d we get here? On the face of it, tech and discretionary names led the S&P from the brink in December, rising 37% and 32%, respectively from the market’s December lows. It would be easy to assume that the usual suspects were responsible for both sectors’ rise (heavy weights Apple and Microsoft in tech, Amazon in consumer discretionary). But no, those names failed to keep pace with the top gainers in their respective sectors, instead, leaving the leadership to others. In discretionary, it was Chipotle (which reports post market) and in tech, it was Xerox (reports Thursday). The communications services index broadly, which houses the rest of the FAANG members? Not even in the top three sectors of the S&P over the period.

As you see above, FAANGs have yet to recover their highs from before the selloff. As a colleague wrote yesterday, this and other tech factors may in fact set up bullishly from a technical perspective. Key players in that calculus report results today, including Facebook, Microsoft and Tesla.

And with lowered expectations abound, even the worst performers have an opportunity to contribute. Retailers like Nordstrom, Macy’s were overshadowed in the recovery, actually posting negative returns in one of the best quarters in years. Cowen wrote earlier this week that they see many parts of retail as an area to beat those lowered expectations despite the deceleration in digital and physical traffic.

For Whom the Bell Tolls

Wednesday’s session will be about bellwethers, though the share reactions will need to be closely monitored in light of our newfound heights in the S&P. Reports that

trade negotiators led by U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin will travel to Beijing did little to boost futures here early, as it appears some investors are taking some money off the table.

Texas Instruments, a semiconductor bellwether, will be battling "good news" expectations that sent the SOXX to records earlier this year, and after momentarily running up more than 5% after the close with results, gravity appears to have taken hold in a very average forecast (ADI also erased some of its momentary gains in sympathy). Stifel analysts had recommended investors play secular themes (like 5G and PC demand) in individual names given the optimism that took hold. TXN management’s commentary on slower annual demand was the main disappointment for investors, Loop Capital analyst Cody Acre wrote, while Goldman Sachs highlighted that TXN’s valuation was “stretched,” even with an expected recovery in 2020.

Caterpillar is due any minute and the last few quarters were tough on the construction and mining company, as shares fell after each of the last four reports. Astec Industries, a much smaller player in that sandbox lost a quarter of its market valuation when it reported results yesterday.

Socially Awkward

It should come as no surprise that the social media stocks are volatile. Snap Inc. and Twitter though put on a show over the past 24 hours. Twitter’s near 18% intraday gain (its best in nearly 2 years) on the back of strong user growth and Snap’s 14% jump post-market yesterday before turning negative (and it’s now positive) is not for the faint-hearted. JPMorgan has already upgraded the picture-sharing platform, while Cowen called results “better than forecast” in DAUs, Ebitda and revenue. Morgan Stanley highlighted better monetization and its success in direct response advertising.

Pinterest should see added volatility today (already up more than 2%) on the back of the two communication mediums’ results, and as mentioned above, the mother of all social media platforms, Facebook, is due post-market today.

Electric Avenue

Included in the FAANG index mentioned above is, curiously, Tesla Inc. And they are due to report just 48 hours after their investor day. Here’s my colleague Esha Dey on what to expect after the close:

Brace for an ugly show from Tesla Inc., whose shares have vastly underperformed the S&P 500 Index so far this year. Expectations for the first quarter have been lowered sharply in recent weeks, especially after disappointing delivery numbers that were announced earlier this month.

Tesla’s stock has fallen nearly 21 percent this year, amid job cuts, a drop in the price of the cars, and a warning about a “difficult” road ahead. Above all, there is the growing investor concern about demand reaching a peak and profit margins thinning out as the company sells more lower-priced versions of Model 3 and the sale of high-margin Model S and X slow down.

The Elon Musk magic may also have run its course. In times past, every Musk tweet or comment citing lofty ambitions used to send Tesla’s stock soaring, while in two recent such events, the reaction has fallen flat. The latest, an autonomous-car focused event that was hosted by the company on Monday, failed to make much waves in the stock. According to Goldman Sachs, the event was merely “a way for the company to focus investors away from the underlying demand and margin pressures the company is currently facing as they bring the Model 3 to mass market.”

With that “autonomous smokescreen”’ now cleared out of the way, clues about demand -- which would include the forecast for second-quarter sales, margin trends and plans for a potential capital raise will be the biggest items to watch out for when Tesla reports results after the market close.

Sectors in Focus Today

- Life sciences names after Waters Corp. fell the most intraday in more than 10 years on Tuesday following results. Results weighed on MTD, A, TMO ahead of their respective results: TMO raised its forecast after beating on the top and bottom line just minutes ago

- Electronic brokers (IBKR, ETFC, SCHW) after AMTD fell post-market after results; Goldman cited good expense control and the capital return program as positives that would offset light revenue

- E&P names (CXO, PXD, NBL) after OXY made a competing bid for APC (after CVX’s bid more than a week ago)

- Aerospace stocks and the military industrial complex (RTN, NOC, LLL) after standout results from Lockheed Martin that included raised forecasts Tuesday. Those figures boosted the S5AEROX index into one of the top performing sub-sectors. Boeing’s results this morning may also have a read through on the state of both military and consumer spending (commercial planes are only 60% of revenues, with its defense and services units accounting for much of the remainder, according to data compiled by Bloomberg) and its supply chain (SPR, TGI, HXL)

- GD earnings are due within minutes; NOC just raised its MTM forecast for EPS and maintained its revenue and CAPEX outlook

- Rails as CP was among the first to post less than desired results in the group (though they cited weather as part of the rationale). Positives included guidance and the description of April conditions as some of the best they’d seen. Other rail names like UNP and CSX soared last week on the back of strong results; NSC reports today post-market

Notes From the Sell Side

Apple received a pair of price-target increases, but neither firm was particularly enthusiastic about the company’s prospects. Goldman Sachs lifted its view to $182 – the prior $140 target was below the current Street-low view of $149 – seeing “less short term downside,” along with expectations for “no further deterioration of [iPhone] demand in China.” However, “European consumer sentiment implies the possibility for worse demand there,” and there is “increasing potential for Apple to miss consensus expectations at the unit and potentially the [average selling price] level." Separately, Bernstein lifted its own view to $190 from $160, saying that while numbers "appear safe," Apple’s "valuation has already returned to its peak from last year, next year’s iPhone cycle appears uninspiring, and the stock’s key question – the structural lengthening of iPhone replacement cycles – remains unresolved." Both firms have the equivalent of hold ratings on the company, which reports second-quarter numbers on April 30.

The long-maligned Snap is showing more signs of life in the wake of another positive earnings print. At least five firms raised their price targets, while JPMorgan upgraded it to neutral from underweight. While the results and outlook “were somewhat mixed in light of 100 percent+ appreciation in the stock YTD, we think SNAP has grown operationally stronger & more disciplined,” Douglas Anmuth wrote. He added that he was “encouraged by the new Android app rollout, but also believe it will be challenging for SNAP to age-up its user base over time.”

Piper Jaffray cut Kraft Heinz to underweight from neutral, saying 2020 estimates were “too high.” The firm wrote that the company bringing in a new chief executive was “the right move,” but that “he needs incremental brand spending to rejuvenate KHC’s dusty brands, which could weigh on EPS.”

Tick-By-Tick to Today’s Actionable Events

- Lulu analyst day (first since 2014); has announced a Strategic Plan that seeks to double men’s, double digital, and quadruple international revenues

- 7:30am -- BA, CAT earnings

- 8:00am -- BIIB, ANTM earnings call

- 8:30am -- T earnings call

- 10:00am -- Bank of Canada rate decision

- 10:30am -- BA earnings call

- 11:00am -- CAT earnings call

- 4:05pm -- FB, MSFT, V earnings

- 4:10pm -- CMG, NOW earnings

- 4:15pm -- PYPL, TSLA earnings

- 4:30pm -- CMG earnings call

- 5:00pm -- PYPL, FB, NOW, V earnings call

- 5:30pm -- MSFT, TSLA earnings call

- 7:00pm -- Chubb CEO Evan Greenberg speaks at The Economic Club of Washington, D.C.

- Treasury Secretary Steven Mnuchin and FDIC Chairman Jelena McWilliams speak at the Fintech and the Future of Banking conference in Arlington, Va

--With assistance from Esha Dey and Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.