States, Cities Forgo Projects to Keep Glittering Balance Sheets

States, Cities Forgo Projects to Keep Glittering Balance Sheets

(Bloomberg) -- Asheville, North Carolina, has a growing population, a burgeoning beer industry and a big slice of the billions of dollars tourists spend each year visiting the Blue Ridge Mountains. It also has $390 million of work it wants to do on its infrastructure.

What the city hasn’t been doing is running up debt to pay for it, with its 92,500 residents on the hook for only about $78 each for bonds backed by the general government budget. “We have a lot of people politely asking, ‘You’re a AAA city and your roads are terrible,’” said Vijay Kapoor, a city councilman. “What gives?”

That’s the paradox of America’s states and cities. The decade-long economic expansion has left surpluses where there were once deficits, interest rates are veering back toward more than half-century lows and there’s hundreds of billions of dollars of spending needed to refurbish roads, sewers and public transportation systems. Yet around the country, governments are showing little interest in borrowing money, cautious that a recession that by some measures seems overdue could resurrect the years of austerity that followed the last one.

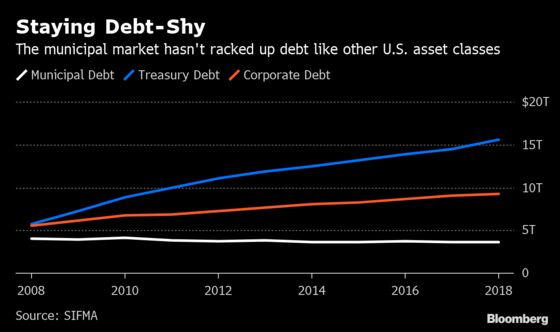

The fiscal restraint has turned the $3.8 trillion municipal-bond market into the only major corner of American finance where the amount of debt is shrinking, with borrowing by businesses and consumers steadily on the rise, according to Federal Reserve Board figures. It also stands in stark contrast with the federal government, whose rising deficits have caused the amount of outstanding Treasury debt to more than double since 2010 to almost $16 trillion. States and have paid off bonds, leaving owing $143 billion less than they did nine years ago.

“There’s this political sentiment or political culture that makes it difficult to raise taxes or issue debt,” said Tracy Gordon, a senior fellow at the Urban-Brookings Tax Policy Center, who researches public finance issues.

The reduced debt load is positive for the finances of American states, whose swelling tax collections have allowed them to continue to invest in public works while stockpiling cash to weather the next economic contraction. It’s also been lauded on Wall Street, where investors have bid up the prices of state government bonds. But the aversion to debt has left them missing an opportunity to borrow at low rates for the $2 trillion of additional spending that the American Society of Civil Engineers says is needed over the next decade to fix the nation’s infrastructure.

“There simply needs to be more infrastructure borrowing,” said Philip Fischer, head of municipal-bond strategy at Bank of America Corp., the biggest underwriter of state and local-government debt. “It has to happen. There’s nothing to compete with a plain old revenue bond.”

Instead of selling debt, states are increasingly paying for infrastructure projects using cash, according to a June 3 report from Moody’s Investors Service. The company said bonds only account for 26% of what states spent on transportation in 2018, down from 35% in 2011.

Debt Aversion

While the aversion to debt isn’t universal -- with the new governors of California and Illinois both moving to step up borrowing for public works -- it cuts across the political spectrum. In Connecticut, the new Democratic governor, Ned Lamont, has proposed curbing debt sales as he contends with large liabilities to employee retirement funds

Ohio Republicans deemed it better to raise taxes than to borrow money. This year, they passed the first gas-tax increase since 2005 to raise an estimated $865 million a year for road projects. As part of his pitch to lawmakers, Governor Mike DeWine, a Republican, condemned the use of debt by the state transportation department.

Arkansas Governor Asa Hutchinson, a Republican, said he wants the state to go back to using a pay-as-you-go approach. The state won’t issue bonds as part of a $95 million highway-funding law passed this year. “That’s one of the selling points,” Hutchinson said in an interview. “This will allow more to go to highways.”

The debate is raging in other states and cities, too. North Carolina Governor Roy Cooper, a Democrat, has proposed putting the sale of $3.9 billion of bonds for schools up to a vote, but he’s faced opposition in the Republican-led legislature.

“You get those dollars out and you have debt for the next ten to 20 years -- it really ties your hands to do anything else,” said Harry Brown, a Republican and state senate majority leader. He’s proposed devoting money from a state infrastructure fund to schools instead.

Much of the resistance appears to boil down to an anti-debt mentality. It took Montana Governor Steve Bullock most of his term to get lawmakers to agree to a $400 million infrastructure deal that includes the sale of new bonds. Bullock said the reluctance to borrow concerned him, given companies have taken advantage of the low interest rates.

“Building and rebuilding what we need shouldn’t be a political and partisan issue,” he said in an interview. “That’s not the way business is run, and government shouldn’t run that way either.”

In Asheville, the needs have grown alongside the city, where the population has climbed almost 11% since 2010. Kapoor, the Asheville councilman, who works as a financial consultant to local governments, said his city needs to increase spending on essential work like paving roads. He wants the city to put a bond proposal on the ballot in 2020 so it doesn’t miss out on a chance to borrow before interest rates rise.

If not, he said, “we’ll all be looking in the past, wondering why didn’t we do it then.”

--With assistance from Martin Z. Braun, Romy Varghese, Elizabeth Campbell and Mark Tannenbaum.

To contact the reporter on this story: Amanda Albright in New York at aalbright4@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Michael B. Marois

©2019 Bloomberg L.P.