Muni Market Looks to Next Year for an Infrastructure Bill and Bigger Returns

Muni Market Looks to Next Year for an Infrastructure Bill and Bigger Returns

(Bloomberg) -- The $3.8 trillion municipal-bond market is preparing to close out 2018 with lackluster gains as it looks to next year for better returns and a bi-partisan infrastructure bill from Washington to help boost spending on roads, schools and bridges.

Yields on tax-exempt securities soared this year as the Federal Reserve raised interest rates four times in 2018. That hampered performance, with the broader municipal market gaining nearly 0.9 percent in the year through Dec. 19, after a 5.5 percent advance in 2017, according to Bloomberg Barclays index data.

Along with higher borrowing costs, states and municipalities lost a financing tool that allows them to refund debt earlier than expected and save money.

Negative Net Issuance

Most municipal-bond investors are anticipating a second year where the amount of maturing debt and refunded securities outpaces the supply of new issuance, even though new-money sales are expected to increase in 2019. The market shrunk by $45.6 billion this year through Sept. 30, according to Fed data. That trend should continue in 2019 as state and municipal issuance fails to match or exceed refundings and retiring debt, according to Citigroup Inc., which anticipates the market will decrease by $15 billion next year.

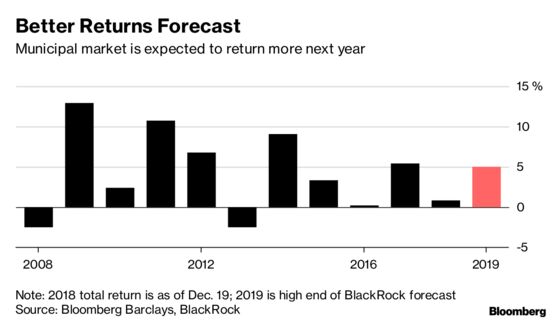

Bigger Gains

If the municipal-bond market continues to contract, that will help performance. BlackRock Inc. anticipates state and local debt could return as much as 4 or 5 percent in 2019 if the Federal Reserve slows down on interest-rate hikes. The Fed on Wednesday trimmed its projections for interest-rate boosts next year to two from three.

“In 2019, we again are going to have a net-negative year,” Sean Carney, managing director and head of state and local government debt strategy at BlackRock said in an interview. “You have an environment where your market is shrinking," he said. "More bonds are being removed then coming in new supply. That’s a strong technical and it should help aid performance in 2019.”

Banks Retreat

U.S. banks have decreased their exposure to municipal debt, paring their holdings of the securities for three straight quarters, the longest-running retreat from the market since 1996. That may continue in 2019 as the firms are less likely to invest in municipals for their tax advantages after the federal government last year cut the corporate tax rate.

“I would expect their holdings in municipals to continue to decline at the same pace,” said Guy Davidson, who helps manage $42 billion as director of municipal investments at AllianceBernstein LP. “The only thing that would stop that would be a sharp sell off in municipals relative to corporates and we don’t see that.”

Advance Refunding Push

States and municipalities will be urging Congress to bring back advance refundings, a mechanism that allows issuers to lower their borrowing costs by refinancing bonds before they can be called back from investors, according to Ken Bentsen, chief executive officer of the Securities Industry and Financial Markets Association. Last year’s tax-cut law ended the use of advance refundings and local governments have been pushing to bring that instrument back. It will depend on how hard states and cities work to let Congress know the benefits of advance refundings, Bentsen said.

“It’s really going to be largely dependent on how much congress hears from its towns and states on this,” Bentsen said.

Infrastructure Hopes

It’s a popular initiative, but Congress has yet to agree on how to fund a federal infrastructure bill that would help repair the nation’s aging roads, water systems, schools and airports. President Donald Trump campaigned on a pledge to improve infrastructure throughout the country but his $200 billion plan failed to pass the House or the Senate. With Democrats taking control of the House of Representatives again in January, a federal plan to help finance public works projects may gain traction.

“If there is anything they would expect out of Washington it would be a policy that would increase infrastructure spending,” said Davidson.

Funding such a measure could come from private activity bonds, public private partnerships or creating bonds similar to the taxable Build America Bonds that Congress enacted during the last recession to help spur infrastructure investment, Bentsen said. The securities are repaid with annual federal subsidies. It’s a structure that the market and issuers are familiar with, he said.

“They’re going to have to think about different mechanisms that they can use to incentivize private capital to come in and help fund this,” Bentsen said. “A direct pay bond whether it’s a Build America Bond or something like it is an option that we think Congress will take a look at because they have experience with it. There are investors willing to buy it or issuers willing to issue them. It would be hard for them not to look at it.”

--With assistance from Amanda Albright.

To contact the reporter on this story: Michelle Kaske in New York at mkaske@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Michael B. Marois

©2018 Bloomberg L.P.