Tesla Seen Needing to Raise Cash Even If Elon Musk Is on a Roll

Elon Musk’s mojo won’t keep Tesla analysts from eyeing capital raise.

(Bloomberg) -- Elon Musk says his car company won’t need to raise money. Some analysts aren’t so sure he’s right.

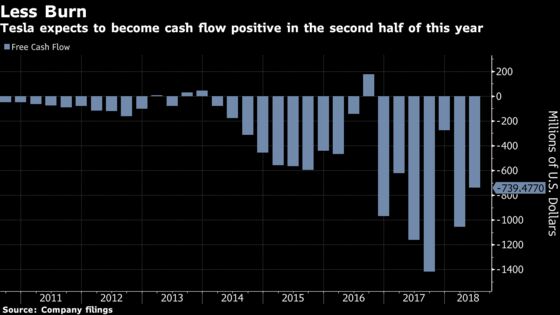

Tesla Inc. burned through $739 million in the second quarter, it said earlier this week, leaving it with its lowest cash level since 2016. The company’s net loss widened from the same period a year ago, and its gross profit fell.

“I have a hard time modeling them not needing cash,” said Cowen analyst Jeffrey Osborne, who’s expecting Tesla to raise $2 billion in convertible debt toward the end of this year. “As we look at the profitability profile of the company, coupled with cash burn the company has with all their expenditures and growth initiatives, as well as debt coming due over the next year, our view is they’ll have to raise capital in some way, shape or form.”

The electric-car maker says it’s turning the corner. Chief Executive Officer Musk said late Wednesday he expects the company to generate positive free cash flow in the second half of this year, and become sustainably profitable for the first time in its 15-year history. He also said he expects to be able to use cash flow to repay around $900 million of convertible debt maturing early next year. A spokesman on Friday declined to comment for this story.

Equity investors agreed that the news was positive. The company’s shares soared the most since 2013 on Thursday.

Musk has set goals for achieving positive cash flow before, and faced similar skepticism. Investors and analysts have repeatedly said that Tesla will need to raise money over the next year as it pursues ambitious expansion plans, with some estimates in excess of $2 billion.

Figuring out how to build Model 3, which is critical to Tesla’s efforts to make money, is proving tricky: the company is assembling some of the cars by hand under a tent outside its heavily automated plant. That may translate to higher expenses than it expects, which in turn may increase the company’s need for capital.

The company has asked some suppliers to give money back for capital expenditures on contracts dating back to 2016, a step that may either reflect rising production needs or desperation, analysts said late last month. Goldman Sachs Group Inc. said in May that the company may need to tap capital markets for more than $10 billion by 2020.

“Sustained positive free cash flow will depend heavily on improving manufacturing efficiency and maintaining discipline on capital spending,” S&P Global Ratings analyst Nishit Madlani said in an interview. “Positive cash flow in the second half is possible, but it’s not something we’ve built into our forecast as we are still somewhat conservative on the pace of reduction of manufacturing costs.”

Debt Due

Then there are the debt maturities to reckon with. Tesla had $9.5 billion of long-term debt outstanding as of June 30, more than $1.3 billion of which is coming due in the next 16 months. That includes the $920 million of convertibles the company has due in March. If Tesla’s stock price fails to reach the conversion price of $359.87 by then, it will have to pay that principal back to bondholders. The stock closed trading Thursday at $349.54, up from $300.84 the day before.

That’s not giving Musk any cause for pause just yet. He said he has “no expectations” to raise equity at this point, and plans to use local Chinese debt to help fund a new factory in Shanghai, its first outside of the U.S. It’ll cost about $2 billion for the factory to be able to build 250,000 vehicles a year, Musk said.

Expenses like that will only weigh on Tesla’s need for cash, said John McClain, a portfolio manager who helps oversee $21 billion of assets at Diamond Hill Capital Management.

“I find it very hard to make the math work to where they’re not coming back to the capital markets,” he said, in addition to the Chinese borrowing.

For more on Tesla, check out the Decrypted podcast:

To contact the reporters on this story: Molly Smith in New York at msmith604@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Jamie Butters

©2018 Bloomberg L.P.