Negative Interest Rates Aren’t Such a Departure After All

(Bloomberg Opinion) -- A new paper by Yale professor Paul Schmelzing is a reminder that it ain’t what we don’t know that causes trouble, but what we know that ain’t so. Two charts in particular refute conventional wisdom about long-term real interest rates.

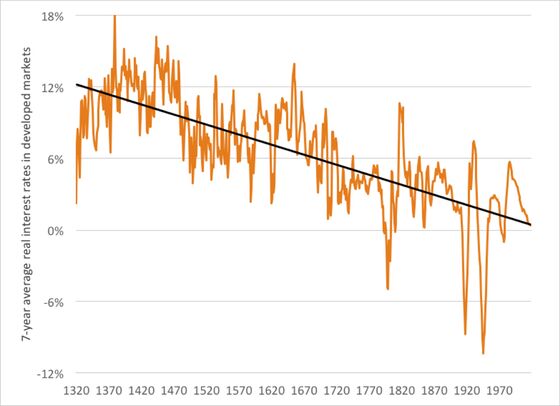

This chart, derived from one of Schmelzing’s, shows real interest rates in developed markets for the last 600 years. It shows a clear historical downtrend, with rates falling about 1% every 60 years to near zero today. Rates do tend to revert to a mean, but that mean seems to be declining.

Drawing a straight line to data does not prove anything about the future, but it does shift the burden of proof. You often hear claims that the “normal” level of real interest rates is 2% to 3%, but the chart suggests the last time 3% was the normal level was 1866. The “normal” claim drives arguments such as:

- Long-term bonds are bad investments at current rates because rates have to rise.

- The U.S. faces a serious fiscal challenge because when rates return to normal, debt interest will consume more than 20% of federal tax revenue.

- It’s prudent for pension funds to assume they can earn 2% or more above inflation on long-term on government bonds.

- Governments should take advantage of current low rates to shift debt to longer maturities, even issuing 100-year or perpetual bonds, and to borrow to fund huge infrastructure projects and social programs.

On the other hand there are people who accept that negative real interest rates are here to stay and contend they are a departure from history that requires radical policy changes to avoid “secular stagnation” and rapid increases in inequality. But the chart suggests that current levels of real interest rates are consistent with history and that there is no reason for shifts in policy.

The long-term future of real rates influences much more than the bond market and policy. Every financial instrument is valued by discounting future cash flows, so real interest rates matter in all markets. And the rates are long term; more than half of the current value of the stock market reflects cash flows to be received more than 50 years in the future. Rates are crucial for environmental choices — how much should we spend today to improve the future in 100 years? — and social welfare — should we increase taxes to raise the current living standard of the poor, or cut taxes to increase economic growth and raise everyone’s living standards in the future? It affects individual choices, such as how much education to get or whether to quit salaried work to open a business. A high real return means future wealth depends mostly on current wealth, while a negative real return means future wealth depends mostly on future earning ability. The former is good because people can earn financial security and weather economic fluctuations, but the latter leads to more equality.

The chart offers another challenge to conventional wisdom. We can explain, more or less, the yearly ups and downs of real interest rates, as well as their tendency to return to baseline levels. The historical record includes significant events such as the Black Death, continental and world wars, the Age of Reason, revolutions, silver inflows from the New World and the transition from feudal to modern economies, from precious metal money to fiat currency, and from divine-right monarchies to democratic republics. But there appears to be something much more fundamental than all of these things at work, something that operates over centuries rather than decades, something indifferent to the things economists study.

The paper includes a literature review that reveals that much prior work on long-term interest rate history was slipshod, little more than anecdotal and that the reliable works are often miscited. Schmelzing compiles copious primary and secondary sources. Rather than concentrating on a single European area, he manages to cover 78% of all developed economies across the globe; and rather than looking only at government debt, he includes private debt and investment in real assets.

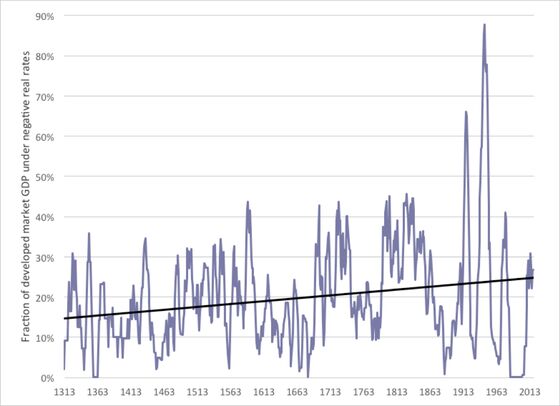

A second chart adapted from one of Schmelzing’s shows the portion of the global developed economy operating under negative real interest rates. A common assumption is that negative real rates are temporary aberrations. But the chart shows they have always been around. In fact, the only extended period in history without them is 1983–2008 (sometimes known as “the Great Moderation”). In the conventional view, the financial crisis of 2008 threw us into an unusual economic situation, but the chart suggests that it returned us to the historical trend from an unprecedented 25-year anomaly. Moreover, it suggests that over the next few decades, developed economies should expect negative real rates about a quarter of the time.

This paper doesn’t tell us what’s true so much as challenge what we thought was true. Maybe long-term real interest rates will average 2% to 3% in the future, and negative real rates will be rare; or maybe negative real rates will be common and cause fundamental economic changes. But both situations would represent departures from history.

Many people knowthat Will Rogers, or Mark Twain, first wrote this, but it ain’t so. Various forms of it have been traced to several 19th and early 20th century writers, but there’s no clear original source.

It’s a matter of controversy whether we should apply the same real discount rates to all these decisions, and of course people argue more over the effects of decisions than the discount rate to weigh present versus future costs and benefits. But the real rate of interest constrains the possible trade-offs and should be a major influence on policy decisions.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Aaron Brown is a former managing director and head of financial market research at AQR Capital Management. He is the author of "The Poker Face of Wall Street." He may have a stake in the areas he writes about.

©2020 Bloomberg L.P.